6th May 2025

There are a lot of different data points pointing to different outcomes. Recent US headline GDP data for the first quarter showed a contraction of -0.3%, less than the -0.4% economists had predicted. Markets actually moved higher on this news though – the main reason for the contraction was a surge in imports, which detract from GDP by essentially bringing forward future demand.

Shipping data from the Port of Los Angeles is expected to show a decrease in import volumes of 35% over a two-week period. Chinese manufacturing and export orders fell to their lowest levels since Covid-19. The American Association of Individual Investors Sentiment Survey has hit such low levels, that only once in its history has it been this low (the 1990 recession).

When survey sentiment previously reached this level it proved to be one of the best ever times to enter the market. The difference today is that we have just not seen as big a fall in markets as when the survey was previously at this level, so investors remain cautious.

Since the April 2nd tariff announcements markets have recovered somewhat, which leads us to think that markets do not expect a major recession and a major hit to business earnings. If this was the case markets would be a lot lower than they are.

Tariffs do not normally cause a recession. What markets fear will cause a recession is the unpredictability of policies. If businesses know there is a 10% tariff on a country because of a clearly defined reason, then they can plan around this for the future.

However, if tariffs keep being rolled back and then at the stroke of his big sharpie, Trump can reimpose them, this paralyses businesses and investment is delayed. This is exactly what we have been seeing. The rollback of tariffs may give markets a boost but it may also just highlight this unpredictability further – if Trump gets upset who is to say he will not reimpose tariffs.

Any recession caused by these policies is more likely to be short lived as it is defined as an event driven recession, rather than say a cyclical recession where recovery takes a lot longer (possibly what markets are expecting).

There is also a belief that the Federal Reserve will come to the rescue by cutting interest rates if growth deteriorates too much, but the Fed Chair Jerome Powell has reiterated that inflation and employment (i.e. growth) must be balanced and whichever is the furthest from target will be focused on. That is to say, if growth deteriorates and unemployment ticks up, but inflation picks up to a greater extent, we may see rates held where they are. We do not think markets have priced this risk in enough.

Think of it this way – as we noted earlier, shipping volumes have reduced because of tariff uncertainty, and if clarity on tariffs appears and volumes pick up again quickly, we could see a spike in inflation as oil prices rise and transport costs increase. Combined with potential tariffs this can turn an otherwise one-time price increase into sustained price pressure (if this sounds somewhat familiar, this is exactly what happened coming out of the Covid-induced lockdowns).

The issue is not only on the broad macroeconomic front, but also on US companies. The big US tech companies have come under fire, and much of this is by the Trump administration. Nvidia for example will have restrictions on how many chips it can ship to other countries depending on which tier they are in, and no chips are allowed to go to China. Clearly this impacts the earnings the company can generate and gives its competitors such as Huawei a chance to catch up.

Meta and Alphabet have been hit by anti-trust lawsuits by the US Federal Trade Commission (FTC). Other lawsuits have been filed in Europe as well contesting their business models and monopolistic like control.

That being said recent big tech earnings have beaten analyst estimates, providing more steam to lift their share prices higher.

While the US Dollar has weakened by just under 10% this year and US treasuries had shot up from just above 4% to 4.5% after Trump’s tariff announcements (although these have since fallen somewhat), investors have looked towards the safety of Swiss bonds, driving the two year yield back into negative yield territory (when you buy a bond with a negative yield you are essentially guaranteed a loss, in effect paying a price for security).

The UK got a boost from JP Morgan CEO Jamie Dimon praising Rachel Reeves’ growth strategy (although we suspect this has something to do with JPM expanding their European operations). UK companies have been performing better than their US counterparts, but we still believe the impact of tariffs, increased National Insurance contributions and higher interest rates will weigh down smaller companies from reducing their huge valuation discount.

To summarise, we are seeing the before data (in terms of tariff effects), but not the after data and this is what markets need to provide a sustained direction. Although Trump has come out with US protectionist policies, the world just doesn’t operate in that way anymore and interconnectedness is key to trade and growth. Uncertainty and change creates opportunity, with Europe getting a much-needed boost to spur potential growth.

–

Areas of focus

- Oil prices have fallen lower, driven by expectations of a global slowdown and an increase in output from OPEC. This can benefit certain companies such as airlines.

