1st February 2026

In times of change it becomes crucial to evaluate whether short-term events will have longer term implications. We have to ask the question, how will these events affect the actual fundamentals? When we say fundamentals we are looking at economic growth, inflation, employment and company earnings to name a few. For example, as we talk about later on, the US getting involved in Venezuela – will this affect fundamentals? Likely not and if so, probably only at the margins.

We see the main driving forces for this year will be much of the same as for last year. Namely geopolitical risk, inflation and the labour market and bond yields. With economic growth still reasonable, although not likely to be above trend (in the US this means around 2.7% real GDP growth), and company earnings and balance sheets still looking strong, we see no obvious catalyst for negative investment returns. Leverage is high in markets and many trades, such as gold, are extremely crowded. This combination could mean even smaller news will result in steeper market selloffs.

Equity market levels are high relative to history, however. Data from Apollo shows that based on the S&P 500’s forward P/E ratio compared to the subsequent ten-year annualised returns for that given ratio, based on the present forward P/E ratio we would expect a small negative annualised return over the next ten years.

The Cape Shiller Cyclically Adjusted P/E ratio (P/E ratio smoothed over ten years and adjusted for inflation, minus the ten year government bond yield) is also at historically extreme levels, indicating smaller future returns from US equities.

These measures are interesting, but they tell us nothing about the next year – only the predicted annualised rate for the next ten years. The relationship between the forward P/E ratio and the one-year return breaks down and gives us no guide. Ten year returns may look unattractive, but it doesn’t mean we won’t get positive returns this year.

With markets high and no obvious reasons for markets to drop, what happens to stock prices? We think there will be a more diverse range of companies generating the returns, not just the Magnificient Seven stocks which have driven the majority of the earnings growth in the S&P 500.

Geopolitical risk remains high, as we will discuss later in this article. In particular we look towards November and the midterm elections in the US which could put pressure on Republicans’ grip on power.

We should also see a ruling from the Supreme Court on Trump’s tariffs. Ruling against at least some of the tariffs will be good for markets. Trump has floated the idea of giving tariff revenues to fund rebates to taxpayers. Rebates in conjunction with tax breaks will help the bottom income consumer who has experienced the greatest inflation hit, due to their spending being more focused on rent, food and energy (which have experienced the highest increases).

So called fiscal dominance and the moves in bond market yields will be key. With the criminal investigation into Federal Reserve Chairman Jerome Powell, we would have thought bond yields would push up much higher, but they have not. This is likely because the next incoming Fed Chair in May still won’t be able to pull interest rates down to 1%, as Trump would want them to.

Japanese Prime Minister Sanae Takaichi has opted to call a snap election in February, looking to consolidate her power in government which will allow her to more easily push through her fiscal spending plans. Government bonds with longer maturities have been rising on this news as they fear it will push inflation up and cause rates to stay higher for longer. There is also concern over Japan’s huge debt burden. As we have said before, a high debt load is manageable if interest rates are low. But as we are seeing globally, if interest rates are high a greater proportion of tax receipts gets spent on paying interest. Demand for recent 30-year government bond auctions has not been as strong as investors are preferring to hold shorter dated debt.

In the UK, local elections in May could result in tax changes from the Labour government as they look to garner support. This is in the back of investors’ minds and already volatile long term bond yields will push up even higher if tax rises do not materialise. The UK market had a strong 2025 and with defence continuing to be a dominant theme we expect this to continue.

Growth in Europe could slow even as Germany looks to ramp up its 500 billion euros in spending. Tariff costs will eat into company margins and more developments over Greenland could hinder exporters’ performance even more. We don’t see German Bund yields coming down this year unless this spending is pulled back.

–

Areas of focus

- Smaller and unprofitable companies continue to perform well in the US. Delays in interest rate cuts could stall some of this progress.

- Investment grade corporate bond spreads remain historically tight. Increased issuance from AI related companies could widen this spread if supply outstrips demand. High yield bond issuance is likely to be lower and could offer better returns, at the expense of higher credit risk.

- Global government bond yield curves continue to steepen as investors sell longer dated debt over fiscal and inflation concerns.

- Defence companies continue to look attractive, but we question how much future earnings growth has been priced in already.

