1st September 2025

Markets have held their nerve and shrugged this news off – a common theme this year. Either markets have already priced in the risk to the Federal Reserve’s independence or they care as control will shift next May when Federal Reserve Chair Jermone Powell’s term ends.

We saw a wobble in big tech companies with improvements in AI models hitting a wall. Open AI’s latest model release was far below expectations and Meta also delayed the roll out of its newest model as the improvements relative to the last iteration were not significant. Nvidia managed to grow its revenues by high double digits but the growth was the slowest it had been for a few years and did not meet investors’ high expectations. With stretched valuations these companies need to deliver high returns on their investments.

Jerome Powell delivered his annual speech at the Jackson Hole Symposium, and following this markets moved up as the probability of a rate hike increased. We will go into more detail on this and the state of the US labour market later on in this article.

Increased tensions arose between Europe and the US on tariffs, with automobile producers still facing a higher tariff unless Europe lowers some of its trade barriers, including its digital services tax on big tech. Despite ‘deals’ being made we are still not seeing the end of the tariff story.

Private equity is the big asset class of the year. With private equity looking to be more accessible to the average investor, many think this may not be such a good idea. Private equity has seen huge growth in its assets under management and it is becoming more interlinked with public markets. There is a lot to go into on private equity and so we discuss this in a separate article later in the month.

The Bank of England delivered a quarter point interest rate cut, but this rattled markets as the Monetary Policy Committee had to vote twice to break a stalemate, indicating to markets that further rate cuts may take time.

Gilt yields pushed up on this news. Inflation also picked up again in July and markets continue to expect tax increases in the next Autumn budget. The economic outlook for the UK remains downbeat, but this highlights an important distinction between the UK economy and UK stock market. The UK small, mid and large cap indexes continue to remain in positive territory for the year and there are returns to be made in UK equities, even if the economy is going down the pan.

A trade deal between the US and China remains distant, with a further delay on tariffs while the two countries negotiate. The Chinese property market has been in a huge slump for a long time now. Recent stimulus measures in Shanghai and Beijing look to help this by encouraging a pickup in demand. We remain cautious and note that many times over the last two years, investors believed “now is the time” for a pickup in Chinese markets, only to be disappointed.

For the first part of the year the broad Japanese equity indices were negative, but since the US trade agreements the indices continue to remain in positive territory. We reiterate the longer term potential from the region amid increasing pressure from the Tokyo Stock Exchange for businesses to improve their price to book valuations and return on equity ratio. The Yen also strengthened against the pound, giving hedged investors a higher return.

–

Areas of Focus

- Corporate bond spreads remain tight. The liquidity on older vintages is restricted while not commanding a suitable premium.

- With yield curves steepening, longer dated bonds offer better yields but carry much more interest rate risk.

- Banking stocks continue to benefit from higher interest rates and defence companies from the narrative around increasing government defence spending as a percentage of GDP.

- Global investors continue to question their high allocations to the US but it remains the deepest and most liquid capital market with the best exposure to big technology companies.

- Emerging market bonds offer opportunities for returns and a negative correlation with the US Dollar.

- Japanese companies continue to look attractively priced and still have a large tailwind of corporate reform behind them.

