1st August 2025

Markets are looking for the winners and losers of the trade agreements and not focusing on the top down macro-economic view. This is good for markets in the short term but it does hide some of the risk – after all, economies have been weakening since the tariffs announcements in April and we are only early on in the innings.

Japan and Europe reached a trade agreement with the US whereby the tariff rate on their goods was implemented at 15% and they would also agree to invest hundreds of billions into the US. Europe did not respond with its own tariffs on the US, which is being debated as a good or bad idea.

In our view we see it as being a good thing. A tariff is essentially a value added tax on the end consumer. Therefore if Europe tariffs the US goods it imports, this would add to the cost European consumers pay. The US would also certainly retaliate as well. However, it could be seen as rolling over and letting the US do what they want.

This month the drama continued, with Musk and Trump’s relationship deteriorating further, Rachel Reeves looking sad in parliament and Jerome Powell being accused of fraud.

Despite all of this, the US equity markets continued to power through the news. Nvidia became the first company to reach a market cap of $4 trillion market, an impressive feat given its market cap at the start of the decade was just under $150 million.

Valuations are high but there are tailwinds that mean the AI dominance of the US is likely to be somewhat protected. We talk more about this later on in the article.

President Trump continued to attack Fed Chair Powell, pushing for him to lower rates by three whole percentage points. This is not the first time a US President has pressured a Fed chair to change interest rates, but markets are not pricing in much threat to the Fed’s independence at this point.

In the extreme event where rates were cut by three percentage points at once, this would likely push up the longer end of the yield curve as investors would expect inflation and rates to be higher in the future – helpful for US debt in the shorter term but more damaging to consumers and the economy over the long term. The Fed can influence the short end of the curve but the long end is controlled by the market.

The UK experienced ‘unexpected’ economic data this month and Rachel Reeves delivered a rather benign annual Mansion House speech on regulation in the financial markets. In order to make the UK more attractive for financial institutions to do business, the government is exploring how to repeal some of the regulation put in place after the Great Financial Crisis.

Labour cuts to certain benefits were repealed as members of the party strong armed Keir Stramer into putting them back into place, giving the UK even less wiggle room in which to cut costs and grow. Markets are thinking it looks even more likely that we will see tax rises in the next Budget. The IMF has lifted its latest economic growth forecasts for the US, China and the Euro area relative to their forecasts in April, but the UK forecast has declined further.

Japan continues to face political uncertainty with the leading party losing its majority in the government and more extreme parties gaining seats. Many commentators argue the Prime Minister has been focused on tariffs when the population care about inflation and wages, and on the tariff front he has not made much progress.

Although the auto sector in Japan is coming under pressure, we still see other areas of advancement which make Japan an attractive region for investment when valuations elsewhere look high. One positive for Japan has been that a trade deal with the US was reached, removing some uncertainty.

–

Areas of focus

- Investors continue to demand a premium for holding the long end of the yield curve, with global yields on the rise.

- Longer duration corporate credit continues to look risky. The higher interest rate sensitivity could be beneficial in a recessionary environment, but this would be offset by the higher credit risk.

- With the US Dollar weakening, global investors may think about hedging their exposure. However, high hedging costs for some investors will result in minimal benefits.

- UK gilts look promising relative to US treasuries, while European government bonds in the lower interest rate environment sit somewhere in the middle.

- Very specifically, investors are finding Romanian government bonds attractive. Despite being BBB rated, they are yielding the equivalent of a BB bond.

- Emerging market local currency debt continues to look attractive given a weakening US Dollar.

- While every year for the past five years has been “the year” for UK smaller company stocks, and history shows that small cap stocks tend to outperform large cap stocks, in this new environment it will be harder for small companies to consistently deliver strong returns.

- Broadly, technology companies have led the way this year again but we are starting to see dispersion, with Nvidia performing strongly while Tesla and Apple struggle.

- Global banks have seen their earnings pick up strongly as their clients have traded more in the volatile market environment.

