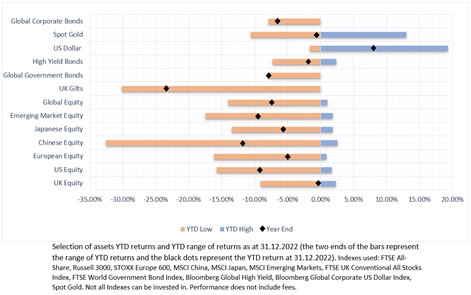

The war in Ukraine has highlighted that geopolitics presents a very important and a misunderstood form of risk. This risk drove markets all year and pushed equity values down with nearly all asset classes ending the year in negative territory.

There was no discrimination and fundamentals were in the backseat while inflation and interest rates eroded asset values.

High volatility was another key theme throughout the year, with large swings in prices the normality in the second half of 2022. Volatility does, however, drive markets and in order to recoup lost ground last year, more of it is needed – volatility is often associated with drops in markets but it also drives upwards rallies.

Last year was very much a bear market, with short-sellers finally rewarded after years of losses in upward market rallies. We experienced several bear market rallies throughout the year which only ended in further declines. The end of the year saw rises in equity values and some falls in bond yields as investors hoped that the US Fed would not have to raise interest rates as high as had previously been expected.

Added to this, bonds did not support falling equity values throughout the year (as they can usually be relied on to do) but instead dragged portfolio values down further, with inflation-linked bonds being some of the worst performing assets. The fixed income sector is more attractively priced now than it has been for a long time. With reasonable coupons and yields, investors seeking income can finally find it!

So it’s a new year, but is it a new market? In some ways yes, in other ways no. Volatility will remain high as investors risk premiums across all asset classes has increased. The key themes driving asset values this year will revolve around how long global recessions last for and how deep they go. This will in turn drive inflation, interest rates and company earnings.

The question is how much of the potentially upcoming economic damage and missed earnings potentials are priced in. Likely not enough, which will drag values down in the short-term.

Longer-term structural issues such as ageing populations and a shift in demand from services to goods will keep inflation elevated while growth is lower.

In previous periods, longer-dated government bonds were the “ballast” of a diversified portfolio, providing an income while protecting the portfolio from a recessionary environment. With inflation at elevated levels and banks raising interest rates into restrictive territory, recessions may be foretold (the consensus suggests the UK is already in one).

Investors in previous downturns could expect to move into longer-dated bonds which would benefit from the typical falls in interest rates. But with inflation high we cannot expect central banks to drop interest rates to the low levels seen since the financial crisis.

While central banks will slow down their interest rate increases and may reign them back in slightly, rates will still be at higher levels than we are used to, reducing the value of holding long-dated government bonds. Persistently high inflation will also erode their real values.

Although the first half of the year will present challenges, in our view the second half of 2023 may present ground on which asset values can grow. Values will be very much dictated by investors’ perceptions of economic damage and market risk.

Summing it up, we think the key investment themes for 2023 will be: the resurgence of the fixed income sector; dividends are key, so value stocks will outperform; and enterprising tech will be an attractive investment area.

Activity in China will also be closely watched, both in terms of its relations with the US and its economic growth. Any further retreats back into lockdowns will strain supply chains again and cause negative effects on equity markets.

2023 Key Themes

- A bottom-up portfolio approach will be key.

- Earnings will dictate equity returns.

- Corporate bonds are attractively priced with reasonable coupons. Companies’ strong balance sheets should help to keep defaults low.

- Long-dated government bonds will be less attractive as persistent inflation, higher interest rates and a larger risk premium pull their values down relative to shorter-dated bonds

- Inflation-linked securities are still preferred as inflation is forecast to stay at higher levels.

- Enterprising technology companies can provide returns while traditional technology stocks (think the “FAANG” companies) may struggle.

- Emerging market equities are positioned to have a better year after struggling in 2022, although the dollar is predicted to remain relatively strong.

- After an extremely challenging 2022, the outlook for sustainable and ethical investing is still bright over the longer term.

UK Equity & Fixed Income

Fixed Income

With bond yields now at higher levels, the fixed income sector is finally providing attractive levels of income for investors. Higher yields also provide a form of diversification – investors are paying less for the same level of income, so if yields do rise further they will not lose as much as they would have when yields were at rock bottom.

Put another way, when yields rise from 1% to 4% investors make a much bigger loss than if they subsequently rise from 4% to 5%.