- High yield bond spreads have widened, creating a buying opportunity, but tariff uncertainty and high interest rates means we still see limited upside and a larger downside. Quality credit remains preferred.

- European equities continue their march upwards but still face short term pressures from a protracted trade war and possible threat from Chinese goods.

- Silver could follow in Gold’s footsteps, as the precious metal often does well while Gold prices are rising.

- UK equities continue to tick along this year posting positive returns, but smaller companies still remain under increasing pressure.

- Automakers are expected to be worst hit by tariffs, with luxury goods and beverages likely to be hit hard as well.

–

Asset Class Returns

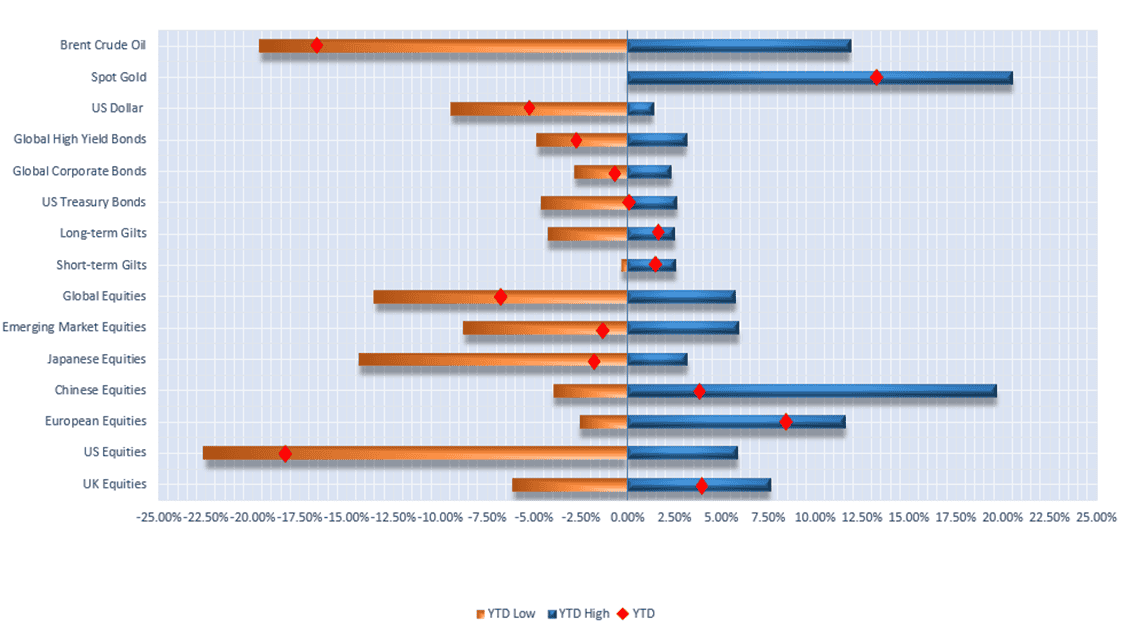

Selection of assets 2025 YTD returns and range of returns as at 02/05/2025 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch

–

US

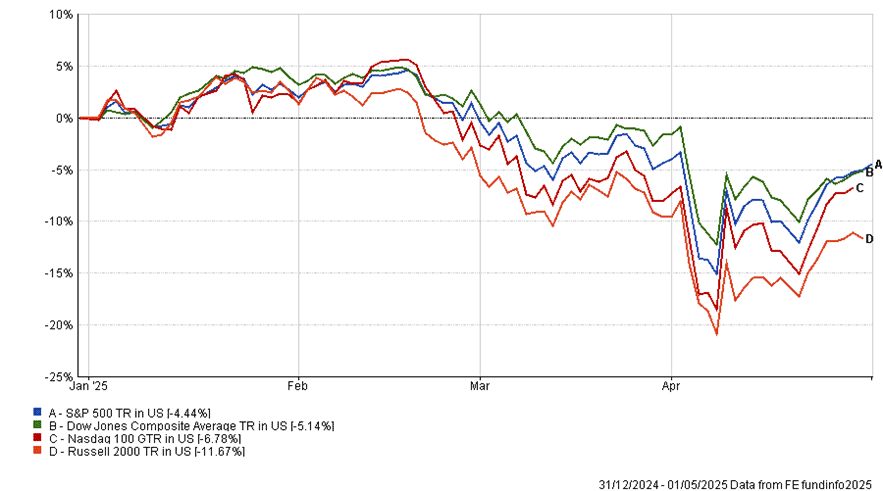

YTD performance of US equity indices (Source – FE Analytics)

