Economists, or professional guessers as they are also known, have been throwing inflation and GDP estimates all over the shop to see what will stick. This is likely to continue well into the future as we move into an investment environment dominated by macro headlines.

In essence, globalisation, the pandemic recovery and deep-rooted structural issues have caused high inflation. Governments became too relaxed with regard to low inflation and low interest rates and now reality has dawned. Countries scramble to secure renewable energy and become less reliant on countries such as China and Russia for energy imports.

Unemployment rates are lower and job vacancies are high, but with ageing populations there are not enough workers to fill the roles. This will be a key theme going forward and will dictate much economic and social policy.

When reading the headlines, one can be forgiven for thinking it is all doom and gloom for the UK economy. The UK is in a recession and the forecast is that it will be a rough time for the next few years. Although this could be the case, it may also not be! Over the past year we have seen how wrong forecasts can be, so it is not prudent to place too much importance on these estimates.

Unrest in China is stirring markets, with investors concerned about the government’s possible reactions. Economic growth is already under strain and the long-term outlook is far from certain.

Any upside surprise next year is likely to come from growth holding up in company earnings, or by inflation falling faster than expected. This, coupled with easing political tensions, would provide a boost for equities.

Any downside surprise would be company earnings falling further than expected (generally, a fall of 10% or more). Also, if interest rates put pressure on government finances this will increase bond yields and send equity markets lower.

Areas of Focus

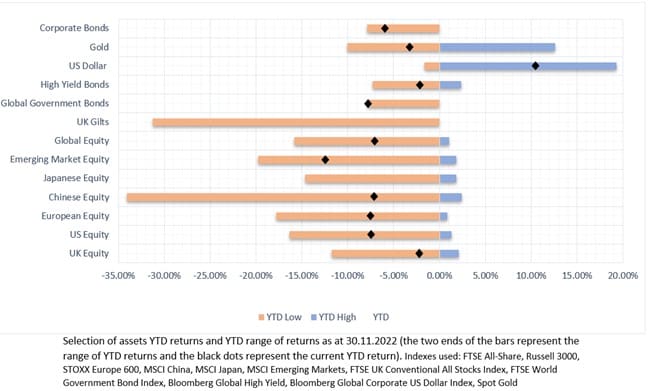

- Corporate bonds continue to make steady gains as more investors buy into the sector.

- Despite bleak economic forecasts, the FTSE 100 continues to perform well and other FTSE indices have started to regain some ground.

- Shorter dated government securities are still preferred over longer maturities as the premium for holding these amid persistent inflation increases.

- Against a backdrop of persistent inflation, index-linked securities do have some upside.

- Volatility in crypto currency markets and the bankruptcy of the FTX exchange show this market is extremely speculative and is certainly no replacement for gold.

- The US dollar has given up some of its strength and this may continue into the New Year.

- Emerging market debt is looking attractive amid a falling US dollar.

UK

Political Background

Matt Hancock left the I’m A Celebrity Jungle in third place. The next day the FTSE 100 dropped by 0.51%. Is there a link here? Is this the start of the next stage of the bear market? (Probably not, but it’s more interesting than continually talking about inflation.)

Jeremy Hunt, the new Chancellor of The Exchequer, released details of the Autumn budget on 17th November.

Clearly there were stark differences from his short-lived successor’s mini-budget and many of these changes will affect investors, business owners and individual consumers alike. While Kwasi Kwarteng presented unfunded tax cuts, Hunt has pushed to increase tax revenue by cutting allowances and in turn creating further stealth taxes.

Stealth taxes are aptly named as they are easy to overlook, due to the fact they do not generate immediate tax revenues. Rather, by freezing the allowances and income thresholds until April 2028, more income is pushed above the allowances and into higher thresholds as individuals’ earnings grow and the thresholds and allowances do not, generating additional tax revenue over time.

The main taxation highlights from the Autumn statement were as follows:

- Main income tax allowances and thresholds as well as National Insurance thresholds and the inheritance tax nil rate band will stay at their current levels until 2028.

- 45% additional rate tax threshold will be reduced from £150,000 to £125,140 from April 2023.

- The dividend allowance will reduce from £2000 down to £1,000 from April 2023, and then this will drop to £500 in April 2024.