–

Asset Class Returns

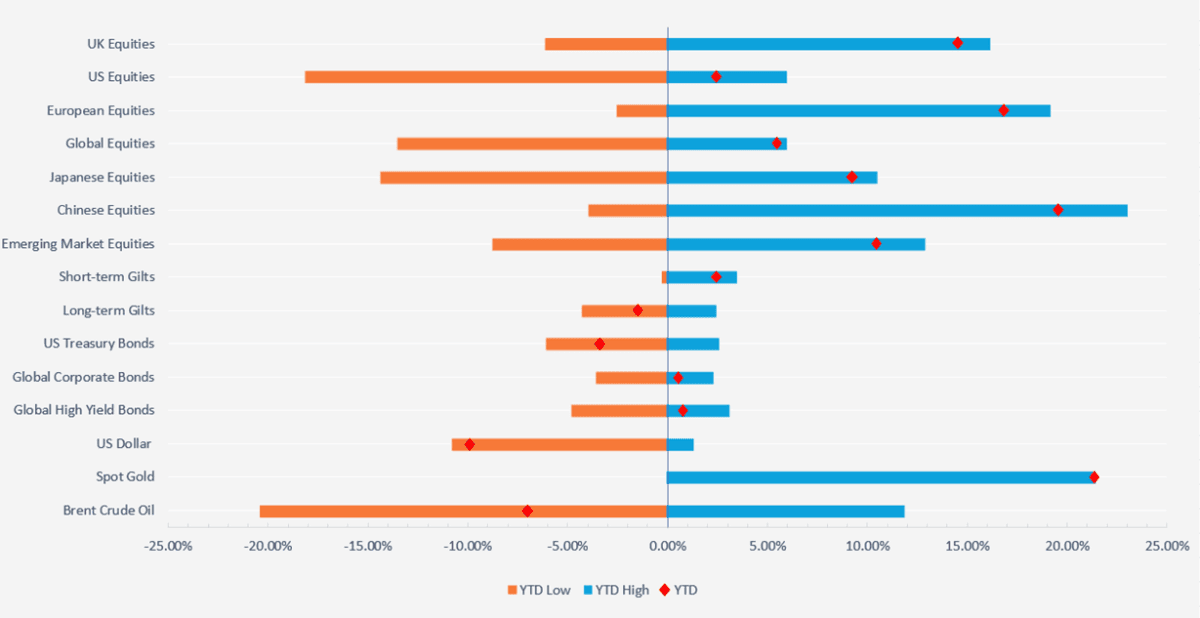

Selection of assets 2025 YTD returns and range of returns as at 01/09/2025 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI China, MSCI Japan, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global High Yield, ICE BOFA Global Corporate, US Dollar Index, S&P GSCI Gold Spot, S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Source – Watson French with data from FE Analytics and MarketWatch

–

UK

We will be economic data-heavy for the first part of this section but I promise I will bring it around! The Bank of England cut interest rates by a quarter point at the start of August, bringing the base rate to 4.00% from its 2024 high of 5.25%. Voting on the decision was very close with the Monetary Policy Committee having to go to a second round of voting as a consensus couldn’t be met initially.

The second round of voting showed four members opting to hold rates steady while five members voted for a quarter point cut. During the first round one member of the committee opted for a larger half point interest rate cut, then during the second round they reduced their preference for a quarter point cut, breaking the stalemate.

While the Federal Reserve had two dissenters on their voting committee, the Bank of England has a much more split voter base. The committee has now gone 30 meetings without being able to make a unanimous decision.

The situation in the US is uncertain and inflation is above target, which could potentially pick up in the future (similar to the UK, but inflation in the UK is above target by a greater extent). However, in the US economic growth is stronger than in the UK.

This again highlights the big problem facing the UK – sluggish growth and above-target inflation. Inflation picked up in July with CPI recorded at 3.8% (up from 3.6% in June) and CPIH at 4.2% (up from 4.1% in June). Core rates, excluding volatile items like food and energy, were 4.2% for CPIH (down from 4.3% in June) 3.8% for CPI (up from 3.7% in June).

Services inflation (which is important for the UK, being a services based economy) remained constant at 5.2% in the CPIH data but increased from 4.7% to 5.0% in the CPI data.

Of particular note and the biggest contributors to the inflation data were food and beverages and transport costs. CPI in the US is at 2.7% and in the Eurozone it is at 2.0% (0.9% in France and 1.8% in Germany), so relative to its peers the UK is a fair margin above target.

Average wage growth (excluding bonuses) for the three months from April to June was 4.6%, down from 5% in the previous three months but still elevated and positive in real terms. The link between the increase in food inflation and strong wage growth suggests that supermarkets and food producers are passing their cost increases onto consumers (particularly National Insurance and minimum wage increases).

Consumers have already faced significant price increases over the past two years and further increases will certainly face strong resistance.

GDP growth slowed from 0.7% in Q1 2025 to 0.3% in Q2 2025. More pressure on consumers spending on essential goods will likely pull this down further.

The Bank of England Governor Andrew Bailey said rates were on a downward path but ‘future cuts would need to be made gradually and carefully’. Derivative markets are pricing in just one interest rate cut for the next 12 months.

The risk of stagflation is picking up with weak growth and strong/sticky inflation. Any tax increases in the Autumn budget would likely weigh further on growth and if there is no offsetting fall in inflation this would put the Bank of England in a difficult position.

As promised I will explain what this means for markets. For the UK equity market it doesn’t mean much, certainly for the large cap stocks (FTSE 100 constituents). Firstly the overseas sales ratio of the FTSE 100 is over 80%, and for the FTSE 250 its around 55%, so the majority of these companies’ earnings come from outside the UK. A lack of consumer demand and struggling economy will therefore not affect the FTSE 100 earnings greatly.