–

Asset Class Returns

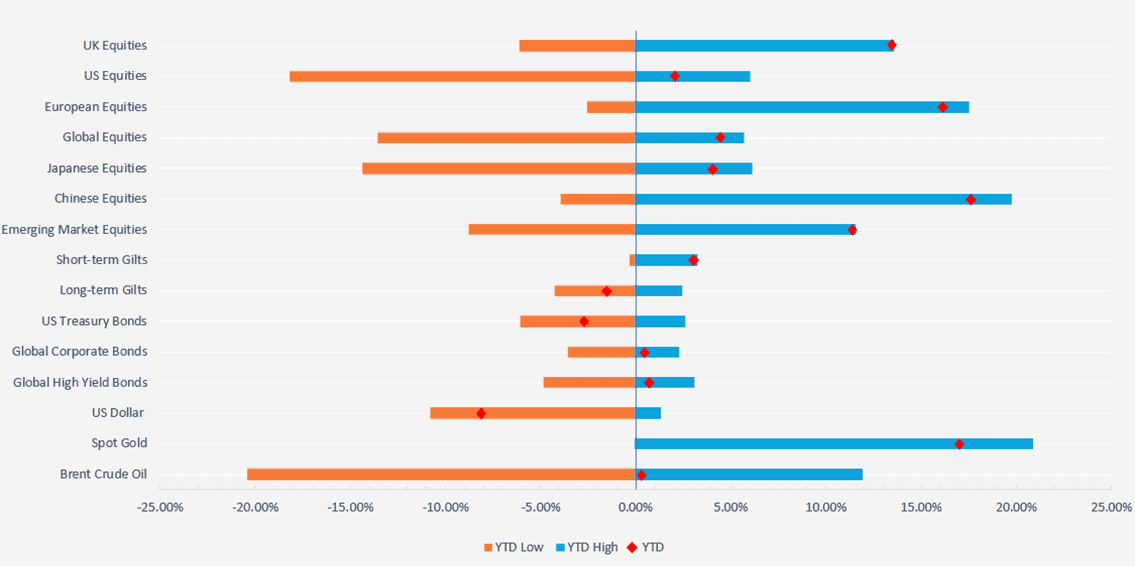

Selection of assets 2025 YTD returns and range of returns as at 30/07/2025 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Data from FE Analytics and MarketWatch

–

US

This month technology and financial companies dominated the headlines. We start with technology companies and why everything seems to be falling into place for the main drivers of the US market, before moving on to the big financial companies in the US and the broader macro and long term thinking.

All the talk around a weakening dollar has missed a key point for US company earnings. That is, US companies which earn revenues overseas will benefit from a weaker US Dollar when they convert their foreign currency back into US Dollars. This positive translation effect is giving companies an earnings boost at a time when any missed earnings will be heavily scrutinised. The US Dollar index has fallen around 9% this year, its worst start to a year since 1991.

The big question is who is likely to most benefit from the weaker US Dollar. The answer, unsurprisingly, is mostly US tech companies.

Data from Goldman Sachs shows foreign sales made up 28% of S&P 500 revenue in 2024, with the technology sector generating 56% of its revenues overseas. At the start of the year the market consensus was for domestically-focused companies to benefit from a rebasing of manufacturing into the US, but companies with the highest international revenue exposure have outperformed more domestically-focused companies by 7% in US Dollar terms year-to-date.

There are a lot of factors that keep supporting technology companies’ momentum. This has been a structural shift over a longer time and this is more reflective of what consumers want and need. By this I mean asset-light businesses such as Meta are able to be more responsive to the changing environment, relative to asset-heavy businesses such as automakers.

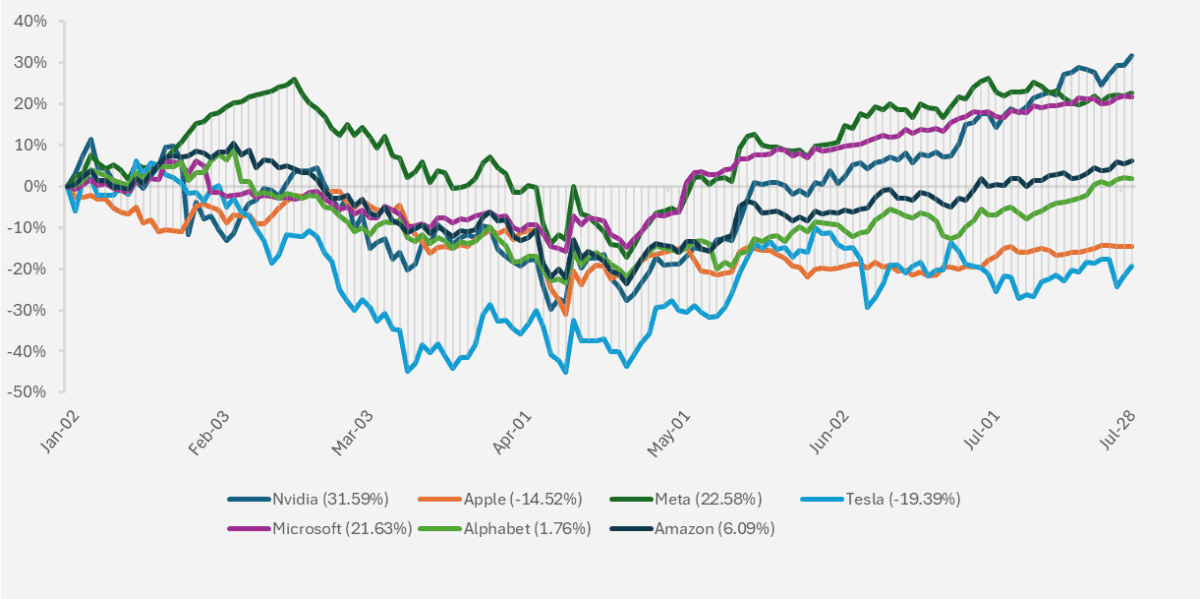

We have seen big swings in values in the “Magnificent Seven” technology companies this year, with a large variance in performance between the group (see chart below).