- The capital gains annual exempt allowance will be reduced from £12,300 to £6,000 from April 2023. This will then be reduced to £3,000 in April 2024.

The reduction in the dividend and capital gains allowances severely reduce the scope for investors to shelter investment income and gains from tax, and highlights the need to use as much of the £20,000 annual ISA allowance each year. Other tax wrappers such as offshore bonds will become more relevant.

The reduction in dividend allowance and higher dividend tax rates will slightly reduce the appeal for business owners in taking dividends. The National Insurance savings will still make the dividends more attractive, however.

The goal of the Autumn Budget was to try to restore credibility in the UK fiscal system. However, many commentators believe it will not be enough, and that further tax rate increases will be needed in order to generate the revenue needed from a smaller economy.

Economic Growth and Inflation

UK CPI inflation rose to 11.1% in October, up from 10.1% in September. Despite the government’s Energy Price Guarantee, rising energy costs were the biggest contributor to this figure. Food prices also rose, while transport, motor fuel and second hand cars partially offset the increase with declining prices.

Oil prices have again fallen this month, weighed down by lockdowns in China (which will help to counter price rises in other areas). While last month the consensus was that inflation will peak sometime in 2023, economists now expect this to be in December 2022. While these forecasts change all the time, the key is that inflation will peak and then start to reduce.

The BoE have given signs that rate increases may slow further if market data points to too much economic damage. This is helping to boost equity and bond returns.

The BoE base rate currently sits at 3% and in December this is expected to rise to 3.5%, settling next Spring at around 4.6%.

According to the OECD, the recession in the UK is expected to be the worst out of all major economies, even more so than European countries who have been arguably the worst hit by the energy crisis.

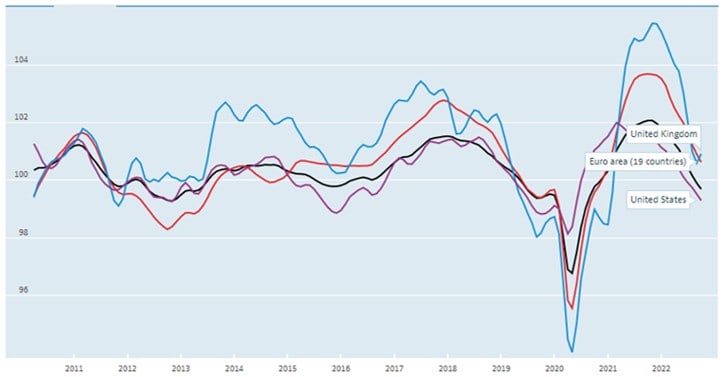

The above chart gives an indication of how consumers feel about future consumption and saving. The purple line highlights how much worse UK consumers are feeling compared to US and other European consumers. The UK continues to trend downwards while the US has ticked upwards, likely because of potentially easing inflation.

This is not surprising reading. High energy costs, which are going to be higher in April 2023, increased taxes and rising inflation are putting pressure on UK households. Political instability is also not giving consumers confidence.

While consumer confidence is low, business confidence is not as bad, with the UK having a high indicator than the US or Europe.

Bond yields

Bond yields have fallen from their year high and in the last month have continued to fall gradually. The 10-year yield sits at 3.1%, down from 3.5% at the start of the month. The 2-year yield has fallen from its year high of 4.7%, and currently sits at 3.2%. However, over the last month the yield had initially dropped to 2.9% before returning to its starting level.

While bond yields have fallen due to investors betting on slower rate rises that previously anticipated, the 2-year yield rising again signals that investors are predicting a longer recession.

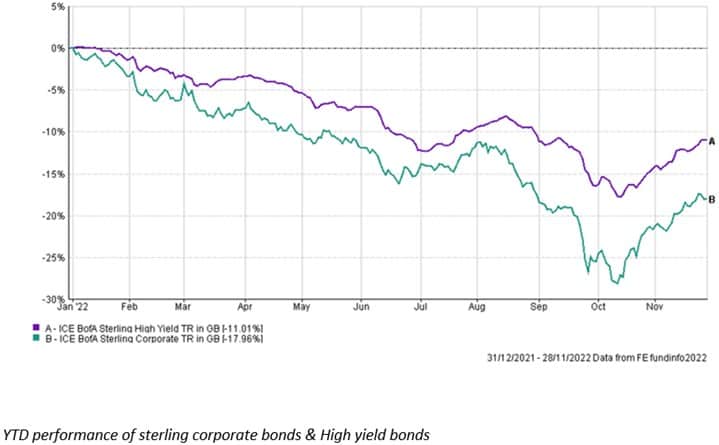

Corporate bonds have continued their upward surge with investors continuing to buy into the sector.