The four major US equity indices end the month of April mostly flat, albeit not without major volatility. The S&P 500 was down 1.08% whilst the Nasdaq 100 was up 0.58%, bringing their year-to-date performance to -4.44% and -6.78%, respectively. The Dow Jones and Russell 2000 didn’t fare any better with losses of 3.60% and 2.35%, again, down 5.14% and 11.67% from the start of the year.

Declines from their all-time highs up until May 1st range between -8.63% and -19.23%, with the S&P 500 holding up the strongest and Russell 2000 being the weakest.

Although “Liberation Day” was in April, it feels like a distant memory with the waves of changes to tariff policy that have occurred almost daily. The uncertainty induced by this constantly shifting picture has significantly increased volatility in markets. The CBOE Volatility Index (VIX) hit a yearly high of 52.33 on 8th April – for reference, the index has been below 20 for the majority of the year. April 4th was the worst trading day (-5.97%) for the S&P 500 since March 2020, when Covid-related uncertainty was at its peak.

We will not go into too much detail on the current tariff environment here, as this was covered extensively in last month’s commentary, and changes with overnight tweets. However, in summary China have been playing tariff tennis with the effective tariff rate going both ways now well over 100%. Although Trump insists that negotiations between the two countries are taking place, the Chinese government stubbornly denies this. The outlined “reciprocal tariffs” on many other nations have been put on pause at 10% for 90 days, and finally, key industries such as pharmaceuticals and semiconductors are given exemptions.

With all this tariff talk, many investors have forgotten that we are currently in the middle of Q1 2025 earnings season. According to FactSet, of the 36% of S&P 500 companies that have reported so far, 73% have beaten Earnings per Share (EPS) estimates relative to the 5-year average of 77%. Assuming company earnings will continue as they have started, this will be the second quarter of double-digit earnings growth (Q1 2025 is currently 10.10%). The impact of the tariffs will not be in the numbers yet but many CEOs are highlighting the uncertainty they have caused in forward guidance.

All eyes will be on Jerome Powell as he announces the latest update to Federal Reserve monetary policy on 7th May. Markets are 91.6% sure (according to CME FedWatch) that the base rate will be held between 4.25-4.50% but they will take a keen interest in what he has to say regarding the future outlook. Powell has also been coming under fire from President Trump for “keeping rates too high”, with Trump also remarking that he could fire him if he wanted to. This rhetoric was later walked back by the President as markets took a disliking to calling into question the Federal Reserve’s independence.

| 1st April 2025 | 1st May 2025 | Change | |

| US 2 Year Yield | 3.89% | 3.61% | -0.28% |

| US 10 Year Yield | 4.18% | 4.15% | -0.03% |

| US Dollar Index | 104.26 | 99.81 | -4.45 |

YTD change in US bond yields and the US dollar index (Source – MarketWatch)

US bond yields tick down again over the month, likely pricing in the lower growth prospects as a result of slower global trade. The shorter end (2 year) came down more quickly than the long end (10 year), otherwise known as bull steepening. This usually suggests that markets anticipate base rates to drag down the short end without having much effect on the longer-term interest rate path. Rates coming down will act as a tailwind for risk assets.

These movements hide significant volatility in US Treasuries over the month, as yields rose 0.5% in a week at one point. This is unusual, as investors usually buy US government debt in times of uncertainty (causing yields to fall, rather than rise) and it led some to conclude that these bonds were at risk of losing their status as a “safe haven” asset.

There are several possible reasons, including speculation that the Chinese government (the second-largest foreign holder of US debt) started selling bonds to drive yields higher, as well as fears over inflation and leveraged investors such as hedge funds selling to cover their positions (see our Term of the Week for more detail on leverage).

Either way, many credit the rise in yields with forcing the US administration to “pause” the imposition of the reciprocal tariffs, following which both equity and bond markets breathed a sigh of relief.