The FTSE 250 will be impacted to a greater extent as it relies more on domestic consumers, but it still benefits from overseas strength as just over 50% of revenue comes from abroad. The FTSE 100 will be more influenced (in terms of revenue) by overseas economic strength or weakness.

Furthermore for the FSTE 100, if we look at the sector and sub-sector breakdowns of the index, over 14% of the stocks in the index are banks.

If interest rates remain higher the net profit they make on interest (what they charge on loans versus what they pay on deposits) will remain high, although at risk from tax increases at the next Autumn Budget (which have been rumoured).

While borrowers struggle under higher mortgage and borrowing rates, banks tend to do well all else being equal. The index is also dominated by energy companies and healthcare companies, both of which tend to be overseas/global in nature and not domestically driven.

It is not so clear cut for the FTSE 250 as it is mainly made up of financial companies (not the same as banks), and lots of these are investment trusts. Around 45% of the index is accounted for by financials and of this 28% are investment trusts. In the index, 87 of the 250 companies are investment trusts with just three being banks.

This sector likely skews the index overseas revenue ratio – after all an investment trust investing in Asia isn’t the same as a company generating actual sales from that region. One of our key themes this year is knowing what you own, and with the FTSE 250 being dominated by investment trusts this is particularly difficult.

The next biggest sector is industrials at 15% and then consumer discretionary at 13%. Consumer discretionary is more domestic in nature and more reliant on how confident consumers are feeling and how much they are spending and not saving.

The smaller UK indices are much more domestically focused and influenced by interest rates as they tend to borrow more and also borrow at higher rates, as their credit ratings and financial strength are lower.

This both reduces net profits and also slows investment, as they either cannot borrow or do not want to borrow at higher rates. This can push them into issuing more equity which, while it can provide financing, does dilute existing shareholders’ earnings.

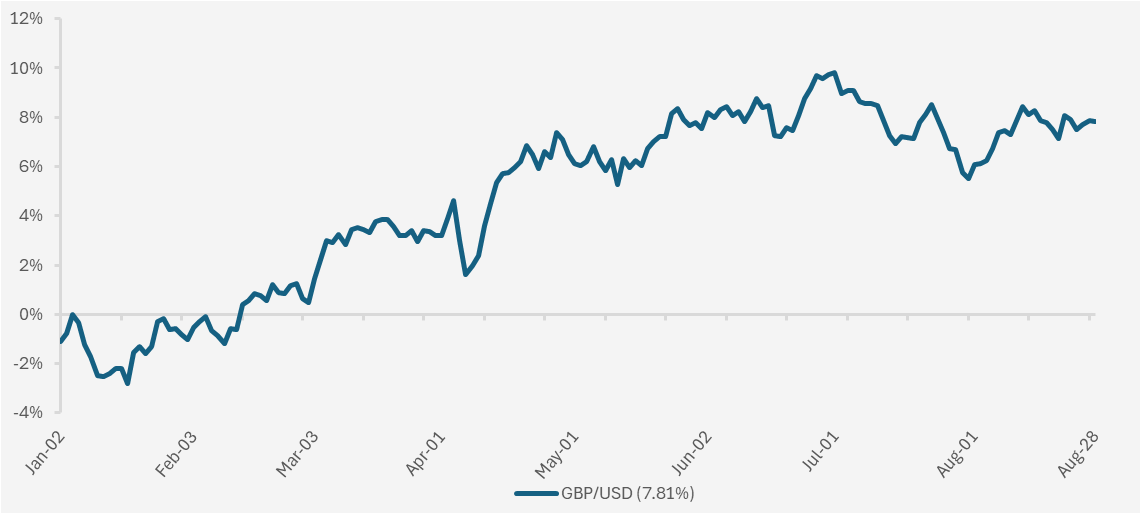

However, a major point to note on higher interest rates and perhaps the most important for the non-domestic companies is the strength of the pound. With higher interest rates relative to other countries, the pound strengthens.

This year the pound has gained just under 8% on the US dollar, which may not seem like a huge value but in currency markets this is significant. A stronger pound means that when companies convert their earnings from a foreign currency back into pounds it is more expensive for them and lowers their profits.