If and when bond yields do drop, investors will make money if bonds are not held to maturity (the increased volatility will not affect investors who hold their bonds to maturity).

With the UK already likely in a recession and interest rates continuing to increase we can expect an increased number of business failings. While it will be expected that they will come from smaller and mid-sized businesses, any big business that may have looked artificially strong in the low interest rate environment will be challenged.

That being said, most defaults are expected to occur at the sub-investment grade end of the credit ladder, meaning high yield/junk bonds will be most affected. Investment-grade bonds have the strongest conviction from investors in the current climate. They pay an attractive coupon and are trading at a more attractive yield, and the issuing companies have been able to build up strong balance sheets.

Like equities, individual selection of corporate bonds will be key for investors.

With inflation expected to settle at a higher rate than previous years and stay there, inflation-linked securities are attractive. Although it must be remembered that inflation-linked bonds are typically longer-dated bonds, so any increases in interest rates above what is already expected will produce capital losses.

Equity

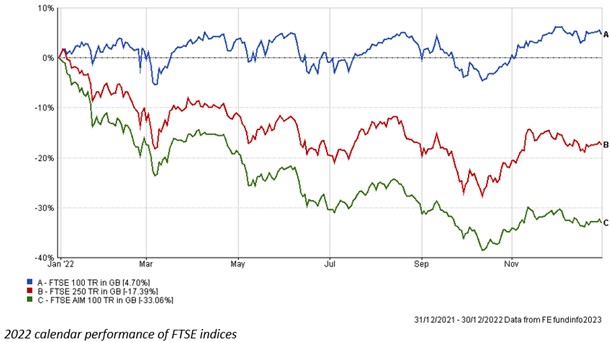

UK small and mid-cap stocks (“SMIDs”) had a very challenging year in comparison to those in the FTSE 100, which was the best performing developed market index last year.

While the current and future environment makes SMIDs a difficult place in be at the moment, it is worth considering what is reflected in their price.

UK SMIDs have had a lot of bad news compounded into their prices, mainly impacting domestically focused companies, but in general there was little discrimination between all companies. Smaller companies may find it harder to pass on rising costs and will see their earnings miss targets. We are already seeing this across the supply chain with companies struggling to pass on inflation in transport, currency and materials costs onto the consumer.

There tends to be higher default rates in recessionary phases in smaller companies (i.e. more of them go out of business in a typical recession). The mindset across the board last year was against anything that wasn’t income/value-oriented or large cap stock, and everything else was consequently punished.

While this will have hurt returns last year, in 2023 this provides a good base on which to invest in the sector at lower levels. The key this year will be in the bottom-up selection of stocks in each industry and sector. The question to ask is, which stocks will show resilience and be able to face the challenges ahead most successfully?

Further to this, as businesses do fall in value or default, it provides room for other competitors who are better positioned to gain market share and increase their value.

It is unusual for small caps stocks to underperform large caps based on historic data. Following a period of underperformance, they usually outperform over the next four to six years of the business cycle. While the market dynamics we are currently in are different to past dynamics, it would not be unreasonable to put some probability on this happening, mainly down to the difference in base value at the end of 2022.

Lower prices can also make companies take-over targets, which will boost their share prices as bidding companies offer a premium over the current share price. We saw how previously companies like Morrisons were taken over by US private equity and it would be surprising if this sort of activity did not resume in the next few years, particularly if the UD dollar remains strong against the pound.

Questions over the wider economy will be centred on whether firms will reduce their workforces and if so, how quickly. Also, how much further will consumer spending be squeezed and where will inflation and interest rates go from here?

The tightness of the labour market will continue to be watched by the Bank of England as it was for all of last year. The outlook for energy prices throughout the year will be a big factor in determining how much disposable income consumers have and how much of that spare income is spent. Any decreases in prices will help to stop the recession being as deep as it may otherwise be.

All in all, the sentiment may look gloomy presently, but an upside of this is that if conditions improve even slightly, we will see a rebound in values.

The outlook will depend on individual businesses rather than sectors as a whole. The key company specific factors investors will be looking at are: the strength of the balance sheet, the quality of the company’s earnings, the company’s ability to pass on costs to the consumer, and whether the company has sufficient cash to grow the business.