Corporate bonds experienced heavy selling this year but investors now see lots of value in the sector. Corporate bonds have characteristics of both equities and bonds and the current climate is suited to holding them, especially when they have declined in value, making them attractively priced.

Corporate bonds offer a higher coupon (i.e. interest payment) than gilts and have a greater potential to experience capital growth in their market price. Investment-grade companies have been able to build up strong balance sheets over the past decade due to high growth and low borrowing costs. This makes them suitable to weather a recession and minimise their default risk.

While high-yield bonds have risen over the past month, this has been to a lesser extent than investment-grade. High yield or junk bonds have much lower credit ratings and so there is a greater risk of default. Their balance sheets are not as strong and so there is a greater risk of a bond payment being missed and even a loss of capital during a recession. Defaults on corporate bonds will rise as companies experience financial difficulties, and these are likely to be higher as we go down the credit rating ladder. Income is very attractive on high-yield bonds and is a welcome sight in a market long devoid of high incomes.

Currency

Having spent most of the year on a downward spiral, the pound has regained some ground of the US Dollar. Since the mini budget at the end of September the pound has risen more than 11%, sitting currently around the $1.20 mark.

The weakening of the Dollar is mostly a function of investors betting that the Fed will slow down its interest rate rises. It is debatable whether fiscal credibility has been restored in the UK, but certainly markets are more positive than under the previous leaders and this will have helped.

Sterling is still down around 11% against the dollar this year, however. Softer tones from the BoE around rate rises will likely keep the pound down.

A slightly stronger pound will benefit UK importers and help to reduce some of the imported cost inflation, helping to stabilise and reduce inflation over the coming months.

Market Movements

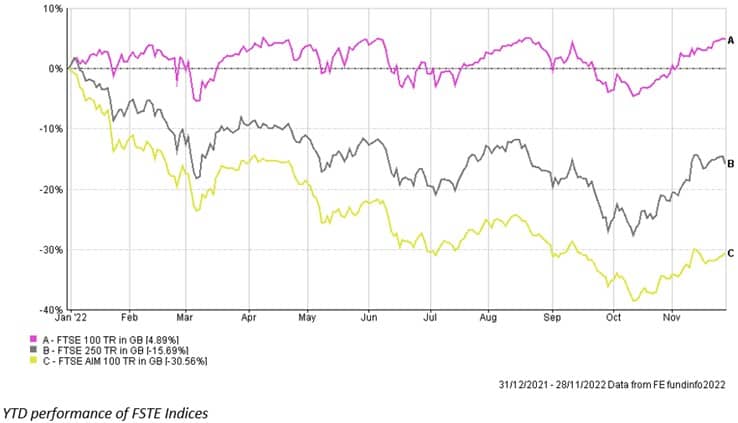

All FTSE markets continued to move upwards this month, with the FSTE 250 gaining 7.87%.

We can see that the FTSE 100 has dipped in and out of positive territory but is still up 4.89% this year. The AIM index fell nearly 40% and has a long way to go to regain this ground. The FTSE 250 has fallen but not as far, and has made a better recovery in the past month.

We can use the previous bond market recoveries to see why this is. Investment grade bonds are similar to FTSE 250 companies, while high-yield bonds are similar to FTSE AIM companies.

FTSE 250 companies are not as large as FTSE 100 companies and are deemed to be less financially strong. Therefore we would expect higher growth and higher volatility.

AIM companies are some of the smallest companies in the FTSE index. They have small balance sheets and are growing their business in typically immature industries.

High yield bonds are typically issued by small companies such as these. We would expect the highest capital growth in AIM companies that succeed, but the number of companies failing is also high, similar to a high yield junk bond and making them a high investment risk.