Chart showing YTD performance of the Magnificent Seven US Stocks (Source – Watson French with data from Investing.com. Data as at 29.07.2025).

Nvidia jumped to take the top spot as the most valuable company in the world, as the demand for their high-margin GPUs to power AI models continues to be strong.

At the other end, we have seen three notable laggards in the group. Tesla has performed the worst this year with declining sales, political problems with CEO Elon Musk’s foray into the world of politics and competition from other EV makers, notably from China. At the start of the year Tesla’s valuation was greater than the next 35 largest automakers. A lot of this is an ‘Elon Musk premium’, but most of the company’s earnings are priced far in the future and are based on robotaxis, AI and humanoid robots – areas in which they are either not profitable or which do not commercially exist.

Apple has struggled to gain traction with delays in the rollout of their AI offering. The company has also come under pressure from the trade war and US tariffs on China. This highlights the above point about how asset light businesses are better able to cope with a dynamic environment than asset heavy businesses. Rumours of a new device coming from OpenAI also cast doubt on whether, in the future, we will even continue to use mobile phones as we do today. That’s not to say that Apple won’t exist in the future, but after all, big names in the past like Nokia and Motorola don’t enter the conversation much these days.

Finally, Alphabet has struggled as investors believe the business is too fragmented and that their lucrative search engine, Google, will be replaced by AI in the future.

This performance may be short term but it highlights an important point – that there is a natural churn in markets, through which we start to find out which companies will be the winners and have positioned themselves best for the evolving tech industry. We will likely see a new acronym in the future for the biggest and best performing companies of the time.

The last acronym we had was for the FAANG stocks, one of which was Netflix. At the time Netflix was one of the hottest stocks, but now its popularity has waned as others have taken its place.

Another positive for US technology companies is that the recent tariffs are on goods and not services. It is also much more difficult to change where goods are manufactured than it is to change, say, a piece of software code or to update features on an app.

That’s not to say there are not risks with technology companies. The trillions of dollars being spent on data centres may turn out to be wasted dollars due to overcapacity, much like the telecom overcapacity in the 90s. There are major differences in how this is being funded and the more diverse nature of big tech’s businesses today, but it is a risk none the less.

Pivoting from technology companies, big banks and other financial institutions have delivered strong earnings growth in the volatile trading environment. Their clients have engaged in more trading and rebalancing, leading the companies to earn higher fees from this activity. At a time when investment banks’ capital markets activities have waned (equity and debt financing), their ability to capture fees from clients’ trading has helped to support their valuations. That said, with markets riding the strong momentum we are seeing capital markets activity pick up.

One risk for banks is the direct competition they have with private credit and equity. We will speak about the rise in private assets in the next asset commentary.

From a secular point of view we see the biggest US financial institutions being big beneficiaries of the new environment. Growth is high, leverage is being used to finance this growth and technology adoption is picking up. The companies that are able to adopt and implement AI are poised to outperform over the long term. This should increase their efficiency and productivity, lower their costs (smaller labour force, less time spent on menial tasks and more on value enhancing tasks) and thus improve their margins.

We are already seeing examples of this in practice. A report in June detailed that the US investment bank Morgan Stanley used a new AI tool to translate old lines of code into plain English for its developers to use to rewrite the code. They estimate the AI tool read through nine million lines of code, saving the firm’s 15,000 developers roughly 280,000 hours of work.

If we use the average software developer hourly wage of $52 as a proxy, based on this value the firm saved $16.24 million by using AI for this task. Not only this but the developers are able to spend their time on value-added tasks, turning the opportunity cost of doing the initial job into an opportunity gain.

We expect larger companies to continue to perform strongly relative to smaller companies. The reason being that the cost of adopting the technology is high and larger companies have deeper pockets to be able to do this. Smaller US regional banks have not seen the favourable performance the big banks have had and we think this could persist. We see a new barrier to entry rising for mature industries, and in this the potential for consolidation or a reduction in competition.

We saw yet another tariff announcement from the Tariff Man this month (among many others at the time of editing this piece), with pharmaceutical companies facing 200% tariffs if they fail to reshore production to the US. A caveat – they have been given up to a year and a half to do this.