US

Equity

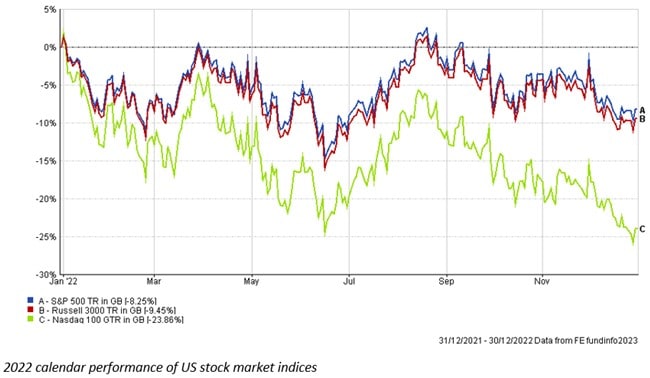

US equities started 2022 at high valuations relative to Europe and the UK. These were soon brought back down, not too the level of other areas but enough to wipe huge values off some large and well-known companies. This is likely to continue into 2023 with earnings estimates projected to miss targets.

Tech stocks in particular were a highlight (or lowlight!), with the NASDAQ dropping by over 23%. We are unlikely to see any major rebounds in value for the first half of the year at least. Upside surprises will likely come from interest rates stopping short of expectations, but in our view this is unlikely based on the Federal Reserve’s commitment to bringing inflation down.

US equities struggled in 2022, with the S&P 500 down approximately 17% over the year. This was partly due to multiple aggressive Fed interest rate hikes throughout the year in an attempt to tackle record high inflation levels. Unlike recent history, 2022 also witnessed most global government bond prices fall just as much, if not more, as equity prices.

The US macroeconomic outlook still looks bleak in 2023. High-interest rates, weak consumer confidence and a slowing US economy are expected to damage company valuations and slow earnings growth this year. With this in mind, many analysts forecast US equities to fall further in 2023.

On a brighter note, US government bonds are looking attractive to investors seeking risk-free positive returns in 2023. Investors can expect 4-6% returns in the US government bond market, with increased overall returns if the US economy dips into recession.

An economic downturn could force investors to seek “safe haven” assets, such as risk-free US government bonds. The US corporate bond market is also expected to be lucrative in 2023, but investors must seek quality options – although they may look attractive, investing in this sector may not be worth the risk during a potentially extended default cycle.

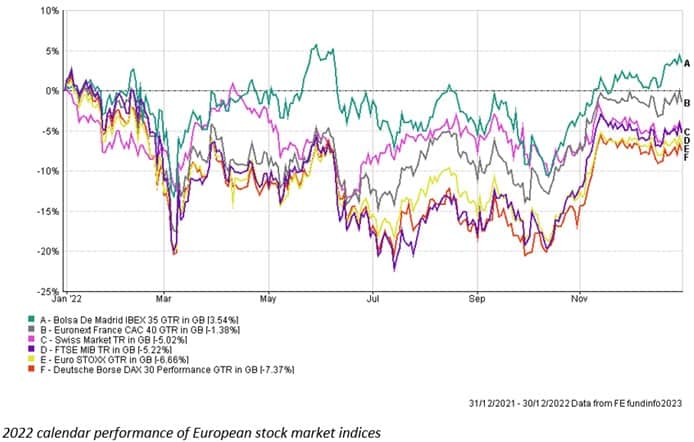

European Equity

In our view, the outlook for European equities is now brighter than it was in the middle of last year, partly because values had already fallen quite far. Inflation has eased recently and investors are betting that this means it has reached its peak. This could be premature and any uptick in the inflation figure will damage equity and bond values further.

The ultimate outcome of this continually lower inflation could (we hope) be rising equity values, but only to an extent. Recessions are predicted across the bloc and once again, the extent and length of this coupled with the corporate earnings environment will be the main drivers of values.

Even though inflation has ticked down, single data points such as this won’t be enough to convince the ECB that interest rate rises need to slow or stop. They have also said that rates will continue increasing to higher levels than investors currently expect.

When investing in this region, discretion will also be needed – the different constituent countries have very different economic makeups and will fare differently.

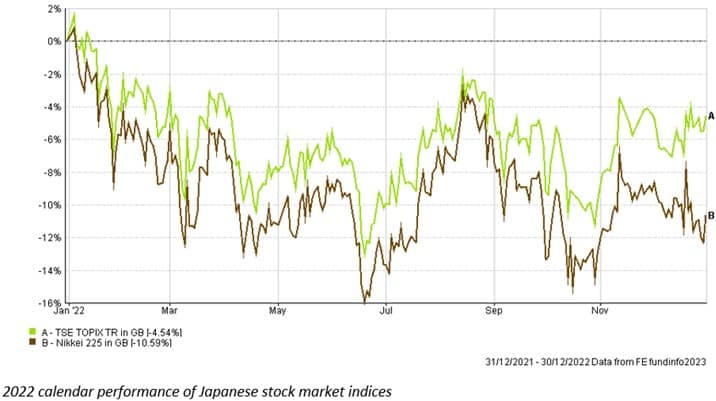

Japanese Equity

While many other economies are expected to enter the recessionary phase of the economic cycle, Japan is at a different stage. After years of deflation, inflation is creeping in at low levels and allowing the Bank of Japan to remain accommodative in its monetary policy (aiming to bring about economic growth).

