1st July 2026

Volatility is, well, volatile and high. Negative earnings are driving markets higher, exciting new industries and companies dominate news flows, markets are becoming more and more concentrated and investors are making rational arguments excuses. All the while bond yields have risen and so the cost of borrowing and financing growth have moved upwards. We are continuing to see complacency in the market. Markets are supposed to grow over the long term, but it is the pace of growth and sustainability that concerns us.

There are some long term structural themes continuing to play out here, but at the same time we are in a casino environment. If you strip out the energy and AI sectors from the S&P 500, in US Dollar terms the market is actually in negative territory. Kevin Warsh led his first Federal Reserve meeting and while the Fed opted to hold rates, members were more hawkish on possibly increasing rates later in the year. Stocks moved higher for much of the month but the reality did start to take hold with some big downwards moves later in the month, including from the newly minted SpaceX.

Keir Starmer stepped down as Prime Minister and a new leadership race opened up, with newly elected MP Andy Burnham looking the likely front runner. Not long ago Burnham said we shouldn’t be driven by the bond market, but he has since changed his rhetoric as the possibility of becoming prime minister becomes a reality. Bond yields fell on the news of Starmer stepping down but we expect volatility in yields to be elevated as markets digest political activity over the next month. This is Britain’s seventh Prime Minister in ten years and this sort of instability brings both a political premium on debt and erratic policy making, leading to anaemic economic growth. It is possible that Rachel Reeves will not be Chancellor for much longer, which puts the fiscal rules under pressure. Expect a bumpy road ahead.

Also, although bond yields fell, if we take a 10,000-foot view they are still highly elevated compared to before the start of the war in Iran, despite oil prices falling as an end to the conflict looks more promising and sustained.

It wouldn’t be very British of us if we didn’t at least try to talk about the weather somewhere in the commentary. There have been more headlines regarding the weather phenomenon known as El Nino, which could boost global temperatures and drive more extreme weather. Without going into detail, El Nino is a natural phenomenon whereby changes in wind patterns in the Pacific push warmer water across the Pacific Ocean. While it is not guaranteed and the timing and impacts vary, a possible outcome is that South America, South East Asia and Australia will see hotter and drier weather which increases the risk of droughts and wildfires. India and South Africa can also experience drier weather, while other areas such as East Africa and the southern parts of the US can experience higher rainfall and increased risks of flooding.

Historically El Nino has pushed food prices higher as crops fail and trade is disrupted. Like energy prices, central banks’ use of monetary policy to control food inflation will be limited (people need to eat and keep warm, and so higher interest rates cannot stop demand for food) and one of the key points economies will have to come to grips with is higher and more volatile inflation. Climate change is a key structural change for investment markets.

Despite yield increases and talks of higher interest rates, we reiterate that 2022 and the yield increases were very extreme. If interest rates do increase we do not expect to see the same losses we saw on government and corporate bonds as we did in 2022. On aggregate, corporate bonds we would need to see a 2.50% rise in UK interest rates before the gains for the year are wiped out (all else being equal). That would mean interest rates in the UK sitting at 6.25%, and even then, the return for the year would be around zero. This is because in 2022, yields started at a much lower point and the coupon from bonds was much lower. The price-yield curve is convex and so at higher yield levels the change in price for further increases in yields is much lower. Now we are starting at a higher yield level and bonds are paying much higher coupons, which offsets some of the losses incurred when yields move higher.

All of this is to say that we don’t agree with lots of the commentary we see from investment managers that the equity/bond portfolio doesn’t work anymore, and that diversifiers and other complex strategies are needed. We do see inflation higher going forward but bonds are paying higher coupons and absolute levels are much higher. It is about diversification within an asset class, rather than just diversifying between different asset classes.

In Europe the ECB opted to increase interest rates by 0.25% to 2.25%, the first increase in nearly three years. The rationale was clear in that they see a broadening out of inflation from the energy supply crunch in the Middle East. Japan followed suit putting interest rates up by 0.25% to 1.00%. Although it won’t be a straight road back to lower energy prices, we are wondering whether they were too premature with their decision – growth is still weak in Europe. Defence company valuations pulled back in Europe as companies are hit two ways. The first is by disappointing revenues in Q1 2026, and the second is in governments’ lack of commitment to increasing defence spending. Investors had been optimistic about the sector but it is clear that too much future growth had been priced in.