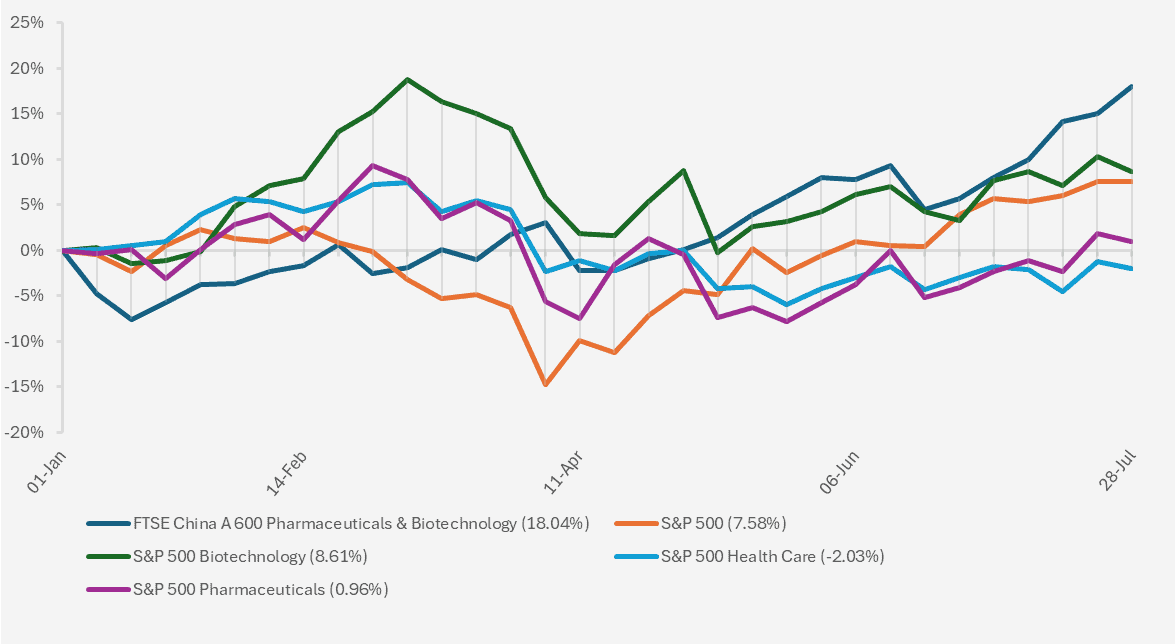

YTD performance chart of US & Chinese Pharmaceutical, biotechnology and healthcare indices (Source – Watson French with data from FE Analytics. US index returns are in US Dollars and the FTSE China return is in Hong Kong Dollars. Data as at 29.07.2025).

Despite this, indices for the US biotechnology and healthcare sectors did not fall. The likely reason for this is that because these companies have been given a year and a half to bring production back to the US, investors are betting that the tariffs will eventually be reduced or removed entirely.

We see many risks for the US pharma and biotech industry over the short and long term. The first is that if these tariffs are implemented, a 200% increase is huge and will significantly impact revenue and margins. The effect will be felt differently depending on the type of company (see below). The net result will be US companies losing their competitiveness and drugs being less widely available.

The second risk is a longer term risk which is difficult to quantify. With grants to universities being withdrawn and potentially higher fees on patents, this impacts the ability for groundbreaking research to be conducted and inform US biotech companies drug development – US companies rely on this research. Drug development takes years (including the trials before the drugs are approved for the market), but prior to this is the academic research stage, which takes just as long.

Couple this lower level of research which will result from stricter immigration policies (the best and brightest researchers not being in the US) and this will add to US companies falling behind. We won’t see this in markets or earnings anytime soon, but it is a long term structural change. To further strain the situation the Secretary for Health and Human Services (Robert F. Kennedy Jr) is a vaccine sceptic and has made big cuts to departments in the FDA. To wrap a bow on it, we see a lot of uncertainty in the sector.

That being said, AI has a huge part to play in drug discovery and the healthcare industry in the future and could revolutionise the industry, shortening research times and speeding up drug development.

On the other hand, Chinese companies look poised to benefit. With lower production and development costs and many big global pharma companies facing a patent cliff, Chinese companies have become a lot more competitive and this has been reflected in recent share price performance (see chart above). Big US and UK pharma companies have begun utilising Chinese drugs and we only see this increasing further.

Back to our point on tariffs and how it will affect different companies. In our view, big pharma companies involved in the development and patenting of new drugs will likely be more insulated than generic prescription drug companies (those that sell paracetamol etc.).

The former companies have pricing power over their products as they are unique and have significant Intellectual Property value. The latter already work on small margins and low pricing to remain competitive and so a 200% increase is not something they can absorb easily.

Markets have been pricing in a scenario that tariffs will not meaningfully affect the headline inflation figure and as we have not seen it yet, that we won’t. Again, we reiterate that someone has to pay the tariffs and so there will be some sort of price pressure. This could be a one off price increase which is absorbed into the economy and then inflation will drop back down. Alternatively it could be a continued and sustained price increase.

The latest CPI report for June showed an annualised rise of 2.7% and 2.9% for core inflation (which excludes volatile energy and food prices). The headline figure was slightly above expectations.

The debate comes down to whether tariffs, essentially a tax on goods, will result in companies increasing their prices or taking the hit themselves. Either way this is not good for consumers or for company earnings. The recent data shows prices on products such as household goods and toys rose while smartphones, having previously declined, were flat. Making it more difficult is the ambiguity in business leaders’ comments on pricing strategy. Rather than giving clear messages they are using phrases such as ‘strategic’ and ‘dynamic’ pricing.