The effect of this loose monetary policy is that the Japanese Yen has weakened, putting pressure on domestic producer prices. This has in the past benefited Japanese corporates, and we are seeing healthy corporate earnings ahead of expectations.

Increasing price inflation could also help to boost wage inflation next year, in turn boosting consumer spending. The outlook for Japan is therefore looking positive but as we saw at the start of 2022, nothing is certain and the potential for downside is ever-present – a rapid rise in Covid infections leading to lockdowns, for example. Another area to look out for is the changing of the governor of the BoJ and how this will affect the implementation of their yield curve control.

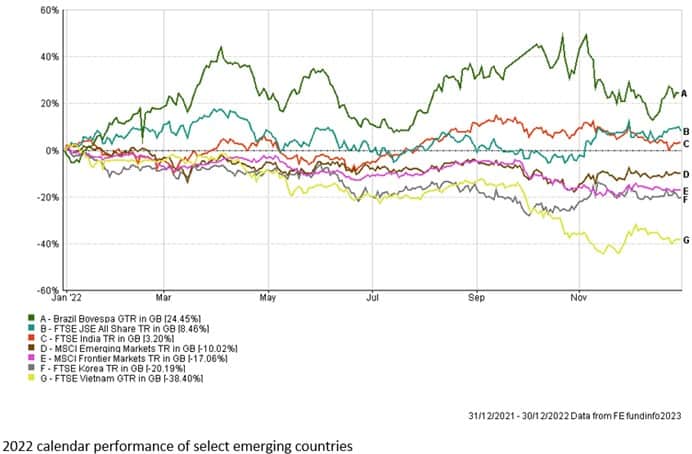

Emerging Market equity

Emerging market equities overall have had a poor year for a number of reasons, including: China and its crusade of regulatory reforms, covid and zero-covid policies, investors reducing their allocation to risk assets generally, global commodities inflation and a strong US dollar.

Select countries such as Brazil have however had a strong year of performance.

Surprisingly to some, China is still categorised as an emerging country and accounts for nearly a third of emerging market indices, so sentiment in China is a heavy driver of investors’ allocation to emerging markets. China has had its share of issues last year (albeit quite different to western economies) and this helped drive volatility in EM markets.

Interestingly, the MSCI Emerging Market index currently trades at a forward Price/Earnings ratio of 10, whereas the S&P 500 is trading at around 17 despite heavy falls last year.

What reasons are there for considering EM investment in 2023? Nothing is guaranteed but several factors could make this sector an attractive investment.

Firstly, the US Dollar has weakened a fair amount since the backend of last year, dropping by over 10% since it reached its 52-week high. This helps both emerging economies and the companies within them, whose debt is often denominated in the US Dollar. A weaker dollar makes the interest payments on this debt cheaper, freeing up cashflows for growth.

With the war in Ukraine causing countries to re-assess their reliance on China, Russia and other exporters, other emerging countries may be able to fill these gaps and improve their own trade-relations with major economies.

The strain that the US-China trade relationship is currently under is evidence of this. Countries in Latin America, India and other Asian countries could benefit accordingly.

The growth China had hoped to create through its flagship Belt and Road Initiative lending program has burdened many emerging countries with excessive debt loads, but if China is willing to support them and agree to restructured debt deals then this will be a tailwind for growth.

As you can see, talking about EMs involves a lot of talk about China and we focus on this country in the next section.

The other market worthy of a specific mention is India. Indian equity has remained relatively flat over the last year, having recovering from a long and deep decline. Over the longer-term, growth in Indian equity has surged, giving investors high levels of returns. There are questions over whether the region is now over-valued, but over the long-term we believe there is the potential for significant growth.