In a recessionary environment we would expect to see a greater proportion of smaller companies fail. As AIM companies are growth companies and the bulk of their cashflows are far into the future, interest rate increases discount their values by a greater extent, and this is what we have seen in their share price movements.

US

Economics

What is the Federal Reserve thinking? I am not sure even they know. Although many Fed members have indicated that rate hikes will slow and the next increase is expected to be 0.5%, some members have also said that they think rates will have to go further than the market expects.

Basically, they are not sure what is going to happen and they want to keep the sum total of rate hikes the same for now, but just take longer to get there. To some extent they do have time to do so – interest rate increases take time for their effect on inflation to be realised, usually around 18 months.

The inflationary outlook is looking better in the US, with inflation data for October showing annual CPI slowed from 8.2% in September to 7.7%.

Stocks initially rallied at the start of November but have since started to come back down. Some of this will be a function of the Fed’s minutes from their meetings, some will be from over excitement at a bear market rally, some will be from protests and instability in China.

The key theme in the US is a shortage of labour (a production constraint) and this is what the Fed is looking at. Interest rate increase cannot solve this issue, only major structural changes can.

Labour figures are important because if unemployment is low (currently 3.7%) and there are lots of job vaccines to be filled then the workforce will demand higher wages to fill these gaps. Higher wages lead to increased spending by consumers and increased costs by businesses to keep the profit line the same. This causes the dreaded “wage-price spiral” the Fed is keen to avoid.

In the US, like many other global economies, the number of people working declined sharply in the Covid pandemic. This had led to an increased number of job vacancies. But with unemployment at a 50-year low, why are there still lots of unfilled jobs?

One of the big issues is retirement and an ageing population. There is a continuous cycle of people retiring and young workers taking their place in the labour force. However, with an ageing population, there is a greater proportion of workers retiring relative to those starting their working lives, and over time this creates more job vacancies.

Furthermore, during the pandemic many workers decided not to go back to work and retired earlier than they otherwise would have.

Therefore, with a continually lower unemployment rate economic activity will have to be lower in order to avoid high inflation.

The Fed realise this and interest rate increases are designed to pull economic activity down in order to bring inflation under control. The juggling act is not to pull the activity so far down that it causes a deep recession. A recession on some scale, however, is most likely inevitable.

Persistent inflation above 2% is therefore also likely and is due to structural issues. While this may not be at the front of investors’ minds now, it is likely to result in a bigger premium demanded for holding government bonds over the longer-term.

This increases government borrowing costs and is not just a US problem but a global problem. If we look at China, not only does the country have an ageing population but it is forecast that for the first time they will have more deaths than births – actual population decline.

Market Movements

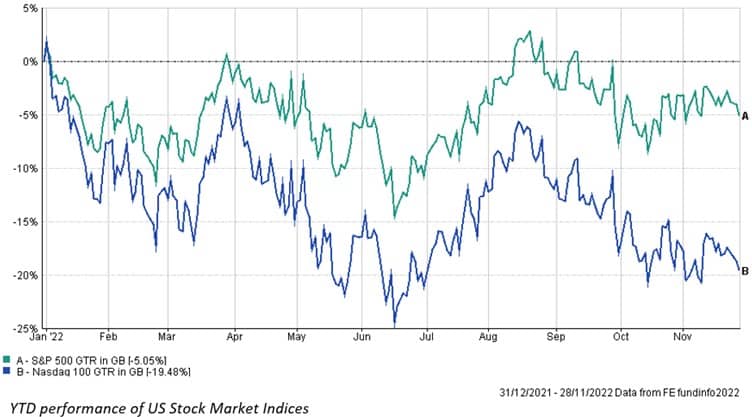

While the S&P 500 has regained some of the ground lost this year, the NASDAQ 100 is back on its way down.

Markets realise the Fed will have to move rates into restrictive territory but values have not dropped far enough to reflect the slower earnings growth that accompanies this.

Yields

The 2-year treasury yield has dropped slightly in the past three months, sitting at 4.4%. The 10-year yield sits at 3.7%, showing steep yield curve inversion.

The fact that the 10-year yield has dropped further than the 2-year yield highlights the heightened recession risk.

China

Growing unrest in China over its zero-Covid policy led to global stock markets dropping. Protestors gathered across various cities to demonstrate against the harsh restrictions.