The effect of tariffs will guide how the Federal Reserve thinks about any upcoming interest rate actions. Markets are pricing in potentially two cuts, but if inflation stays sticky or shows signs of increasing we can plausibly see no rate cuts materialising this year.

Tariffs prices will take time to pass through to the real economy for several reasons. The first is whether businesses decide to increases prices; some will take the opportunity to do so regardless of tariffs.

The second point is that businesses, in anticipation of tariffs and difficulties in getting stock, built up around three to four months on inventory which they are currently working through. When this runs out we will see inventory purchased at higher prices and also likely higher transport costs, owing to political tensions in the Middle East and the recent attacks on ships by the Houthi Rebels.

We saw second quarter GDP increase at an annual rate of 3%, up from the 0.5% contraction in the second quarter. This is misleading, as the first quarter saw a rise in imports to get ahead of tariffs (detracting from GDP), with the second quarter seeing a rise in exports (or a fall in imports), adding 5% to the GDP figure. We will therefore need to wait until the end of the year and the first half of 2026 to get a clearer picture.

The last point to note is that with tariffs moving around, being paused, resumed then paused again businesses don’t know what to do. A risk here is businesses anticipating tariffs and increasing prices anyway.

In other US news, individuals who had previously paused payments on their student loan debt will now have this reflected in their credit scores. In our view this is a hidden risk in the system for several reasons and will pressure earnings and borrowing in the months to come.

With first time buyers struggling to get on the property ladder already, lower credit scores will prohibit many of these consumers from securing a mortgage before their actual earnings are even looked at.

Data from Harvard’s Joint Centre for Housing Studies shows that for a median-priced US house, a house buyer would need to earn $127,000 pa to pay the monthly mortgage payments, up from $79,000 pa in 2021.

With interest rates expected to remain high for this year, the housing market looks to be locked in for a while (a win for rental landlords, however).

Higher credit scores also mean high borrowing costs on other forms of debt. This makes debt harder to access, which could pull down spending and consumption. This also increases the proportion of disposable income spent on financing costs, again leading to potentially lower spending on other goods. This is not a recessionary event on its own but it does add fuel to the fire. Markets seem to be mostly ignoring this and again, it represents another downside risk that should be priced in.

Our final point on the US this month is to comment on the idea of a non-independent Federal Reserve. If we did see political influence in the Federal Reserve, it would certainly add a few percentage points to the inflation figure in the long term and raise borrowing costs in the treasury market.

However, even if Jerome Powell was removed from his position as the Fed Chairman and President Trump appointed someone who was more in line with his views on dramatically lowering rates, it is the Federal Reserve Open Market Committee which votes on interest rates cuts. These votes come from seven Federal Reserve Governors and five Federal Reserve Regional Bank Presidents. Therefore, the rest of the committee would need to vote in favour of rate cuts as well, which seems unlikely.

–

Europe

The Euro has strengthened considerably this year, gaining over 11% versus the US Dollar at the time of writing. The reasons for this are threefold.

The first is that investors are looking for alternatives to the US Dollar because of damaged confidence in the dollar, owing to fiscal concerns and geopolitical risk. The second is the potential for bigger spending in the bloc (certainly in Germany) pushing up yields and making the region more attractive for both debt and equity investment.

The third is a somewhat more indirect consequence. Smaller countries also want to hedge their US Dollar exposure but this tends to be more expensive for them to do. Many of the smaller currencies are not priced directly against the US Dollar, but are priced through “cross rates”. A cross rate is a transaction between two currencies (not involving the US dollar), that are both valued against a third currency (almost always USD) as an intermediate step. So for example, if you wanted to exchange Mexican pesos for Chinese renminbi, you would exchange pesos for dollars and dollars for renminbi.

Firstly, this can add to transaction costs, but secondly, the liquidity tends to be lower, leading to wider spreads and a greater cost. To get around this, companies and institutions are not hedging by selling the US Dollar but buying Euros as an alternative.

A stronger Euro presents both problems and benefits for the bloc over the next few years.

A stronger Euro makes imports cheaper. With the latest CPI reading in June for the bloc coming in at 2%, there is a risk of deflation or persistently low inflation. For nominal growth and corporate earnings this is a weakness.

Cheap goods from China flooding the EU market because of US tariffs will also add to the deflationary pressure. The EU has already lowered interest rates eight times to 2%. The ECB could reduce rates further, which would weaken the currency and make the bloc more attractive for financing, but the risk of tariffs is still a concern for prices. In their July meeting the ECB held off lowering interest rates, which was what markets had expected.

On the other hand, a stronger currency makes exports less competitive. The combination of a strong currency and 15% tariffs on exports could weaken companies reliant on overseas trade. With growth in the bloc picking up but still sluggish, this is not a good scenario. One of the biggest losers in this scenario would likely be automakers.