–

Areas of focus

- Technology stocks’ prices remain elevated and highly volatile, driven by daily news flows, not fundamentals.

- Defence companies have pulled back as investors re-evaluate just how much growth there will be in earnings and how willing and able governments are to spend on defence.

- US treasury yields remain high as Warsh’s first Fed meeting pointed to the same if not higher rates later in the year. The US Dollar has strengthened this year, which will help unhedged sterling investors in US assets.

- UK Gilts dropped slightly on the departure of Starmer but remain elevated and we expect them to stay so.

- YTD gold has underperformed major global equity indices, indicating its momentum has slowed and the higher real yields will weigh on its attractiveness. Falling below $4,000 at one point, we reiterate our previous stance on the yellow metal.

- US high yield bond spreads are tighter than they were at they were at the start of the year and have outperformed investment grade debt, as a junk rally in assets continues and investors look for risk.

- Global emerging markets continue to push higher while Chinese equities remain in the red throughout the year.

–

Asset Class Returns

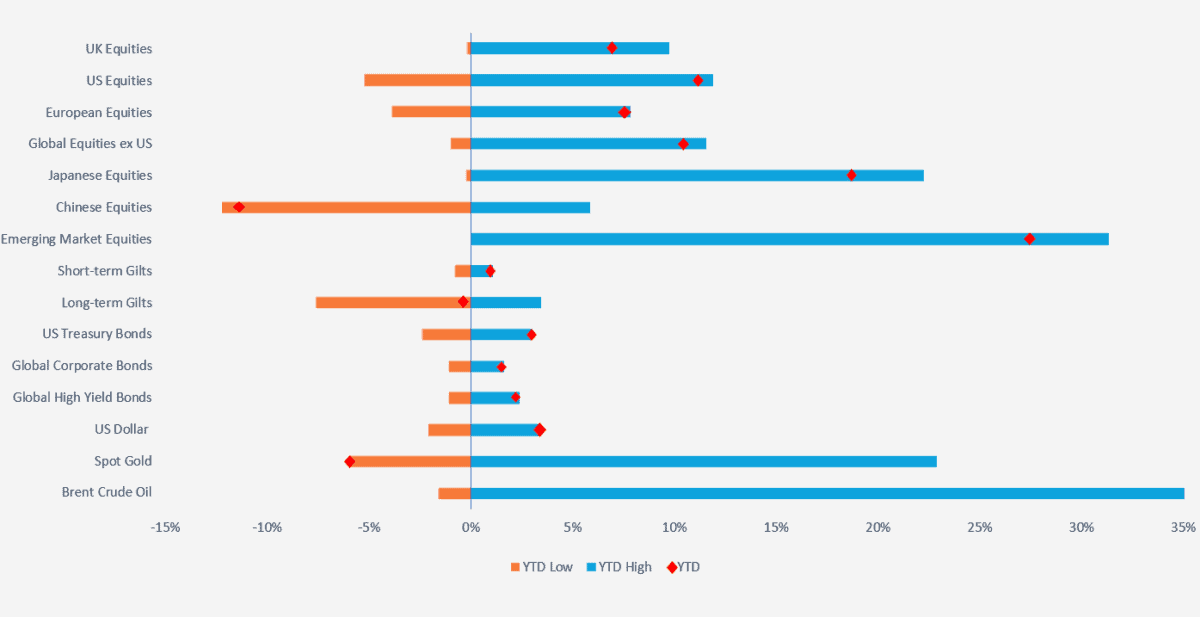

Selection of assets 2026 YTD returns and range of returns as at 25.06.2026 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 3000, STOXX Europe 600, MSCI World ex USA, MSCI Japan, MSCI China, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global Corporate Hedged GBP, ICE BOFA Global High Yield Hedged GBP, US Dollar Index, S&P GSCI Gold Spot & S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Returns based on daily data. Source – Watson French with data from FE Analytics and MarketWatch. Data correct as at 25.06.2026). The YTD point for Brent Crude Oil is not shown as its YTD return is 50.05% and including this would distort the chart too much.

–

US

Are private markets and big technology companies taking everyone for a ride? Last year we saw no indication that private companies such as SpaceX and Anthropic wanted to list publicly, and now we see them rushing for the door. Alphabet raised $85 billion in equity to fund its increasingly expensive AI buildout and South Korean memory maker SK Hynix is also looking to list on the NASDAQ using American Depositary receipts to raise $29 billion. Following SpaceX’s IPO, Anthropic and OpenAI are now rushing to go public.