- Restaurants and airlines struggled last year as consumer demand is still relatively weak.

- Divergence in technology companies will continue in 2026 as the winners and losers become clearer.

- Global emerging markets returned strong growth last year. A weakening in the US Dollar and lower US interest rates will help these returns to continue. Are emerging markets a US diversifier trade? We do not think so, as the dynamics and risks are far too different. They are a trade in their own right.

- Gold and silver continue their strong rallies, defying expectations (ours included). These ‘emotional assets’ started off as geopolitical hedges but are now more akin to a meme stock.

- The US Dollar has weakened and may continue to do so given trust in the US is waning. Higher interest rates will provide fundamental support though.

–

Asset Class Returns

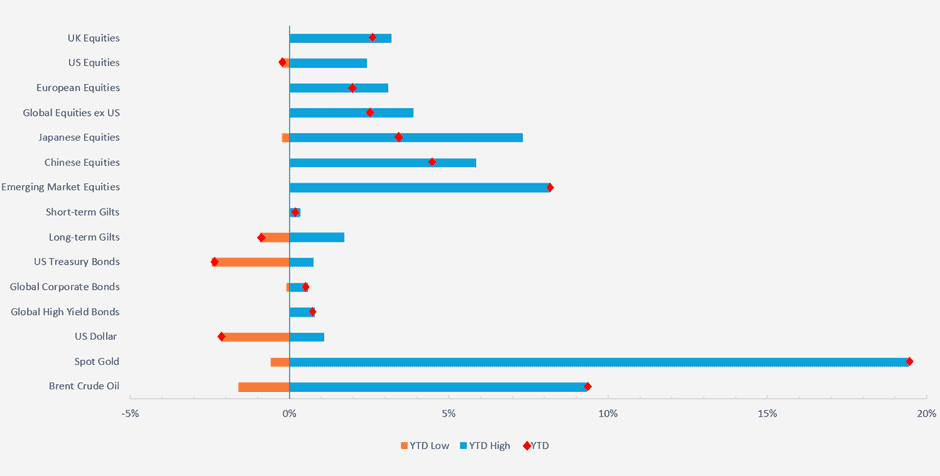

Selection of assets 2026 YTD returns and range of returns as at 28.01.2026 (the two ends of the bars represent the range of YTD returns and the red dots represent the current YTD return). Indexes used: FTSE All-Share, Russell 2000, STOXX Europe 600, MSCI World ex USA, MSCI Japan, MSCI China, MSCI Emerging Markets, FTSE UK Conventional Up To 5 Years, FTSE UK Conventional Over 15 Years, ICE BOFA US Treasury, ICE BOFA Global Corporate Hedged GBP, ICE BOFA Global High Yield Hedged GBP, US Dollar Index, S&P GSCI Gold Spot & S&P GSCI Brent Crude Spot. Returns hedged back to GBP with exception of US Dollar which is in US Dollar terms. Returns based on daily data. Source – Watson French with data from FE Analytics and MarketWatch. Data correct as at 28.01.2026.

–

US

Once again the year didn’t start off quietly, with President Trump dominating the headlines.

The US launched an operation in which they captured Venezuelan President Nicolás Maduro and his wife, bringing them back to the US to face criminal charges relating to conspiracy to export illegal drugs to the US. This only happened a few weeks ago, but with all of the more recent events this seems like a long time ago.

Trump claimed that the US will run Venezuela for now and has pushed for investment in the country by US oil – investment of up to $100 billion. In response the boss of Exxon Mobil said Venezuela was ‘uninvestable’.

We think the impact on oil markets will be limited and so far, it has been. Venezuela’s daily oil output is less than 1% of the overall global output. One of the key factors needed to do business in a country is the rule of law, and with this shaky at the best of times, US oil companies are reluctant to invest in the country without US government guarantees. Other businesses such as investment banks are looking to find opportunities but will likely be led by big oil companies, as US banks have a limited footprint in the country.

A problem facing Trump is that many oil companies donated to his re-election campaign in 2024 and they now feel they are being discarded. Only the biggest companies will be able to do business and extract oil from Venezuela, as high levels of dollar investment are required. Smaller companies cannot afford this.