For the past few months we have talked about the idea of a joint Euro bond and the benefits and drawbacks of issuing one. Another example on the issue was a recent quote from German defence minister Boris Pistorius where he said “Eurobonds mean that those who have already done or are doing their homework pay for what others don’t do”. With 27 EU member states, agreements can be hard to come by and likely further cements the US Dollar and treasury markets as the global safe haven (as we said last month – frayed at the edges but not broken).

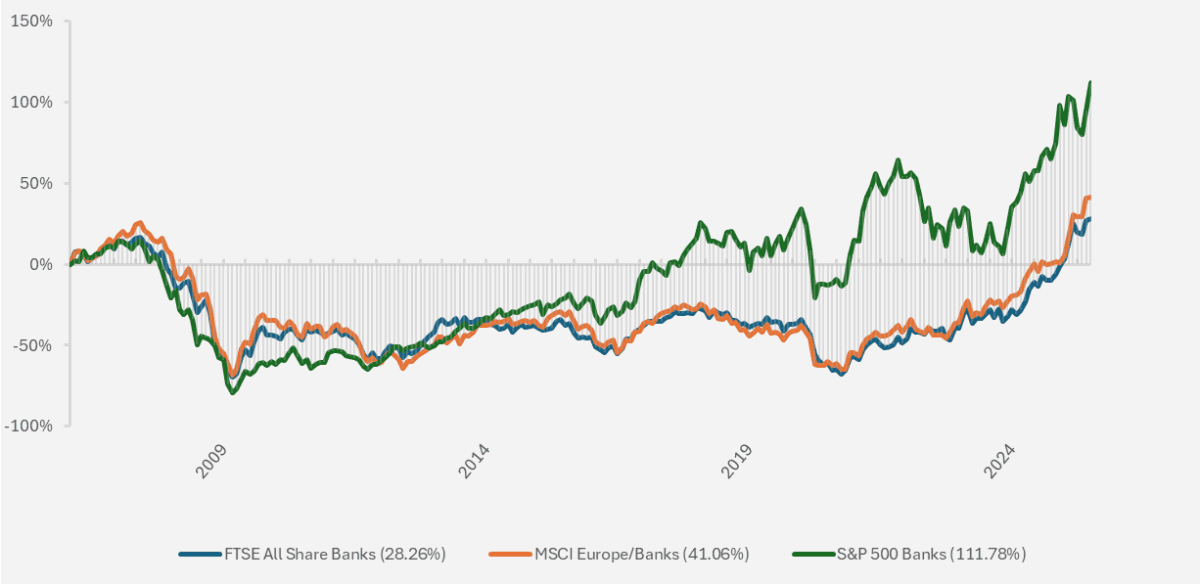

European and UK banks have lagged their US counterparts in terms of value since 2014 (see chart below).

Chart showing long term performance of US, European and UK banks (Source – Watson French with data from FE Analytics. All returns are in local currencies. Data as at 29.07.2025).

The US has more liquid capital markets, lighter regulation relative to the UK and Europe and more innovative companies with greater financing needs. Couple this with issues in the UK since Brexit and fragmentation issues in the EU market, and it’s no surprise that big US companies have dominated the global landscape. We see positive factors helping to change this though.

Loan growth, a major part of banks’ business, has finally started picking up after years of benign growth. We see potential reconstruction efforts in Ukraine, German fiscal spending and a potential lighter touch to regulation helping to boost banks earnings. Certain European banks are reassessing their footprint in the EU with the aim of not needing to be present in every country, but focusing on their core areas and making these profitable. After years of underperformance we think the valuation gap could narrow.

An EU trade agreement with the US, setting a tariff on goods at 15% (excluding steel and aluminium, which is presently at 50%,) has reassured markets and they are taking this in their stride.