So are these genuine capital raising events or are companies seeing something we don’t – are they looking to lock in gains and raise funds while markets are high and pass most of the risk onto the public?

It is interesting that Alphabet has started to issue equity given it has spent years buying back shares (a form of return for shareholders). With other big tech companies also looking to issue equity we will likely not see share buy backs for a long time and that part of the return for shareholders will disappear. This will put pressure on them to deliver exceptional earnings to keep the growth going. The $85 billion Alphabet has issued will be small relative to its market cap but it will dilute the earnings per share for existing investors and will put pressure on the share price – will this extra equity translate into increased growth and earnings? Unlikely, but at the moment it is seen by Alphabet and other big tech companies as necessary to keep up in the AI buildout. There was strong investor demand for Alphabet’s equity raise, causing the company to increase the amount it raised.

Meta also looks to be following suit with a potential equity issue as well and this could start a trend of more equity issues in the US. Again we reiterate that with huge IPOs coming to the market this year and more equity being pumped into the market by already huge tech companies, we don’t see how the market will absorb this.

But we are in a changing landscape. Data from Goldman Sachs shows that in the Russell 3000 US equity index, there has been a negative net supply of equities into the market since 2003 (share buybacks are greater than new equity issues). When you reduce the supply of something and demand picks up this results in a price increase. Combined with asset-light balance sheets, low interest rates and plenty of money in the market from quantitative easing, this powered growth stocks’ valuations higher over the decade.

Now the tides are a-changing. Big tech companies are looking to issue new equity, they are cutting back on share buybacks, interest rates are relatively higher, Kevin Warsh wants to shrink the Fed balance sheet (quantitative tightening, which involves selling bonds into the market and taking liquidity out) and we are seeing some big IPOs into the market along with corporate bond issuance. We see all of these as frictions on equity prices. Goldman Sachs forecast that for the first time since 2003, net equity supply will be neutral in 2026 and could likely increase.

The earth’s tectonic plates are constantly pushing, pulling and sliding past each other, and when enough pressure builds stored energy is released and an earthquake occurs. These changes in market activity are exactly this. What we are not saying is that this will happen tomorrow, next week or next month. But we are saying pressure is continuously building in the market and at some point we will see a correction, and so in the meantime we reiterate our points on diversification and knowing what you own. It’s not the growth that concerns us, but the pace of the growth.

AI is also enabling the formation of more companies in the US (history shows that if new technology makes something cheaper, the demand increases and so more jobs and companies are needed to fulfil that demand – this is Jevons’ paradox).

This is where unloved areas of the market may be attractive, such as dividend paying companies which can utilise AI. We expect returns to broaden out and are cautious as to whether passive index investing (especially with indices mandated to buy new equity issues) will perform as well as it has over the past decade. With three S&P 500 passive tracker funds now holding more than $2.6 trillion in value, it is less about fundamentals driving the market and more so the mechanical flows into the indices from regular investing.

As expected, SpaceX’s IPO went off with a pop, initially making Elon Musk the world’s first trillionaire and attracting strong inflows to push the stock’s price above $160. We expect this to prompt more IPOs but again caution against fatigue from investors. Starting with the biggest IPO puts pressure on smaller IPOs to perform. Later trading pushed the price of SpaceX down to $154, a fall of 16% in a single trading session. As an interesting point, Cerebras Systems, which launched its IPO earlier in the year, peaked at $311 and is now trading at $182, $3 below its IPO price.

But it’s not just equity that we need to be watching. We have a size and volume problem with bonds. The big tech companies have already issued billions of dollars’ worth of bonds and this will continue. In the dot com bubble technology bond issuance peaked at $85 billion in 2001, which was 14.5% of the total bond issuance that year. Forecasts point to AI related bond issuance reaching $400 billion at high estimates, representing 20% of total issuance. In 2015 the big tech companies represented just 1% of issuance.

When companies issue bonds someone has to buy them, and while there is a lot of demand for corporate bonds it still has to compete with other forms of borrowing and capital issuance. As the supply increases the only way to deal with this is for spreads to widen, i.e. investors will demand more yield (and pay lower prices). Spreads are still historically tight and so despite good coupon income on offer, the risks are asymmetrical on the upside (that is to say, further spread tightening looks very unlikely). Higher government bond issuance at the same time also puts further pressure on yields.