Further supply of oil will put more downward pressure on the oil price which may be good for consumers, but estimates put the price of oil that US oil companies need to be profitable at $60 a barrel.

We see limited impact of this on equity markets but it does highlight Trump’s interference in foreign countries. Data shows this tends to pick up when his approval rating among US consumers is low. Trump has raised further warnings over buying Greenland and interfering in Cuba and Colombia as well. We think this highlights one of the key risks we will face again this year – that of heightened geopolitical risk.

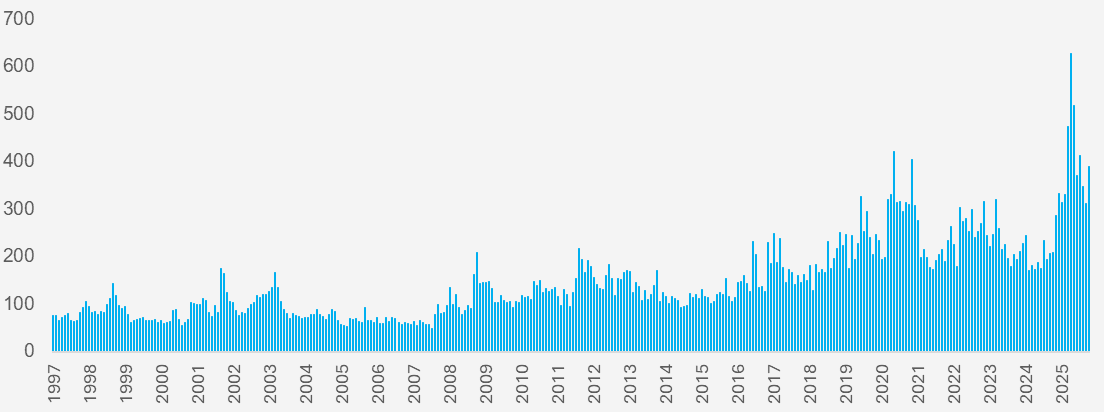

The Global Economic Uncertainty Index tracks global uncertainty by looking at key words in global newspapers in 18 major economies weighted by GDP. Based on this measure, policy uncertainty is at its highest level by far since the data started in 1997. The level of uncertainty has been rising over time and the frequency of elevated/extreme levels of uncertainty has picked up markedly since late 2024. This is unsurprising given that around this time Trump was elected as President. The general upward trend points to a diverging world and the more volatile environment we are in.

Chart showing the Global Economic Policy Uncertainty Index. This is a news flow-based index which measures the relative frequency of global newspaper articles which contain a trio of terms related to the economy, policy and uncertainty. 18 major global economies are included, and this series is GDP weighed. The y-axis shows the index level and the x-axis the year. (Source – Watson French with data from Economic Policy Uncertainty. Data runs from 1997 to 2025).

Defence companies were rocked as Trump stated that they should not engage in share buybacks nor pay dividends until they accelerate the production of military hardware. He did however say that he wants US defence spending to increase by 50% to $1.5 trillion, which will support defence companies if it materialises.

Further to this, home builders – and in particular private equity companies engaged in purchasing residential properties – suffered as Trump wanted to restrict the purchase of single family homes, meaning that institutional investors were banned from doing so.

Along with geopolitical risk we see continued industry-specific risk from White House interference. It is important not to trade on what Trump says. Things can change quickly, as we saw with defence companies.

The TACO trade (Trump Always Chickens Out) played out frequently last year. Trump would do something to cause fear in markets and markets would drop. Trump would then back down and investors who had bought the dip would then benefit from the upswing in markets. The problem with this is it can encourage Trump to go further and do more, as he thinks markets will pick back up. They will… until they don’t. FAFO – (Fool… Around and Find Out) is the latest acronym.

There are also questions being raised about Trump’s state of health, with a recent blunder of referring to the wrong country when speaking about Greenland (he said Iceland) being covered up by the White House Press Secretary Karoline Leavitt.

In economic news, we saw the first complete picture of the labour market since the government shutdown distorted the data. The unemployment rate fell from 4.5% in November to 4.4% in December while jobs added were 50,000 in December, below expectations for 73,000 jobs.