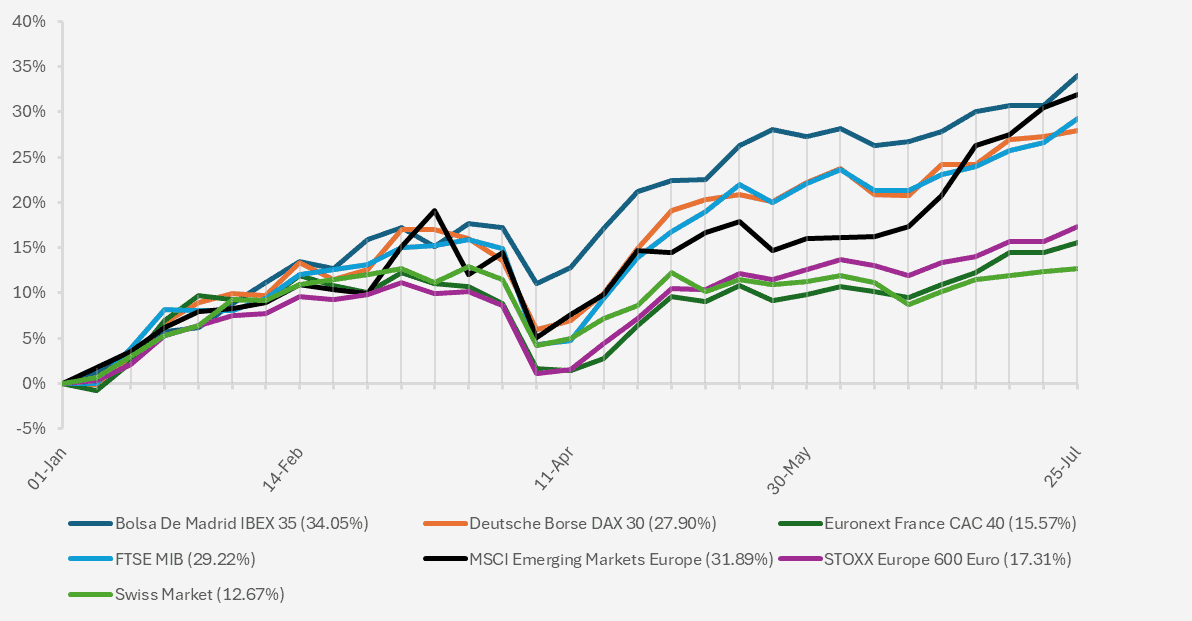

All European stock market indices are positive for the year to date, but we are continuing to see dispersion between individual countries continue. Spain, Germany and the emerging European economies (Greece and Poland for example) are continuing to outperform while the French and Swiss markets lag. Although they are grouped together and have a singular central bank to set interest rates, each country has different dynamics and economic situations. France, for example, has persistent fiscal problems with no solution in sight, whereas Germany has made headway in this space. The Swiss market faces tariffs of 39% and negative yields on some of its government debt.

European members of parliament have voiced their displeasure regarding the EU trade agreement with the US. With voices from different member states looking to protect different industries and needs, in Europe sometimes the least-worst solution is the best.

Chart showing YTD performance of major European stock market indices (Source -Watson French with data from FE Analytics. Returns hedged to GBP. Data up to 25.07.2025).

Our last point on Europe is to touch on Ireland, as we briefly mentioned in last month’s commentary. Ireland has a huge trade surplus with the US (i.e. the US has a trade deficit) and 61% of Ireland’s exports to the US in 2024 were in drugs and medicines. The small town of Westport in Ireland produces the world’s entire supply of Botox.

Tariffs of 200% on these products would be hugely damaging for Ireland. If companies reshore their production to the US, unemployment would increase and tax revenue would drop. Ireland would then need to rebuild parts of its economy. Ireland has favourable corporate tax rates in place for pharmaceutical and technology companies and the tax revenue they do pay has contributed to an overall budget surplus for Ireland.

The price of medicines and medicinal ingredients would also likely increase, as well as a fall in net earnings for the pharmaceutical companies such as Pfizer and Johnson & Johnson that are based there.

–

UK

I am sorry but we attempt to state the facts in this commentary, and it has been a dreary month for the UK on the economic data reporting front. A lot of unexpected events for the UK this month: employment, inflation and GDP growth. I say unexpected as this is what the media is portraying the data as, but it certainly was not.

UK inflation picked up to 3.6% in June, up from 3.4% in the previous month and a large margin away from the Bank of England’s 2% target. The biggest contributors to the figure were transport costs. The figure for services inflation, which is arguably more important for the UK given the service-based nature of the economy (which accounts for 80% of GDP) held high at 4.7%. We still view some of this data as short term due to the higher employer burdens introduced in April, which are still filtering through the economy.

At the same time the unemployment rate ticked up to 4.7%, up from 4.6% and above expectations, and average weekly earnings picked up by 5.0% over the quarter to May.

GDP growth contracted in May by 0.1%, the second month in a row in which GDP declined. The first three months of the year were characterised by strong growth of 0.7% due to the front loading of exports in advance of the proposed tariffs.

Data also showed that growth in the UK private sector business activity slowed in July. While still in expansionary territory, the fall is reflective of businesses beginning to cut jobs and slow on the number of orders filled due to the higher taxation and wage burdens placed on them from the April NIC and minimum wage increases.

It was not unexpected that the economy would come under some strain, with tariffs higher than when we started the year, continually higher interest rates and a barrage of higher costs for businesses since April. The main implication of this is what the Bank of England will do with interest rates. Unlike the Federal Reserve they do not have the dual mandate of maximum employment and inflation at 2%, but they do have an objective to support the government’s economic objectives.

In that respect the threat of a slowing economy does mean that the Bank of England needs to step in to support the UK economy, as this is the government’s main priority at this time. This does risk inflation picking up further, but with a weak economy and tight fiscal constraints there are a lack of options to spur growth.