Spreads may widen but oversupply isn’t the main and most major risk. As competition becomes more intense in the AI space the risk of defaults is the main risk. Although it doesn’t look likely over the short term, longer term this could cause losses in the sector. We have to remember that when the winning AI companies become clear, bond investors do not capture the upside (as opposed to equity investors, who do) and so properly identifying the risks in software/technology bonds is crucial.

The US jobs report for May was released with 172,000 jobs added, far above the 80,000 jobs markets had forecast. The unemployment rate also held steady at 4.3%. The war in Iran looks to be on the road to ending and in theory this will and has pulled oil prices down. But a lot of infrastructure was damaged in the war and this will take years to rebuild, and so it is unlikely that oil prices will fall to the levels seen before the war started. I note that after writing this, the oil prices are actually below their pre-Iran war levels.

It is important to recognise this to be a short term price level, with prices likely rising in the next few months as short term supply (where there is a lot because of all the stranded oil tankers) moves through the system.

Most of last year and earlier in 2026 we talked about how job revisions were being revised downwards, but for the last two months jobs were revised collectively upwards by 93,000, with 350,000 jobs being created. At the same time CPI for May came in at 4.2%, up from 3.8% in the previous month and up from a low of 2.4% in February. Core inflation did however only move up from 2.8% to 2.9% as the inflation picture is being driven by energy costs.

Some strain is already coming through as Apple has said it will raise prices on its products to offset increasing memory and chip costs (prices rose by roughly 15% to 20%, which is high in percentage terms but for the US consumer a MacBook Air rose by $200, which is large in dollar terms because they were not cheap to begin with).

If inflation looks likely to pick up further, and with a still steady labour market there is no reason for the Federal Reserve to cut interest rates. But if prices come down the pressure on inflation may slacken. When interest rates are higher the discount rate on equities stays higher, and for more distant cashflows this results in a much lower net present value.

What the Fed does about this is a puzzle. If we start to see core inflation picking up the Fed will have to act. In his first meeting as Federal Reserve Chair, Kevin Warsh promised price stability as the Fed kept interest rates on hold. Nine of the 18 Fed officials estimated higher rates by the end of the year, compared with no officials forecasting this earlier in March. Warsh promised to slim down the Federal Reserve’s balance sheet which stands at around $6.7 trillion, which would put further pressure on treasury yields. With rates appearing to stay higher we will be interested to see if he follows through on this. He also wants to cut down on the Federal Reserve’s future guidance, which could act as a drag on bond yields as investors have less information on what the Fed may do in the future.

Despite the potential bumpiness we see in markets going forward, the data does point to the rise in US equities’ prices coming from earnings growth. For the first quarter of 2026 S&P 500 earnings growth was 18% (14% excluding mega cap tech companies). Future earnings growth has risen faster than the growth in share prices and this has lowered the forward P/E ratio from 22 to 21. But again we come back to the growth coming from AI spending, with data from Goldman Sachs pointing to half of future earnings growth in 2026 being driven by AI spending. We also reiterate our point in the introduction that without AI and energy, the S&P 500 would be in negative territory (highlighting the narrowness of the market and dominant sectors).