This allowed the Fed to keep rates on hold at their recent meeting with their statement indicating that they are happy to stay on hold and take a cautious approach for a while. We believe there may be only one cut this year, if any at all. With other global economies cutting rates this should provide some support for the US Dollar.

Relative to historical data, the number of jobs added has been weak. Throughout 2025 the US economy added 584,000 jobs, which is an average of 49,000 a month. In 2024 the average was 168,000.

It is not clear why job growth has slowed. Markets are leaning towards the reduction in immigration and increased government layoffs, rather than the worse scenario where the private sector demand for labour has dropped.

The White House has intensified pressure on the Federal Reserve, in particular its Chairman Jerome Powell, with the Department of Justice opening a criminal investigation into whether he mislead the Senate over cost overruns related to the renovations of Federal Reserve buildings. Gold and silver have pushed higher on this news but equity markets have remained fairly flat.

This is likely another attempt by Trump to push interest rates lower by pressuring Federal Reserve members. The risk comes when Powell steps down in May and Trump appoints a new Chairman. Will the Fed be able to stay independent?

It is impossible to say, but if there are rate cuts due to White House interference we will see bond yields quickly rise over future inflation expectations, along with a weakening in the US Dollar. These effects would be bad for equity markets, especially for the unhedged sterling investor. We think this is unlikely given the way interest rates are voted on by the Federal Open Market Committee. Markets have not reacted too much to the probability of Federal Reserve independence waning.

US CPI came in at 2.7% for December, still showing that the effect of tariffs has been muted due to businesses absorbing costs. The core CPI figure (which excludes volatile food and energy costs) remained at 2.6%, the same as the prior month and below analysts’ expectations for a 2.8% increase.

This is the first clear picture of inflation since the government shutdown distorted data and some readings were missed, but as data is collected at different frequencies next month may show some moves.

This will allow the Federal Reserve more room to focus on the employment side of their mandate, but we may start to see businesses increase prices as they tend to do so at the start of the year.

It may be good for consumers that businesses have absorbed some of the price increases, but the flipside of the argument is that unless businesses can become more productive and efficient, it will lead to lower earnings and margins, which should adversely impact their stock prices.

Some of the data shows that AI productivity is already picking up, in a similar fashion to when the internet and PCs were first introduced.

It looks to be a busy year for corporate bond markets. In the US, investment grade borrowers raised more than $95 billion in the first week of January, the highest volume since May 2020. Forecasts for full year issuance could put the value of debt raised above $2 trillion.

Although there is a lot of liquidity in markets, a large increase in supply will put pressure on corporate spreads and we will likely see widening from their current tight levels. We have also seen lots of activity in Europe and in particular from financial institutions. For investment grade borrowers, fundamentals remain strong and so the risk of defaults looks low. The biggest risk is how much spreads widen by.