YTD performance of GBP versus the USD (Trends upwards show a strengthening of the GBP and greater demand and downwards show a weakening of the GBP and lower demand. Source – Watson French with data from Investing.com. Data based on daily exchange rate. Data correct as at 28.08.2025)

A stronger pound does however mean that imports are cheaper. The UK imports a lot of goods so this could help to lower inflation somewhat, although tariffs from the US may indirectly offset this.

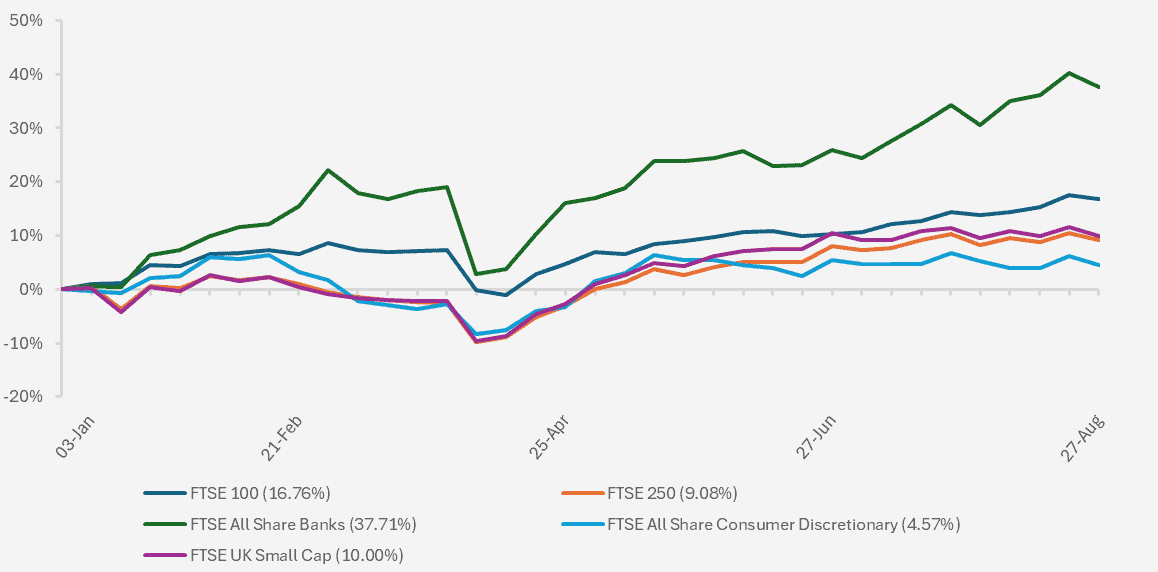

As we can see in the chart below, the UK equity markets have mostly stayed in positive territory for the year despite the risk of stagflation in the economy. The FTSE All Share Banks sector has continued to push higher and is still one of the best performers in the index.

Consumer discretionary stocks have continued to be weighed down as they are more domestically focused.

We also see the FTSE 100 index outperforming its mid and small cap peers for the reasons described above. Although the pound has strengthened against the dollar, the higher weighting towards non-domestic companies and the strong dividend yield has helped the index continue its momentum.

Lots of this momentum behind the UK market could be seen as shorter term tailwinds. One area the UK market will benefit from (and indeed, already has) is the increase in defence spending by major economies. This is expected to be a longer term theme.

The FTSE All Share Aerospace & Defence sector has returned over 68% YTD. Whether this will continue and how much has been priced in is a major question, although we think much of the future earnings are now reflected in share prices.

One area in which the UK will likely lag in terms of longer-term tailwinds is technology. Just 5% of the FTSE 250 consists of technology companies, and just under 1% of the FTSE 100.

YTD performance of UK stock market indices & sub sectors (Source – Watson French Ltd with data from FE Analytics. Data based on weekly returns. Data correct as at 27.08.2025).

The final and most important impact of the UK economic situation on markets is on the gilt market. Higher interest rates, or rather expectations for higher interest rates, keep gilt yields (the government’s cost of borrowing) higher. Higher gilts yields affect mortgage borrowing costs, corporate borrowing costs, equity markets and company investment plans/returns. It is fair to say that gilt yields are a pretty big deal then.

An important distinction to make is what the Bank of England (and all Central Banks) controls and what they don’t. Central Banks can influence the short end of the yield curve through their setting of interest rates, but the market dictates what happens to the longer end of the curve based on their expectation of economic growth, inflation rates and other things such as fiscal concerns.

Not all of the gilt yield curve (the curve showing the yield for different maturities of gilts) is equal in respect to higher interest rates and other fiscal concerns.