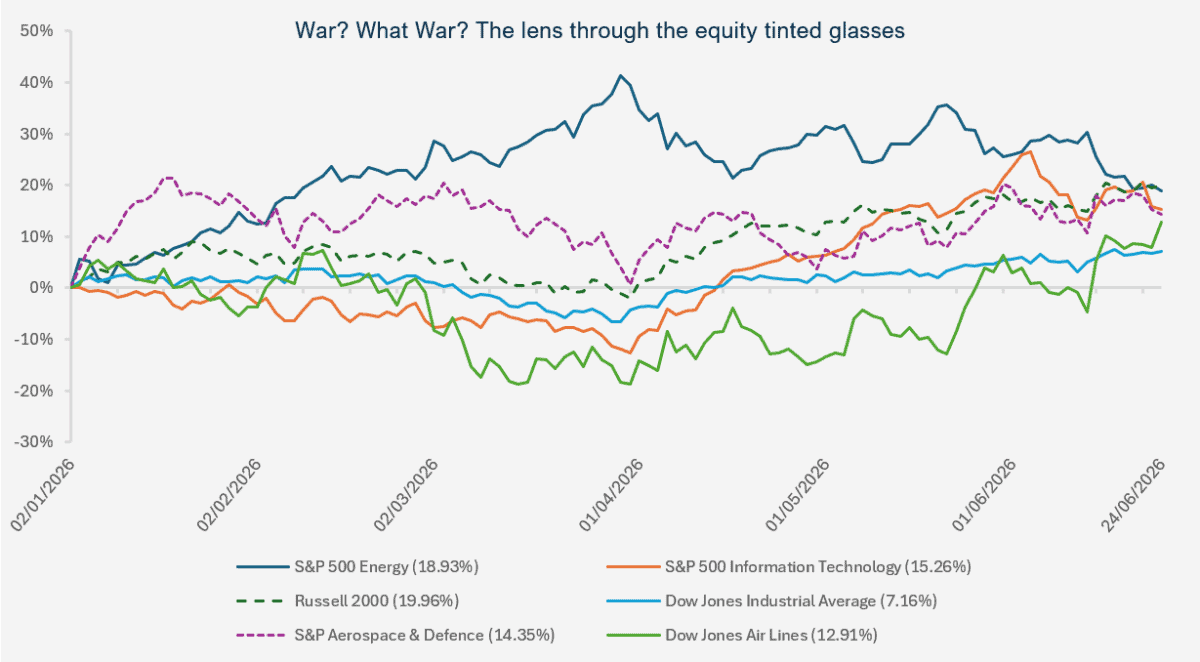

Chart showing the year to date performance of various US equity indices and sectors including the Russell 2000 (smaller companies index) & the Dow Jones Industrial Average index (price weighted index of the 30 of the most traded US stocks). (Source – Watson French with data from Investing.com. Data based on daily opening prices and in US Dollars. Data correct as at 25.06.2026. Data period runs from 02.01.2026 to 24.06.2026).

For our final note in this section, the FT reported on an innovative and strange financing mechanism for Anthropic, led by two private credit firms. It is difficult for investors to lend to private and unique companies because there is nothing for them to value the company to relatively. This makes it difficult to decide on what yield to lend to private companies at.

Anthropic wants to keep debt off its balance sheet to make it look attractive for public investors with its upcoming IPO and reports say that it refused to share information with credit investors (strange and again, some poor governance/transparency issues here). So rather than get companies to lend directly to Anthropic, the two private credit firms have set up a special purpose vehicle which raises cash from investors via debt offerings, and in turn buys AI chips which it leases to Anthropic. The debt is backed by the lease payments Anthropic makes and the value of the AI chips (which do depreciate over time and eventually become worthless, but no one can agree on how long this is). So a bit strange so far given the lack of transparency and the collateral being something that could be worthless sooner than the company says so.

But what we find very strange is that Broadcom, an entirely separate company involved in the AI buildout and a public company with an investment grade credit rating, has agreed to be a guarantor on the debt in case it cannot be paid by Anthropic… There is no intuitive reason why Broadcom would do this, but they state they want to help their customers realise their AI ambitions quickly. We can see the benefit for Anthropic as it lowers the yield on the debt significantly, but we think it again points to creative financial engineering and technology companies’ reliance on each other to keep the cogs turning. If one domino falls, we expect the whole pack to fall.

–

UK

Unsurprising? Surprising? Expected and unexpected? The media love their adjectives to sell news headlines for the UK economy. The UK economy contracted in April by 0.1% (whether expectedly or unexpectedly), driven by a slowdown in the important services sector. The three-month growth rate to April remained at 0.7% but the higher energy costs and uncertainty regarding the war in Iran and the direction of interest rates dragged on growth in April. A slowing of growth could put a halt on an interest rate rise, as if the direction of travel is downwards for growth, this should start to reflect in services inflation and thus wage inflation. The Bank of England Monetary Policy Committee has never been one for aligned thinking so anything could happen.

Following this CPI inflation for May held steady at 2.8%. Oil prices continued to put upwards pressure on inflation but with the war in Iran settling down and oil prices now falling below their pre-Iran war levels we could see a steadying in the inflation picture. Slow growth and steady inflation put the prospects of an interest rate rise much lower.

You could argue that interest rates were already at a restrictive level prior to the war in Iran and no further rate hikes are needed, and this is the risk Europe and Japan face with increasing rates as energy prices start to retreat following resolutions in the Middle East. Suddenly you could have central banks chasing short term data which doesn’t do much for their credibility.