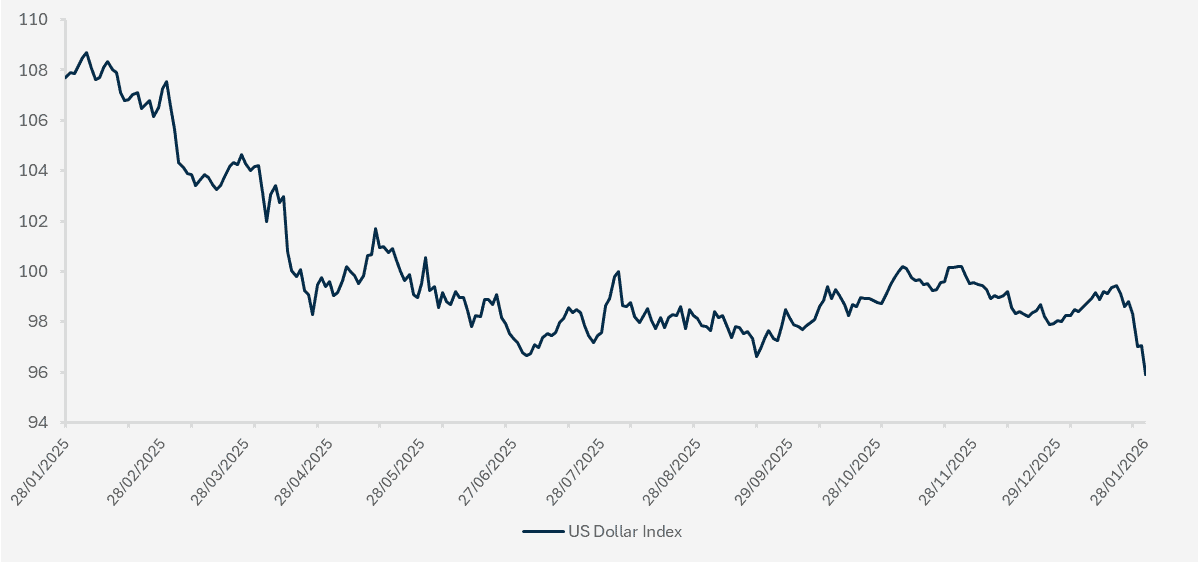

Having steadied itself after a dismal start to 2025 the US Dollar has once again depreciated against a basket of major currencies.

Chart showing US Dollar Index over a one-year period. The US Dollar Index measure the US Dollar against six major currencies. (Source – Watson French with data from Investing.com. When the blue line falls this shows a weakening in the US Dollar. Data period 28.01.2025 – 28.01.2026. Yield based on daily opening rates. Data correct as of 28.01.2026).

Around this time bond yields briefly sold off along the curve, with both movements coinciding with the Greenland narrative. Gold has started the year in stellar form and we firmly believe this is a momentum trade now, not a debasement trade. If we were seeing debasement we would be seeing a greater sell off in US treasuries along the curve, but we are not seeing this. A cheaper dollar also makes it cheaper for non-US investors to buy gold as it is denominated in dollars, which is a tailwind.

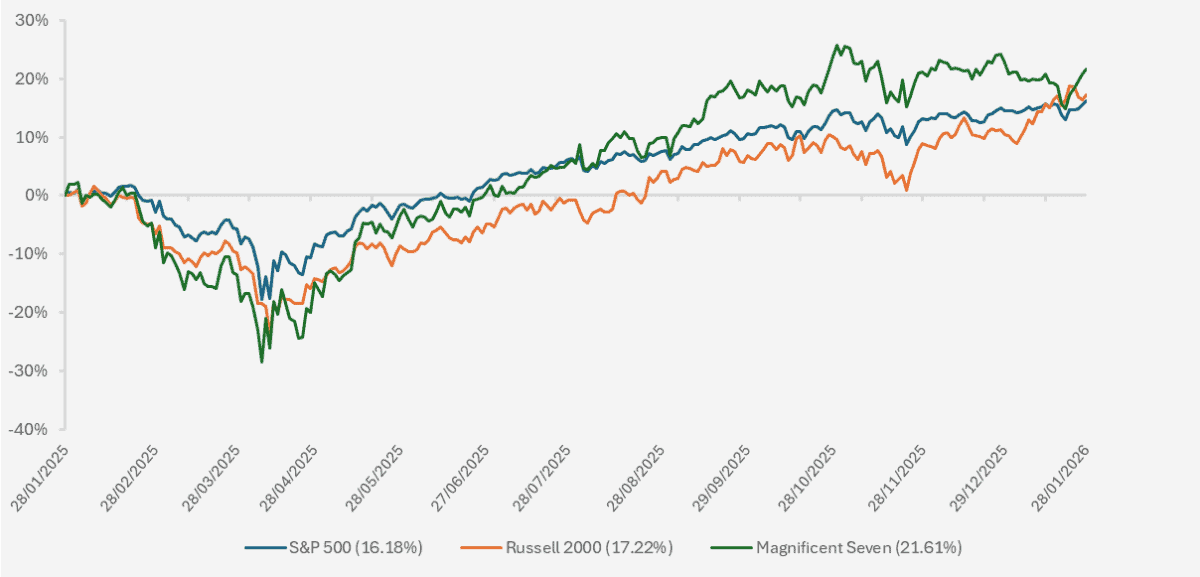

Chart showing performance of various US equity indices and stocks (S&P 500, Russell 2000 (small cap index) and Magnificent Seven stocks) over a one-year period. (Source – Watson French with data from Investing.com. Magnificent Seven stocks are represented by the Roundhill Magnificent Seven ETF. This is used as a proxy and is not advice nor a recommendation to purchase this asset. Returns are in US Dollars. Return period between 28.01.2025 – 28.01.2026. Data correct as of 28.01.2026).