So far this year we have seen the yield on the 2 year Gilt fall by over 9% (from 4.37% to 3.97%) while the yield on the ten year gilt has increased by 3.74% (4.57% to 4.74%) and the thirty year gilt yield has increased by 9.15% (5.13% to 5.60%).

The two year gilt yield has fallen on the expectation that the Bank of England will continue to cut interest rates and thus bring short term borrowing down. The ten and particularly the thirty year yields have moved in the opposite direction and thus we have seen a yield curve steepening. A steepening yield curve usually indicates investors are expecting economic growth and inflation to be higher in the future.

When we subtract the yield of a conventional gilt from the yield on an index-linked gilt (one whose returns are linked to inflation) of the same maturity we can see what the market’s future expectations for inflation are. For both the ten and thirty years this comes in at around 3%, above the 2% inflation target.

We think however, that there is more at play here than pure inflation expectations. Economic growth has been weak in the UK for a while and the current inflation is likely structurally embedded, not a result of growth. The main reason for this steepening is fiscal rather than monetary.

Many global economies have high debt loads relative to their GDP levels. Some of this is still collateral from the 2008 GFC, but more recently from the emergency stimulus needed when the Covid pandemic hit. High borrowing is acceptable when interest rates are low but with the Bank of England base rate at 4.00% and yields much higher relative to the past ten years, interest on this borrowing becomes a massive burden.

The latest data from the Office for Budget Responsibility for 2023/2024 puts interest on government debt at around £106 billion or 3.9% of GDP. Note that as this includes gilts held by the Bank of England some of this doesn’t leave the public sector. In 2019/2020 this figure was £38.9 billion or 1.7% of GDP.

What this means is more government tax receipts are spent on paying this interest and thus less can be spent on investment and public spending. To keep spending the same borrowing therefore needs to increase – a vicious cycle because this borrowing itself attracts high levels of interest.

Chancellor Rachel Reeves’ current fiscal rules state that the government cannot borrow to fund day to day spending and debt must fall as a share of GDP by 2029/30. She had pledged to stick to these rules and bond markets like this. That’s why when Keir Starmer did not initially publicly back Reeves, bond markets got rattled and yields moved higher. Bond markets like and need fiscal responsibility. The risk here was that a new chancellor would come in who would not stick to the fiscal rules, pushing debt up with no plan to bring debt as a share of GDP down. Government bonds may be seen as risk free, but that doesn’t mean markets are chumps who will continually lend to a borrower who is irresponsible.

As a quick side note, corporate bond spreads – the interest rate companies pay to borrow relative to governments – are narrow in the UK and globally, and we think this could persist because investors see companies as more responsible. Combine this with strong balance sheets (for investment grade quality issuers) and we could see spreads staying tight. Some companies in Spain for example actually have lower borrowing costs than the government.

If bad policy decisions are made bond markets correct them. We saw this with Liz Truss and more recently Donald Trump, and will certainly see this again if the Labour government steers off its fiscal sustainability course. This is the biggest risk and we will see a sharp rise in yields if so.

What is the solution then? With growth and productivity low, inflation above target, spending cuts looking unlikely and borrowing restricted… the hard and unpopular choice – tax rises. The probability of this happening at the Autumn Budget looks more and more likely and all eyes will be on Reeves to see what she does. Tax rises will hurt growth in some way but it will potentially bring inflation down and more importantly it will provide much needed non-borrowing sources of income for the government. So does this matter for gilt markets? Absolutely. Fiscal irresponsibility will certainly push yields up higher and this needs to be avoided.

Another key point that is not being talked about much is the Bank of England’s quantitative tightening program. This involves the BoE selling or letting their gilt holdings mature, effectively reducing demand and taking money out of the economy. We all know what happens with falling demand when supply is higher. Yields push higher. The consensus is that they need to pause this program to help yields stabilise. Presently around £100 billion of bonds are leaving the Bank of England’s balance sheet over the course of the year.

The real elephant in the room is that structural changes are needed in the UK to sort this out for the longer term. Productivity needs to increase, both by technology changes and labour force rule changes. Increased investment is needed in the UK in new and profitable industries (semiconductors, AI datacentres, clean energy, robotics, digital finance, digital currencies).

I could talk about this all day, but back to bonds. Following the Bank of England’s Monetary policy decision we saw the yield on the two year gilt rise by 2.2% and the yield on the ten and thirty year increase by 4.15% and 4.63% as further uncertainty over the pace of interest rate cuts was introduced. 4.63% may not seem like a big increase, but imagine paying an extra 0.25% of interest a year for thirty years, that’s 7.77% in total (especially impactful when UK government debt is at nearly £2.7 trillion).