This is a direct challenge to the Chinese government which has prompted concerns over the potential backlash.

Investors had previously speculated about whether and how China would relax its zero-Covid policy and this had caused markets to rise. Any relaxation would help in several ways – boosting consumer confidence, increased freedom to move around and spend, in turn boosting consumption and giving the Chinese economy the growth it is aiming for.

While most of the rest of the world has been tightening financial conditions, China has not. This is in an attempt to hit its goals for economic growth.

Inflation in China has remained relatively subdued, although at a 29-month high in September at 2.8%, the Central Bank is reluctant to loosen monetary policy any further for now due to the risk of rising inflation.

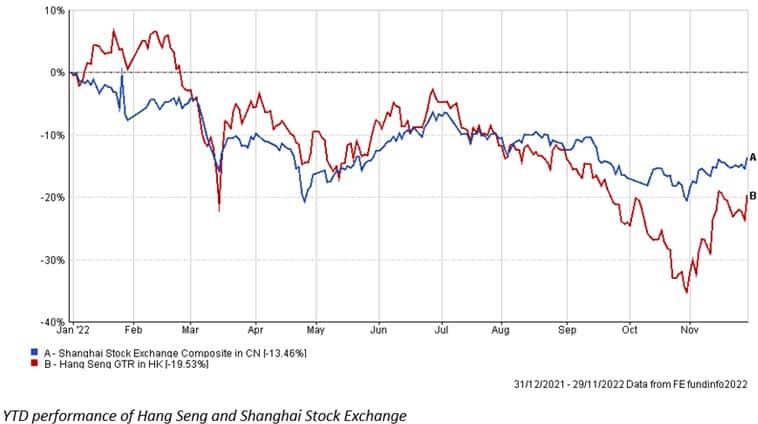

So far this year both indices have struggled, with points of resurgence in March, May and November. At these points investors questioned whether now was the right time to invest in China, but ultimately the markets fell lower. While short-term prospects may improve, longer-term the political risk is very high and it is unclear what direction Chinese markets may ultimately take.

Europe

Inflation in the Eurozone dropped to 10% in November, down from 10.6% in the previous month. This has again prompted investors to re-evaluate whether interest rates will need to go as high as previously forecast.

Inflation is projected to fall further from here as the main contributors to increasing inflation are energy and food prices. Energy prices have likely reached their peak and will fall slowly. Food prices face input lags and will fall, but likely not in the next month.

Like the US, inflation is expected to stick at levels above 2%, and the consensus is for this to be around 4%.

The ECB has raised interest rates in recent months, with the central bank’s base rate sitting at 1.5%. This is likely to continue into restrictive territory as the ECB will need to see clear evidence that inflation is on a continued downward path.

A recession for Europe is still forecast, but there will be heterogeneity as to who this will affect the most. For example, Germany is a big industrial country and will be greater affected by a recession than Spain, which is more focused on financial services.

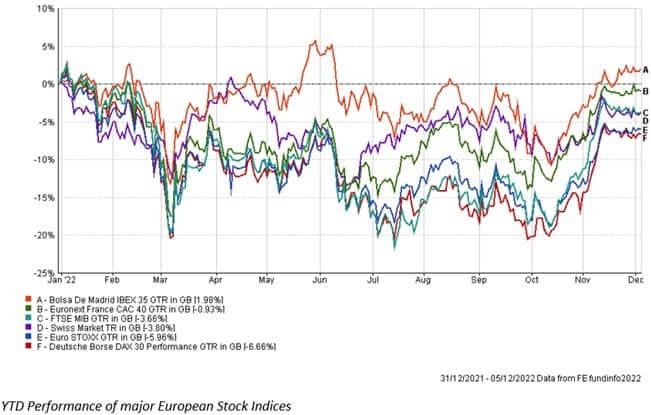

For most of the year European stock markets have underperformed most other global markets, due mostly to their proximity to the conflict in Ukraine and countries’ reliance on imports of energy from Russia. The German DAX index in particular fell by around 20% at its low point. We can see from November that all European markets have jumped, regaining a lot of lost ground.

There is downside risk next year with a correction in the first quarter likely. This will leave limited upside overall next year. Earnings could also drive markets lower as their effect is fully priced in

Robert Dougherty, Associate IFA

December 2022.

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.