Since September the Magnificent Seven technology stocks as a whole have been flat while smaller companies have rallied. We still do not remain fully convinced on the investment case for smaller companies, with higher rates, slower hiring, tariffs and political uncertainty weighing on growth.

–

UK

Starting the year and looking backwards, the UK has got off to somewhat of a good start with GDP growth for November coming in at 0.3% month on month. This was higher than the 0.1% expected by economists and came from growth of 0.3% in services and 1.1% in production.

Inflation for December picked up from November’s reading of 3.2% to 3.4%, a step in the wrong direction. Some of this is to do with price increases over the Christmas period and the increase in the Tobacco Duty, and was previously forecast by the Bank of England.

Core inflation remained at 3.2% but services inflation picked up to 4.5%, up from 4.4% the previous month.

In the short term this puts less pressure on the Bank of England to cut interest rates at their next meeting, but markets still expect the next rate cute to come in June, not the Bank of England’s next meeting in February. Although tariff threats have now been resolved, ongoing uncertainty over increased tariffs from the US in relation to Greenland could see growth drag and inflation rise if these tariffs are implemented.

For the UK stock market and in particular the FTSE 100, this tension can weigh on company earnings as the dollar is again weakening against the pound. As the majority of the earnings of FTSE 100 companies come from overseas this will decrease their value when they are exchanged back into pounds.

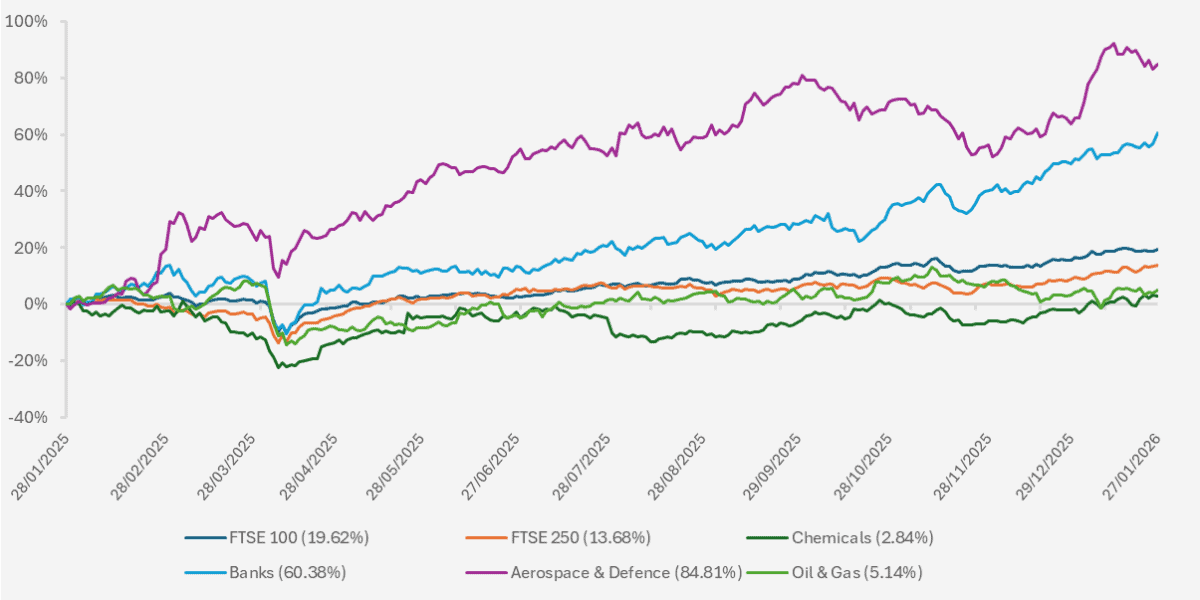

Chart showing performance of the FTSE 100, FTSE 250 indices and various FTSE All Share sub-sectors over a one-year period. (Source – Watson French with data from Investing.com. Returns in Pounds Sterling. Data period between 28.01.2025 – 27.01.2026. Data correct as at 28.01.2026).