Changes in US policy and Treasury yields also have an effect on gilt yields as well which doesn’t help.

We expect long term yields to trend higher over time for a few reasons (i.e. the term premium continues to increase). Firstly, we do not expect inflation to settle at 2% sustainably over the long term due to technological and geopolitical changes. Second, we expect government borrowing to remain higher over the short to medium term to fund shortfalls in income. We also expect investors preferences to naturally drift towards lower maturities or alternative assets – think increased investment in long duration assets such as private equity, and the shrinking proportion of Defined Benefit (final salary) pension schemes.

We are watching out for changes in US yields and US economic data relating to interest rates and also any changes in tone from both Keir Starmer and Rachel Reeves over fiscal constraints. Longer dated debt is more sensitive to changes in expectations and so we continue to prefer shorter dated debt.

–

US Equity

Keep your head down if you are working in the American public sector (or private for that matter); if President Trump doesn’t like what you are saying you may just be ousted in the media and demanded to leave.

Recently Trump fired the head of the Bureau of Labour Statistics over what he claimed were politicised jobs figures which were designed to hurt him personally. Not only that but he has called on Intel’s CEO to resign, Goldman Sachs’ top US economist to be fired and now a Federal Reserve Governor.

It is widely acknowledged that like the UK, the Bureau of Labour Statistics has problems with its survey response rates, but the real solution is to invest in technology to improve efficiency, not reduce the department’s budget. One reason that response rates are falling is that immigrants are worried their data will be passed on to other government departments and they will face deportation, so they are not responding.

We also continue to see the US government getting involved in market affairs. The US recently took a 10% stake in struggling chip manufacturer and designer Intel, with an option to take a further stake should they sell off their manufacturing business. For the ordinary shareholder this has diluted their earnings and may deter other investors and customers from doing business with Intel.

Trump has also floated the idea of turning grants and loans given to semiconductor companies under the 2022 CHIPS Act into equity stakes. Again, this may well deter companies from going to the government for help and in the long run may damage investment and growth.

Nvidia and AMD are having to pay the US government 15% of any revenue they generate from sales of certain chips to China. A recent deal by Nippon Steel to buy US Steel gave the government a golden share, giving the US government a vote on major decisions.

As we mentioned previously, if some of this sounds familiar it’s because it is, and is more likened to what we would expect in China.

I should mention that the revenue AMD and Nvidia are paying to the US government is a form of export tax/penalty which is not allowed under US legislation. It brings into question whether the US will start using this tool more widely to generate revenues and whether it will be allowed by the courts.

CPI data for July held steady at 2.7%, unchanged from June and helping to keep US stock markets at record levels. Core inflation (stripping out energy and food prices) did tick up, rising 3.1%, 0.1% above estimates. The goods that did see prices rise include things like furniture, much of which is imported (the US is the world’s leading importer of furniture, with China being the world’s largest exporter).

This could be a possible start to tariffs filtering through into prices, but we still see it as too early to tell. One side of the argument believes tariffs will not have anything more than a one-time effect on prices and will now push harder for an interest rate cut, while the other side of the argument still thinks prices have not had time to adjust.

US labour market data remains in tension. Unemployment has remained low while the demand for workers has slowed, as shown by slowing payroll jobs growth. This is because the supply of labour has slowed dramatically – with net immigration near zero, much of the labour supply the US needs has dropped.

This has short and long term implications. In the short term a lower labour supply will stop the unemployment rate from pushing much higher. The unemployment rate edged up slightly in July but remains historically low at 4.2%.

Over the long term a smaller supply of labour hinders economic growth as it relies on labour and productivity. This is where AI can step in and help to push up the productivity level, keeping growth ticking along with a smaller labour force.

In the long run this could also mean lower wage growth and lower inflation, translating into lower interest rates. As mentioned, the stall in AI growth has started to turn investors’ heads and with a recent report from MIT showing 95% of AI pilot programs delivering no measurable return, meaningful AI productivity could be some way off.

Certain industries will feel the crunch of labour supply more abruptly. Construction, hospitality and agriculture have a greater reliance on immigration to fill job gaps. With lower supply this will mean lower output, lower growth and higher wage costs.