But the question again is can we rely on the economic data we are getting and is it accurate, with another major error from the Office for National Statistics. This time they allocated interviewers to the wrong survey, failing to spot this for several weeks. Around 1,200 telephone interviews that were going to be used to inform the labour market report did not happen. The result of this will be a decline in the quality of the survey and less confidence in what is reported. It’s no wonder the economy is stagnant if we don’t even know who and how many people are working.

Last month we spoke about the UK Gilt yield curve and how long term rates could stay higher due to structural reasons. In some respects this will increase the attractiveness of longer term bonds because the upward sloping nature of the yield curve would make roll down attractive (holding onto a bond as its maturity decreases with the yield on the bond falling as it moves down the yield curve, increasing its price). But in the UK Gilt market this is far from a reliable strategy due to the higher volatility we continue to see and likely expect to see going forward. However, if we see short term rates higher because of shorter and medium term inflationary pressures this will flatten the yield curve and makes the short end look more attractive.

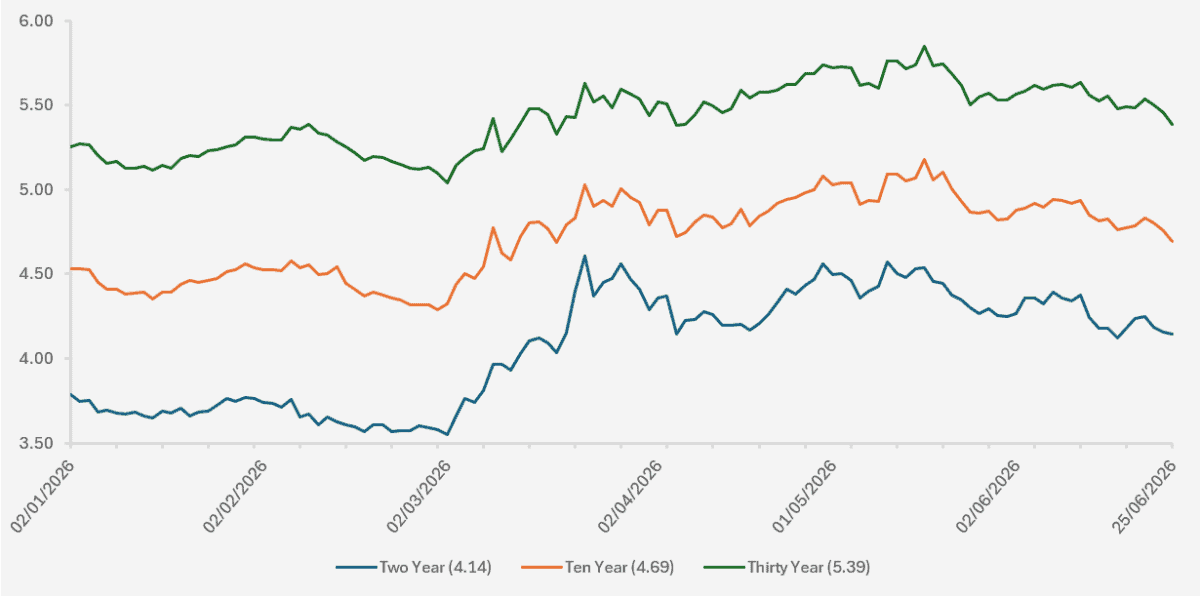

We can see in the chart and table below the change in UK Gilts with three different maturities. The two-year yield has increased by a greater magnitude than the ten and thirty year Gilts (yield curve steepening) because the two year yields are more sensitive to changes in interest rates and inflation. Shorter term bonds have less duration (sensitivity to changes in interest rates) so the losses have been lower than that of longer term bonds.

Chart showing the YTD yields of UK Gilts over different maturities. (Source – Watson French with data from Investing.com. Data is based on daily opening yields. Data correct as of 25.06.2026. Data period runs from 02.01.2026 – 25.06.2026. As the lines rise the yield on the bond rises and the bond prices fall).

Table showing the percentage increases in the above Gilt yields.

So if yields fall it would be intuitive to think that the longer term bonds would benefit more than the two year bonds. This isn’t necessarily the case and often the two-year can fall by a greater amount and still offer good value. The real question is where the yields will go from here with a new Labour leader upcoming.