In 2025 UK equities posted solid returns, but if we look at some of the fundamentals things were disappointing. For example, earnings growth in the FTSE All Share was expected to be 9%, but by the end of the year this was revised down to zero. Banks and defence companies performed well but transport, mining, oil and gas and chemicals performed poorly in earnings terms. Given this disparity and the underlying holdings in the FTSE 250 being dominated by investment trusts, we continue to believe in an active approach to UK equities.

Larger companies look relatively more expensive than smaller companies and this could offer some opportunity further down the market cap. However, we continue to believe that higher financing rates, labour costs and increased taxation weigh more heavily on these companies and there is a reason they are cheaper. Larger companies have been driven by the strong performance of banks and defence companies and they have a better ability to maintain their dividends in more difficult environments. For smaller companies and consumer cyclicals to do well, interest rates have to be lower.

Still, expectations for stronger growth from smaller companies have been on the merit of earnings, not on a lower interest rate environment. We have seen this narrative for the past two years and until investors put their money where their mouth is (net fund flows in UK equities last year were negative for the tenth year in a row) our conviction remains subdued. Furthermore, high M&A activity in the UK market means that opportunities in the small cap space are disappearing.

Calculations from Man Group show that if the pace of M&A and share buybacks continues as it did in 2025, in thirty years there would be no market left. Many large UK investors are reallocating their UK exposures and reducing their home bias. We think this is a reactive decision based on recent overseas performance. At a portfolio level this greatly reduces the exposure to value stocks and makes the portfolio more core-focused. Growth stocks have performed well for many years but over the longest periods it is dividend reinvestment which has compounded into the best returns, something the UK is very good at.

In a world of growth, the UK looks attractive as historically 75% of its total return has come from dividends over the past 20 years (for the MSCI World index, the contribution from dividends was 48%).

–

Japan

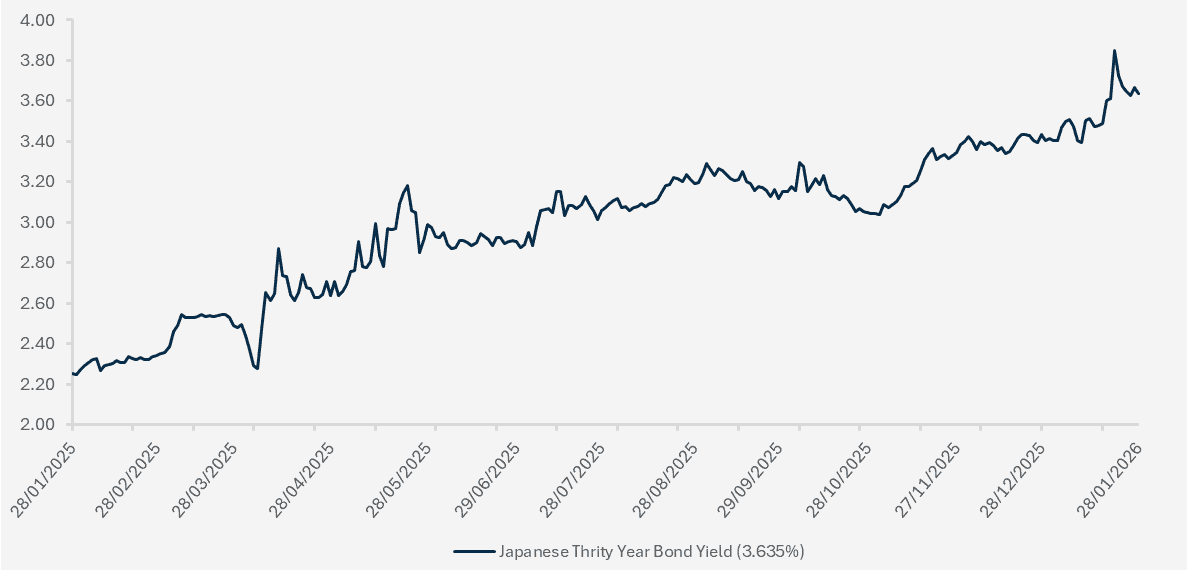

Prime Minister Sanae Takaichi called a snap election in Japan in a bid to solidify her grip on government at a time when her popularity among voters is high. Winning her party more power in government should give her the ability to push through her spending increases and tax cuts. At the same time, long term Japanese bond yields have risen to levels not seen in a long time.