With labour data in tension, a sharp rise in layoffs will quickly push up the unemployment rate. Powell commented that ‘with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance’. Markets interpreted this as an interest rate cut at the Federal Reserve’s next meeting in September, but we are still cautious given a constantly shifting dynamic.

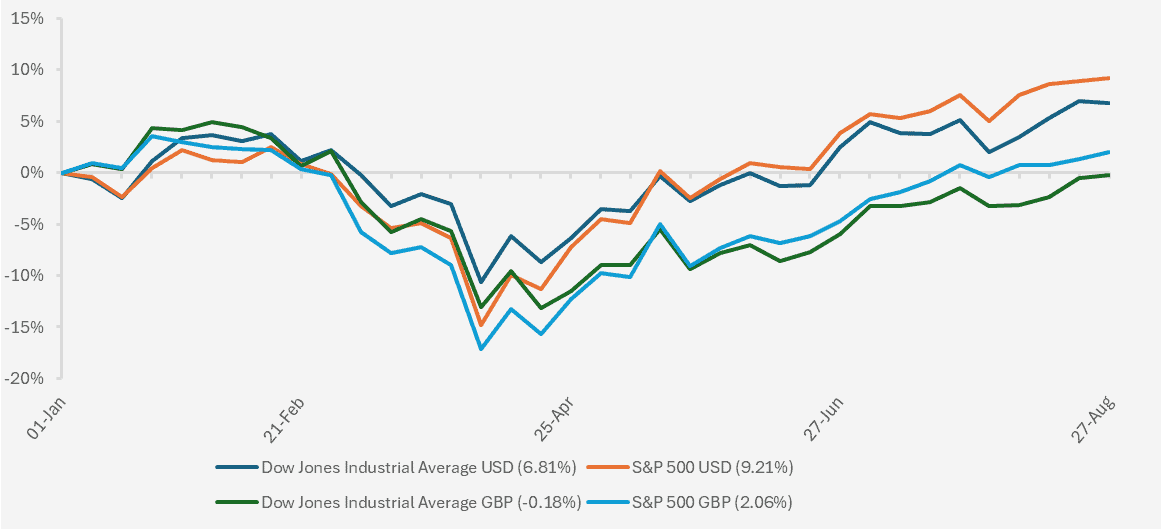

Further points to note from Jermone Powell’s speech include no change to the Fed’s 2% inflation target and a shift away from allowing inflation to overshoot this target, following a period of below-target inflation. From the weekly low point for the S&P 500 in April, in US Dollar terms the index is up 24% and 19% in Sterling. The strength of the Pound versus the Dollar means that although the US indices (minus the Dow Jones) have returned to positive territory, the currency has detracted from returns this year.

Prior to this year the strength of the US Dollar had given sterling investors a boost to their returns on unhedged holdings. Investors are now reconsidering whether to hold US assets unhedged or not. While hedging may seem like the right choice, there is a cost to hedging and over the medium term currency movements are prone to mean reversion, reducing the benefit of hedging. With US interest rates forecast to fall at a greater pace than UK rates, and investors feeling more uncertainty surrounding the role of the Dollar, we will likely see a further strengthening of the pound in the short term.

Chart showing YTD performance of US equity market indices (Source – Watson French with data from FE Analytics. Orange and dark blue lines shows US indices in US Dollar terms and green and light blue lines show the same indices in pounds sterling. Returns based on weekly data. Data correct as at 27.08.2025).

–

China

Both China and the US are looking to protect domestic interests and security by reshoring important industries and natural resource capabilities. On that front China is continuing to make big strides.

In terms of energy, China is making significant moves to protect itself from outside influence, looking to source all energy needs domestically. Presently 25% of the energy China uses is imported. Recent news on the massive infrastructure project on the Tibetan plateau is another step to change this. The hydropower dam is estimated to be able to power 120 million homes and will cost $167 billion.

China is also approving the merger of two shipbuilding companies, which will create the world’s biggest company in the industry with a market cap of $16 billion.

The US is attempting to make ship building a priority but has a long way to go compared with China. Data shows that the two Chinese companies accounted for 17% of the shipbuilding market last year, including building 55% of global tonnage, while the US built just 0.05%.

The US gave Nvidia the go ahead to sell less advanced chips to China (while taking 15% of revenue) but China has told its domestic companies not to buy the chips, instead preferring for companies to use their domestic alternative to Nvidia, Huawei.

Huawei chips are less efficient but the more profits they make the more they can invest to compete with Nvidia. China also believes that Nvidia chips will have a back door that will allow the US to spy on China.