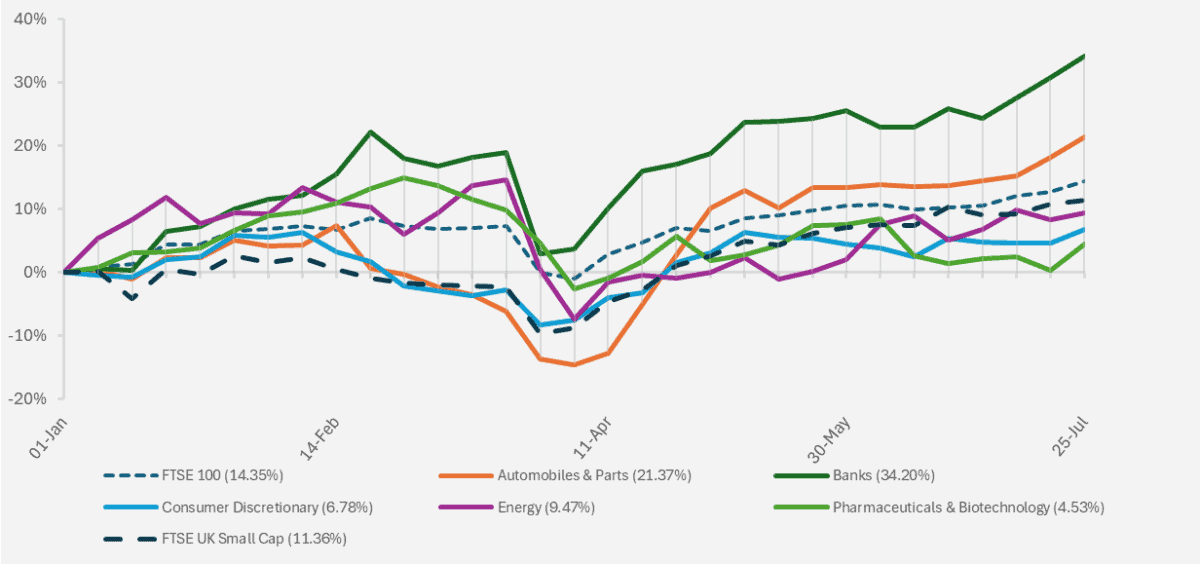

Nonetheless there are potential positives for the UK stock market, mainly in the financial area. High interest rates have continued to help boost profits in this sector and over a longer time horizon their growth should be secular, as it is in the US.

The growing risk for the City of London is that the Chancellor will go after them with increased taxes to create room for the economy to grow. With financials continuing to drive the UK stock market higher (see chart below) this would represent a headwind to earnings and investment.

One of the most effective tools the Labour government has to increase growth, without borrowing (upsetting the bond market), increasing taxes (upsetting consumers and businesses) or reducing spending (upsetting… well everyone) is to cut the tiresome and difficult regulation stopping businesses from growing and investment. Rachel Reeves’ Mansion House Speech didn’t really touch the sides on this.

This is not a problem just in the UK but also in Europe and is one of the reasons why markets place a higher valuation on US equities – it is just easier to do business over in the States.

Although regulation was put in place after the GFC for a clear reason, some of this has become overburdensome and has gone too far. Regulation needs to be looked at to see if it is actually effective.

For example, after the GFC banks had to ring fence their riskier investment banking divisions from their relatively less risky retail banking divisions. Banks can operate in the repo market internally between divisions to provide lending with very low or even negative haircuts (essentially no cost to lending). Therefore it may seem the banks activities are ring fenced, but in reality if the retail arm is lending to the investment banking arm at no cost, is it really protecting the retail depositors?

One area Labour is looking to target is the cash ISA allowance. Around £300 billion is held in cash ISAs and unlike the US, most UK consumers do not invest in the stock market. With an annual GDP of £2.56 trillion, this value represents over 11% of GDP and could be used more efficiently. Critics to the plan argue that this money wouldn’t necessarily flow into the UK stock market. More importantly is that the money flows into a stock market, where long term returns tend to be positive in real terms relative to the interest rate on cash.

Over the long term this matters as it creates a wealth effect. That is, if consumers’ wealth is growing by a greater amount through stock returns, they will feel the need to save less and spend more, creating growth in the economy. This is something the US excels at but Europe, the UK, China and Japan lag. To create this effect requires long term planning, incentives and safety nets.

Another example of the struggles facing the UK market this month is the IPO market (Initial Public Offering). Shein, the Chinese online fashion retailer had filed a draft prospectus for listing on the Hong Kong stock exchange. This is despite the company applying for a listing on the UK market… 18 months ago. The FCA has not been accepting of the risk disclosures described in the company’s prospectus, and when this was finally accepted the Chinese regulator did not agree.

Despite the doom and gloom, UK markets continued their positive returns this year, with smaller companies continuing to lag their large cap counterparts. Banks have led the way and we expect this to continue.

Chart showing YTD performance of UK stock market indices and select sectors. (Source – Watson French with data from FE Analytics. All sectors are FTSE All Share sectors. Data up to 25.07.2025)

–

Robert Dougherty, Investment Specialist

August 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested. Data is correct at time of writing and cannot be guaranteed.