The dollar also continued to weaken, with the DXY now below 100 – this too will be positive for risk assets, particularly as the dollar is still valued above its historical average on a trade weighted basis and so there is the potential for further weakness.

Finally, April was capped off with the first quarter GDP report. At the top level, the US economy contracted by an annualised rate of 0.3% over the quarter. This was worse than analysts’ estimates and way worse than the 2.4% growth shown in Q4 2024.

To understand the reason for this print, we must first understand how GDP is calculated. In broad terms, GDP is the sum of consumer spending, business spending, government spending, plus net exports (exports minus imports). As businesses rushed to import as much as possible before tariffs came into effect, the net exports part of the equation was significantly reduced, pushing down overall GDP. Data for Q2 will likely show the reverse as imports should be notably lower, assuming spending and exports stay relatively stable.

–

UK

Inflation in the UK slowed in March to 2.6%, down from 2.8% in the 12 months to February. This was a larger decrease than expected, with the ONS quoting a reduction in petrol prices as the main reason for the decrease in prices.

On the other hand, UK food inflation increased to an 11-month high of 2.6% in April, up from 2.4% in March as the price of food staples such as bread, meat and fish all witnessed steady increases in price.

Higher employment costs in the form of increased employer NI contributions and an increase in the minimum wage came into effect last month. Many economists believe this is the main reason for the heightened food price pressures, with retailers passing their increased costs onto the consumer.

According to their recent report, the International Monetary Fund (IMF) predicts that UK inflation will be the highest among the world’s advanced economies this year due to higher energy and water bills. The organisation also cut its 2025 growth forecasts for the UK economy,

In response to the likely impact of Trump’s tariffs on UK economic growth, markets have now almost fully priced in a 25-basis point interest rate cut at the Monetary Policy Committee’s next meeting on 8th May. Markets currently also expect three more interest rate cuts by the Bank of England later this year.

According to Nationwide’s latest figures, UK house prices were down 0.6% month-on-month in April. A slowdown in prices was largely expected due to changes in stamp duty from 1st April. Although average house prices fell slightly over the month, they remain 3.4% more expensive than they were a year ago. The average price for a UK home is now estimated to be £270,752.

The consensus view is that UK house prices will be softened in the coming months due to these changes.

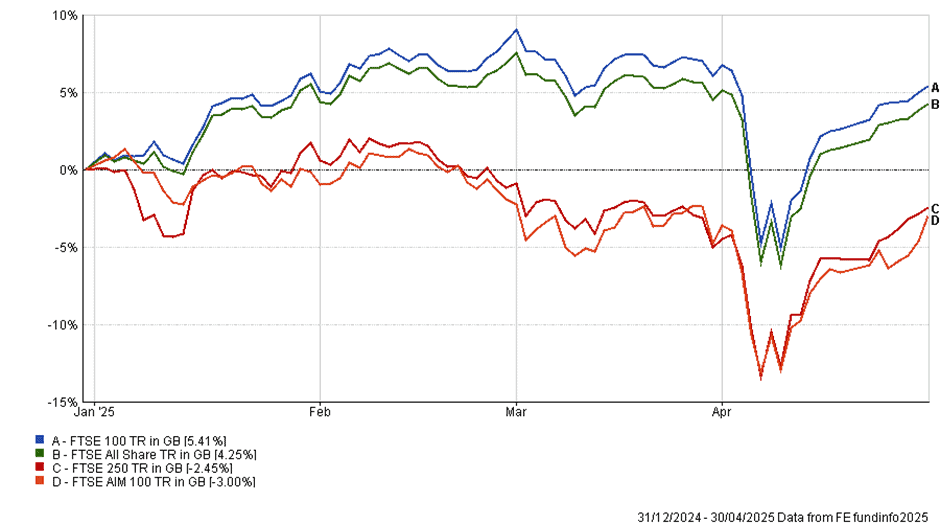

YTD performance of major UK stock market indices

April was a volatile month for global stock markets, and the UK was no exception. In response to Trump’s Liberation Day announcements, UK markets tumbled with the FTSE All Share losing over 10%. Towards the end of the month, the index had largely recovered and ended the month 4.25% positive year-to-date.

Amid the calming of investors nerves and the increasing prospect of a May interest rate cut, the FTSE 100 posted its 11th consecutive winning session towards the end of April, its longest winning streak since December 2019. The rally was largely led by strong performances in the Healthcare and Consumer sectors – which were hit the hardest by the announcement of Trump’s tariffs on 2nd April.