The new Labour leader may fund expenditures from borrowing, which will increase supply and push yields up. Inflation may prove to be persistently higher than expected and keep yields higher. There are a lot of ifs and buts. What we do expect is for them to remain elevated and volatile. Long term bonds can be a proxy for future economic growth. With severe structural issues we think the bonds reflect political and fiscal risk premiums, not growth.

The UK, like Europe, is finding it difficult to fund its proposed defence spending. Rachel Reeves hoped to be able to fund £13.5 billion in extra spending by making cuts in operations elsewhere, rather than having to increase taxes or issue more debt. She did say increasing taxes is preferable to issuing more debt and this has helped to keep the bond market calmer. Higher taxes could equate to lower growth which would pull down inflation and rates in the future but it would not be a popular choice. This is all in doubt though, with Starmer’s resignation and a potential new Chancellor.

Defence companies have had a wobbly year. The main demand for their products comes from governments, and it is constantly in doubt whether they will follow through on their commitments to higher defence spending. We saw several high ranking officials in the UK government resign over delays and a lack of clarity over whether there will be higher defence and where it will come from. Defence companies have had such a stellar few years with triple digit gains. Without further clarity, and there already being a lot priced into their share prices, we could see share price growth stall. We are also seeing the rise of high-growth, technology-focused defence companies such as Anduril in the US which will provide competition for traditional and established defence companies. We see increased conflict as a longer term structural theme which in theory should mean higher defence company valuations. With these already reflecting the long term outlook we see higher commodity and energy prices as the main implication of this theme.

–

Japan

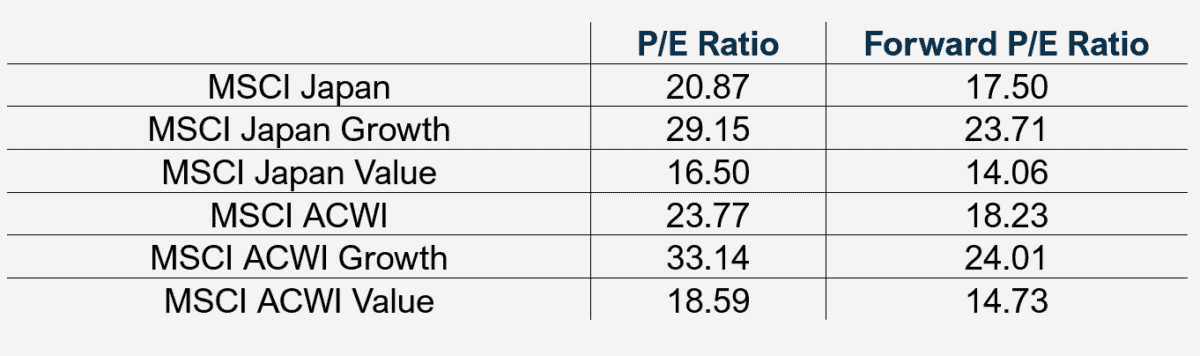

Japanese equities have continued to perform well this year, with the longer term outlook of structural reforms in the stock markets and better managed companies continuing to help push value companies higher. For the past six years growth has lagged value in Japan but this year we have seen growth companies excel as the buildout in AI benefits many companies. Some estimates show Japanese equities as highly valued and so there are risks in the asset class, but valuations are not yet as high as broad global indices. If earnings grow more than share prices we will see these valuations remain under control.

Table showing the trailing and forward price to earnings ratios of Japanese and global MSCI equity indices. Data from MSCI and correct as of May 2026.