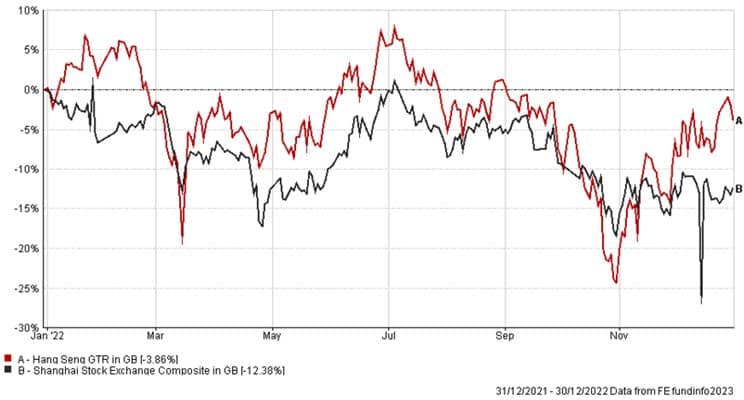

China

China’s relaxation of its zero-covid policy was much-anticipated by investors. Economic growth was slowing, supply lines were still tight and the property market is in distress.

The knock-on effects of hospitals unable to cope with the number of patients, inaccurate reporting of the number of covid related deaths puts pressure on the government and economy. It was a pipe dream to think that China would open up fully without any consequences. It is expected though, that if China stays the course some form of stability will return in the next few quarters.

The Chinese government will be pushing growth policies in 2023, most likely targeting growth of around 6%. This will be above the IMF’s more realistic forecast of 4.1%. Like Japan, China is at a different stage in its economic cycle, with inflation low and the capacity to ease monetary policy further.

The downside of this is that the yield advantage that Chinese government debt had over US government debt has now disappeared.

Key issues will lie in restoring relationships with western countries, most likely in Europe rather than the US, and restoring confidence in the property market (which has been a big driver of GDP growth in recent years).

Government policies aimed at boosting consumer spending will help domestic companies and the economy as a whole, and some investors are seeing this as a sign to start reinvesting in China.

Valuations have also dropped drastically, and while corporate earnings were subdued last year due to the zero-covid policy, its relaxation could provide a boost to earnings and therefore to share prices.

The idea of whether this is the right time to invest in China has been put forward several times over the last two years as investors reach for any good news to justify a change in attitude towards the country. Often political news dominates the headlines in China and it is hard to see what is actually happening in the economy itself.

So, is now the right time to invest in China? It remains very hard to say with any certainty. There are significant short-term risks and no one knows whether the government’s policies will achieve their goal.

Valuations are low however, and 2023 could be a building block for China to rebuild its economic growth, sort out its property market (although demand and growth will not be as high as pre-covid levels) and rebuild relationships with western countries. Longer-term there is definitely potential for big growth in the economy, but whether this will translate to investment returns is unknown.

Like all regions at the moment, selectivity is key and in China especially, keeping a diversified and balanced portfolio should be a priority.

Ethical & Sustainable

While 2022 was hard for most investors, those with an ethical or sustainable portfolio will have found it especially tough. Missing out on the positive returns from the oil and gas sector, and the typically higher allocation to technology stocks made 2022 a miserable year for the ethical investor.

There are however many positives to look forward to in the ethical investment area.

A global structural change is taking place and countries are aiming to reduce their carbon emissions down to zero over coming decades.

Coupled with the strains that the Ukraine war has put on the energy market in Europe, countries are increasing and accelerating the focus they are putting on their own renewable energy sources. The Inflation Reduction Act in the US is also supporting accelerated investment in clean energy.

All of this helps to provide a tailwind for clean energy.

Fossil fuels may be the solution to the current problem we face, but in the long-term they are not the answer and ultimately, it is the long-term which drives change and return. Nothing good comes easy, and difficult changes take time to bring about – time is the issue here and thus it is important to be patient when investing in ethical portfolios.

It is easy to think of just clean energy when thinking sustainably, but there is a much wider scope of investment areas and themes including, water, digitisation, circular economies, equality and corporate governance. These areas can be forgotten about but are just as important and are positioned well going forward.

Structural changes are needed and perceptions of the world are also changing. This change (or need for change) is what will drive the development and modernisation of the world.

There are two things to focus on while looking ahead.

Firstly, while ethical stocks were punished last year, they have returned from elevated valuations to a more reasonable base from which to grow. Secondly, as many sustainable stocks are in the growth/technology sectors, investors again did not distinguish between quality companies and overvalued companies.

This year, investors will feel the need to find something else to base their investment decisions on, and we expect that to be fundamentals – meaning that quality companies will revert to their intrinsic value, rewarding patient investors.