This is happening because Takaichi plans to cut taxes and increase spending. She deems this will be ‘responsible fiscal expansion’ but with inflation continuing to pick up, these actions increase the risks of higher and sticky inflation. Higher inflation will require higher interest rates to bring it back to target.

Interest rates are on the rise in Japan having spent decades at near zero levels. Takaichi has pressured the Bank of Japan to not raise rates. Higher interest rates will put pressure on the cost of debt for consumers and businesses and risk bringing economic growth down. There is also the risk that if businesses are facing higher interest costs then they will stop annual pay rises, putting downwards pressure on wage growth.

Japan is not immune from the geopolitical uncertainty we have seen coming out of the US. They have also recently angered China and risk backlash here as well.

Chart showing movement in the Japanese Thirty Year Government Bond yield over a one-year period. (Source – Watson French with data from Investing.com. Yield in brackets is opening yield at 28.01.2026. Data period 28.01.2025 – 28.01.2026. Yield based on daily opening yields. Data correct as of 28.01.2026).

The majority of Japanese government debt is issued with maturities of less than ten years, so why do we care about longer term yields rising? As markets say, what happens in Japan doesn’t stay in Japan.

For years, investors and in particular big Japanese institutional investors waited for Japanese bond yields to rise from their historic lows. At such low levels these investors could get a better yield by buying overseas bonds such as US Treasuries and hedging the currency exposure. This resulted in a build-up of overseas bond holdings by Japanese investors. With the Yen now weakening and Japanese bond yields looking more attractive, there is less of a reason for them to hold overseas bonds.

Money is therefore starting to flow back into Japanese bonds and the higher the yield goes, the more attractive the bonds look. For US Treasuries and other global government bonds this will mean Japanese investors selling their overseas bond holdings and therefore increasing the yield on these bonds. This has clearly caught the US administration’s attention, with US Treasury Secretary Scott Bessent speaking to his Japanese counterpart regarding the bond sell-off.

Recently the US Treasury instructed the New York Federal Reserve to reach out to banks to see who could offer the best Yen-US Dollar rate. The US rarely intervenes in overseas currency markets, but the Treasury has a $500 billion facility to do so.

Japan is the largest foreign holder of US Treasuries, accounting for 12.8% of the total holding. It also holds a lot of US corporate debt as well and so both markets could be affected by rising Japanese yields.

If Takaichi doesn’t prove to markets that she can be responsible with stimulus we could see another “Liz Truss” moment – except this time, the effects would be more global.

The Yen has weakened against many major currencies, which is concern. A weaker currency makes exports more attractive but makes imports more expensive, adding to import inflation. The Bank of Japan could intervene in markets to support the Yen by increasing rates, but this would damage growth and increase borrowing costs. Increasing bond yields combined with a weaker Japanese Yen shows investors are selling Japanese assets.

Investors have long been concerned with Japan’s gross debt levels, which in 2024 stood at 236% of GDP. However, as we mentioned previously, Japan’s assets have grown above the debt level and a large proportion of the debt is held domestically. The problem now surfaces with potentially higher interest rates. Financing a debt which is that large is costly and the more debt the Japanese Treasury issues, the bigger the burden becomes.

Another area of focus is hedge funds and other institutional investors. The Yen has been used in recent years as a funding currency. Investors will borrow money in cheap Yen to buy overseas assets. We saw in August 2025 this trade unwind and cause big drops in markets. This could happen again should we see the Bank of Japan hike rates unexpectedly.

Last year rising yields benefitted Japanese banking stocks as their net interest margin increased. This year will be supportive for banks again but with markets already pricing in most of this yield increase, we will need to see even more weakening in the bond market for banks to outperform.

We continue to expect corporate reforms and we seeing evidence of this in markets with higher dividends, share buybacks and big conglomerates selling off their unprofitable businesses. Stocks are not cheap in Japan and higher bond yields could put pressure on more expensive technology stocks.

–

Robert Dougherty, Investment Director

February 2026

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested. Data is correct at time of writing and cannot be guaranteed.