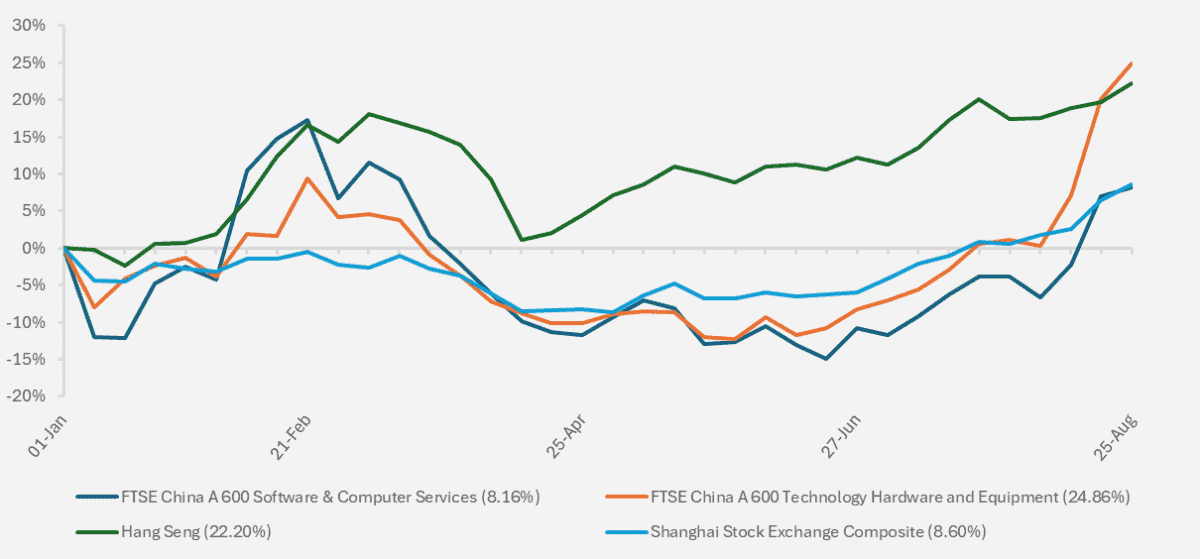

In a big boost for the sector (see chart below on recent performance), Chinese chip manufacturers are aiming to triple manufacturing output in 2026. This will allow them to produce chips at a greater pace and gain global market share.

Chinese technology companies had a strong start to the year along with the Hang Seng index. The Hang Seng index has outperformed the mainland Chinese indices because the Hang Seng index is much more technology heavy.

Despite a dip in the Hang Seng in April, the index has continued its move upwards, driven by a strong Initial Public Offering (IPO) market in Hong Kong and investors’ preference for technology companies. Chinese technology companies are seen as a diversifier away from the exclusively US big tech companies.

The Shanghai exchange is influenced by activities on the mainland and is not as technology heavy. The back and forth on tariffs has kept the index subdued relative to the Hang Seng index. Overcapacity in most sectors and a deflationary environment is keeping markets subdued as well.

YTD Performance of Chinese & Hong Kong stock market indices and sub sectors (Source – Watson French with data from FE Analytics. Returns denominated in Pound Sterling. Weekly returns used. Data correct as at 25.08.2025).

In other news the failing property company Evergrande has been delisted from the Hong Kong stock exchange.

The property sector slump in China started back in 2021 when the company was unable to meet the payments on its huge debt holdings, sending the property sector into a downward spiral. Government policies have looked to help revive the property market but have so far fallen short.

US tariffs on India have renewed a relationship between China and India with air travel between the two countries open again. China is looking to boost relations at a time when the US is penalising its allies.

China faces a continuing battle with deflation due to involution, which is excessive price competition stemming from overcapacity (caused by government support for most companies).

The government increased manufacturing and infrastructure investment and support in an attempt to keep GDP growth high, as the struggling property sector is no longer the driver it once was.

The government has introduced anti-involution measures to try and counter this, but to get out of the deflationary slump demand will need to increase as well as excess capacity being reduced. If companies exit a sector, the remaining competitors will jump on that share of the market and overcapacity will remain, not disappear.

Things to watch out for on the mainland are how the tariff situation with the US evolves, what advancements Chinese technology companies can make on AI and what other intervention or stimulus the government will propose in markets and the economy.

–

Robert Dougherty, Investment Specialist

September 2025

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested. Data is correct at time of writing and cannot be guaranteed.