Smaller companies, represented by the FTSE 250 index, witnessed similar declines and a subsequent recovery towards the end of April. However, due to its poor performance since the beginning of the year, the index remains negative year-to-date (down 2.45%).

Looking forward, interest rate cuts may provide a much-needed boost to the performance of small-mid cap companies in the UK.

| Yield as at 02/05/2025 | YTD change | |

| 2Y Gilt | 3.77% | -13.87% |

| 10Y Gilt | 4.42% | -3.24% |

UK bond yields and YTD change as at 02/05/2025

Gilt yields continued their decline last month as investors priced in interest rate cuts from the Bank of England. The shorter end of the yield curve fell further last month, again reflecting the risk of inflation picking back up over the longer term.

–

Europe

April proved to be a turbulent month for European equities, driven by the announcement of widespread tariffs on US imports; ongoing geopolitical uncertainty regarding the Ukraine conflict and the advancement of notable changes to fiscal policy and increased defence spending in Germany.

President Trump’s announcement of sweeping US import tariffs marked the first week of April. The tariffs were more severe than investors had expected; the global equity market reaction was decisively negative, and Europe was no exception. The Stoxx Europe 600 index fell by 13% following the announcement, virtually wiping out the gains made in Q1.

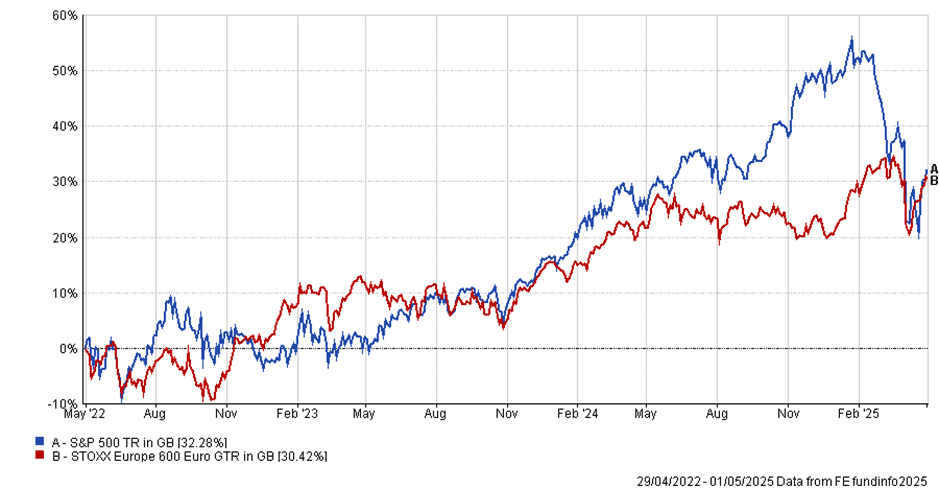

A temporary suspension of the tariffs to allow for ongoing negotiations offered a slight reprieve and led European markets to rebound. At the time of writing, the Stoxx Europe 600 index has recovered over half of its losses, sitting at an 8.16% YTD gain in GBP terms (outperforming the S&P which sits at -9.99%).

Nevertheless, the renewed investor confidence that buoyed European equities in Q1 has been significantly undermined by the uncertain outlook regarding tariff negotiations.

Whilst the Stoxx Europe 600 is currently outperforming the S&P 500, it may be wise to remember that this is over a short period of time and that the European index has only outperformed the S&P 500 in three out of the last ten years. Excluding this year to date, the magnitude of outperformance was much greater than the underperformance as well.

| Year to Date | 2025 | 2024 | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

| S&P 500 TR in GB | -9.99 | 26.73 | 18.58 | -8.25 | 29.34 | 14.12 | 25.65 | 0.96 | 10.62 | 32.67 | 6.58 |

| STOXX Europe 600 Euro GTR in GB | 8.16 | 4.46 | 13.79 | -5.04 | 17.74 | 4.07 | 20.48 | -9.22 | 15.66 | 18.57 | 4.62 |

| Excess S&P 500 Return | -18.15 | 22.27 | 4.79 | -3.21 | 11.60 | 10.05 | 5.17 | 10.18 | -5.04 | 14.10 | 1.96 |

*Discrete Calendar Year Performance of the S&P 500 TR against STOXX Europe 600 Euro GTR, both hedged back to GBP (Source – Financial Analytics)

The proposed 20% tariffs on European exports continue to pose a significant risk to Europe’s economy, which relies heavily on export-focused industries. According to a report from Jefferies, €400bn out of €500bn of US exports from Europe will be exposed to tariffs.