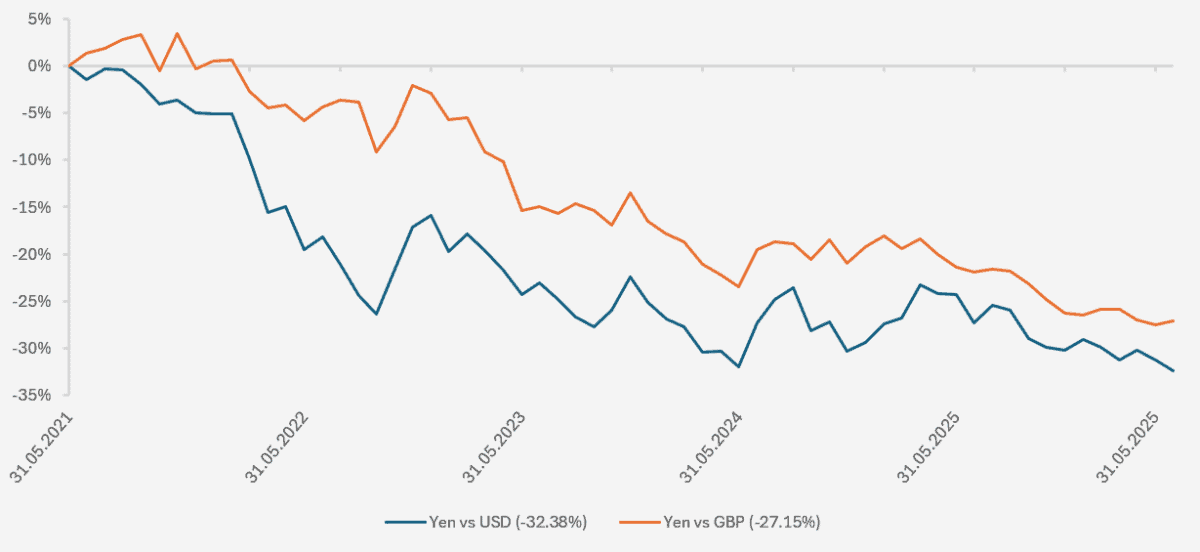

The Japanese Central Bank raised interest rates to 1.00% in order to make sure inflation doesn’t get out of hand. Like the US, higher interest rates will put pressure on Japanese equity valuations and earnings. CPI for May came in at 1.5%, which was an increase from the previous month’s rate of 1.4% but still in line with January’s figure of 1.5%. Like other Asian countries, Japan is an energy importer and the war in Iran will have had an effect on prices in the country. The Yen has also continued to weaken against the US Dollar which will make imports more expensive, but exports more competitive. Japanese bond yields continue to move upwards and remain at their highest levels since 2006.

Chart showing the five year cumulative change in the Yen vs the USD & the GBP. (Source – Watson French with data from FE Analytics. Data based on monthly change in exchange rate. Data correct as of 25.06.2026. Data period runs from 31.05.2021 to 25.06.2026. When the line declines this indicates a weakening of the Yen versus the other currency).

The weakening of the Yen has long been a problem for Japan and has been a source of frustration for Trump and US Treasury Secretary Scott Bessent as this makes exports to Japan more expensive. Currencies are often driven by interest rate differentials, this is why currency futures and forwards are priced based on interest rate differentials not by speculation – see the GBP versus the Yen. The UK has been plagued with political instability and sluggish economic growth and yet over the past five years the Pound has strengthened against the Yen. Why – because UK interest rates have been more attractive owing to higher inflation. The Japanese Central Bank aims to combat this by buying bonds in the market and using yield curve control. A weak Yen is important for Japan because it adds to import costs which have a big effect on the consumer and economic growth. It does make exports more attractive though.

This matters for equities because part of an overseas equity return comes from currency movements. If the Pound strengthens against the Yen this reduces any gain on the underlying equity (Japanese equities are purchased in Yen. If the Yen weakens, one Yen buys less Pounds when we want to realise our gains in Pounds). In our portfolios we choose not to hedge currency risk for equities because we see it as part of the higher risk asset class. Many companies also engage in currency hedging within their operations and so it can result in double hedging. And finally, hedging is not free or straightforward. But the main point is that we are not forecasters, and no one knows with any accuracy what interest rates are going to do. For example, between January 2015 and August 2018 the Yen strengthened against the pound by 44.31%.

Where we do see some potential major risk is the rising of Japanese government bond yields and the reallocation of domestic Japanese investors’ capital away from the US and back into Japan.

We think the combination of growth companies and value companies which have a real tailwind behind them make Japanese equities varied with lots of opportunities.

As a recap for the value theme and the structural reforms, for years Japanese companies hoarded cash on their balance sheets and didn’t pay attractive dividends or buy back shares. They also tended to be very large conglomerates which have a wide range of businesses which had little if any link to one another. Because of this many parts of their businesses had a low return on equity and this dragged down profits and the share prices of the companies. The Tokyo Stock Exchange started a long process of reform which aimed to improve corporate governance to enhance shareholder value and improve their cost of capital and capital efficiency. The result has been a steady improvement in dividend payouts, share buy backs and the selling of periphery and unnecessary parts of their businesses. Return on equity and share prices have improved but there is still much more room for improvement.

–

Robert Dougherty, Investment Director

July 2026

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested. Data is correct at time of writing and cannot be guaranteed.