The permanent imposition of 20% US import tariffs from the US has the potential to damage European growth prospects in 2025 and perhaps even tip the region into a shallow recession.

The three areas most at risk, and which Europe relies on heavily, are the auto sector, the luxury goods sector and the alcoholic beverages sector.

The European Central Bank confirmed a further interest rate cut of 0.25% in April, which places the benchmark rate at the upper boundary of the ECB’s estimated neutral range of 1.75% to 2.25%. ECB policymakers, including Olli Rehn (governor of the Bank of Finland), have indicated openness to further rate reductions, potentially below the neutral level, to stimulate economic activity amid external shocks such as the ongoing trade war.

The EU is amongst the many regions threatening to impose retaliatory tariffs on the US – no action has yet been taken and negotiations are currently at an uneasy standstill, whilst the US administration first tackles negotiating agreements with Mexico and Canada.

The EU has continued its pursuit of big tech with more fines against Apple and Meta, which will not please President Trump (although the Federal Trade Commission are also launching anti-trust cases against Meta and Alphabet – a bit of “I will tell my own children off, but you cannot” from the US).

All of this uncertainty continues to weigh heavily on the bloc, in addition to existing structural vulnerabilities including ongoing weak economic growth and the ongoing war in Ukraine.

The US administration has been making continued diplomatic efforts to end the conflict in Ukraine, albeit with a more transactional approach, linking future US support to strategic access to Ukraine’s natural resources through the recent unveiling of a joint Reconstruction Investment Fund.

However, Trump’s recent threats to withdraw support from Ukraine and NATO have alerted Europe to its reliance on the US and that increased spending is required to fund a new military deterrent independently.

The European Union has already launched a €150bn bond programme in pursuit of this goal. In Germany, the chancellor-in-waiting Friedrich Merz has already pushed bills through Parliament to lift the deficit cap on defence spending and to fund a massive domestic infrastructure spending programme.

This is a clear shift from the previous approach to fiscal deficits that have severely restricted investment in the country, which should benefit equities in the medium-term. These measures have been reflected in European defence stock performance, with Germany’s Rheinmetall and Italy’s Leonardo both performing well.

An end to the war in Ukraine may weigh on earnings for companies such as Rheinmetall as they have been a large supplier of equipment and ammunition for Ukraine. In this event other industries may benefit from the peace, such as construction companies who will lead in the reconstruction efforts and banks, who will likely finance these efforts (loan growth in European banks has been flat for a while and this would help grow these volumes).

Another reason for cautious optimism is that a survey by Bank of America found that the proportion of fund managers identifying European shares as undervalued (relative to global peers) reached its highest in six years. Following years of underperformance, as shown below, the forward price-to-earnings ratio of the Stoxx Europe 600 is a third lower than the equivalent valuation measure for the S&P 500, making it potentially attractive for long-term investors.

Three-year performance of the S&P 500 against the Stoxx Europe 600 index, in GBP terms. (Source – FE Analytics)

Although there is a discount between the two regions, it is worth remembering that it may be for a good reason – a chair with four legs is more valuable than a chair with three legs, so the three-legged chair will undoubtedly be available at a discount.

European equities have shown modest resistance amid significant external pressures as the events of this month tested the resilience of the global equity markets. The combination of proactive monetary easing, ambitious fiscal stimulus, and structural shifts in defence policy may position the region for renewed investor interest.

However, as seen in the week following “Liberation Day”, this hinges on the successful negotiation of the reduction of tariffs, which have the potential to wipe hard-won gains quickly in the short term and causing long-lasting damage to the economy in the longer term.

–

Robert Dougherty, Investment Specialist

Ryan Carmedy, Associate IFA

Harry Downing, Associate IFA

Fiona Chegwidden, Graduate Trainee IFA

May 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested. Data is correct at time of writing and cannot be guaranteed.