It is common for stocks to rally in bear markets. Over the past 95 years during bear markets stocks have rallied on average 18% before dropping back down. The NASDAQ and S&P 500 have rallied just under 15% and are now dropping back.

In mid-July investors were more optimistic that the Fed would not continue to raise rates at high levels as inflation had cooled slightly. At the Jackson Hole symposium Fed Chairman Jerome Powell stated that they will bring inflation back down, even if it damages the economy.

From someone who was adamant they could avoid a recession while bringing inflation down this is quite a change in stance. The Fed’s previous inaction is prompting increased action now, and the tightness of the labour market will determine what actions the Fed takes next.

Elsewhere, in the UK inflation continues to rise. Citi Group forecasts inflation to reach 18% in 2023, although this is not the consensus view. Consumer confidence continues to plummet amid the backdrop of rising interest rates, rising living costs and an increasing energy price cap.

Consumers are looking to the government for further help as the current and proposed support packages are not enough to lift many households from fuel poverty.

In Europe, shortages of gas continue to put huge pressures on economies. German industrial companies previously had a competitive advantage as they could source an abundance of natural gas from Russia at cheaper prices. Now this advantage has gone, the cost of energy is 15 times higher, growth is slowing in China and US interest rates are rising. This combination of problems is causing some industrial companies to halt production completely.

Area of Focus

- Investors remain cautious on equity over an increasingly gloomy outlook. The long-term outlook remains positive.

- The US Dollar continues to gain ground on other major currencies.

- US treasury yields are expected to increase with a steepening of the yield curve.

- Chinese fixed income is no longer looking attractive compared to other developed market bonds.

- Investment grade bonds exhibit better characteristics than high yield bonds in an increasingly difficult economic backdrop.

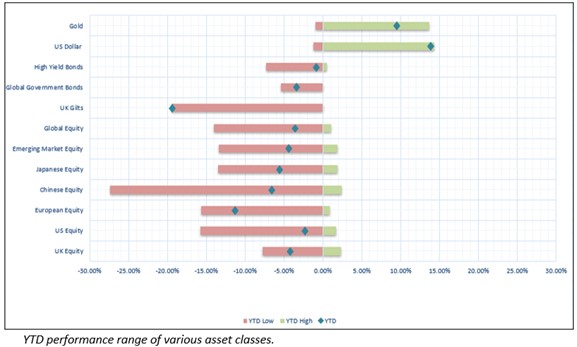

We put together the chart below to illustrate the considerable volatility seen across all major asset classes this year.

Essentially, the red bars on the left show the lowest point reached for each type of investment since the beginning of the year, and the green bars on the right show the highest point attained.

The blue diamonds then pinpoint where in this range each asset class is at the time of writing – most showing some signs of recovery, but still firmly in negative territory.

UK

The UK economy continues to struggle under inflationary pressures. The cost of living crisis, fuelled by soaring energy prices, is not coming to a plateau yet.

Ofgem, the UK energy sector regulator, has stated that there will be an 80% increase in the gas and electricity price cap from October. Average households’ annual gas and electricity bill will rise to £3,549.00 from £1,971.00 at present. This sharp increase is the result of further Russian restrictions on energy supply into Europe.

That said, energy prices have slightly moderated which has brought some stability across Europe, for now.

As there is no foreseeable end to the Russia-Ukraine conflict, industry forecasters are predicting that energy price caps will continue to rise to over £6,600.00 by spring next year. The chief executive of Ofgem, Jonathan Brearley, now claims the £15bn of government support to households announced in May will no longer be enough, as that proposal was under the assumption that price caps would reach only £2,800.00 by October 2022.

However, the cost of energy bills does not only affect households directly, but businesses too. Business’ costs will rise. Those businesses which have pricing power can transfer this to consumers, but those that do not will find their profit margins squeezed.

Inflation will rise along with the changes in energy caps, with Citi Investment Bank predicting inflation rates of over 18% in 2023. Citi assumes that BoE base rates will be subsequently forced up to around 7% if higher wages are demanded.

Currently the market is pricing in the BoE base rate to reach around 4.5% by the end of 2023.

With the current climate it is difficult to see a clear path that avoids a recession. The way in which energy prices are heading and the influences of inflation and interest rates, it seems likely that confidence and consumption will remain low and GDP growth slow for a number of years.

The new prime minister Liz Truss has a tough job ahead. Though she has pledged tax cuts to help consumers, investors are wary. We will have to wait to see how economic conditions develop, what further support she will offer and how the BoE will fare, with Liz Truss having already voiced her critical assessment of their poor job of managing inflation thus far.

The pound continues on its slippery slope, losing 5% against the US Dollar in the last month. While this is bad for UK inflation and exports, investors who hold overseas equities will see gains on their positions due to the currency movements.

For example, if an investor had purchased one share in JP Morgan Chase one month ago, it would have cost them £93.57 (with an exchange rate of 0.82 USD/GBP, costing $112.74). Today if the investor had sold the one share at $113.71, the investor would have made a 0.86% gain. However, when the investor changes this back into pounds sterling the investor would have £98.98. This would represent a 5.78% gain, which is 4.92% from currency movements alone.

Despite the FTSE 100 being one of the best performing major indices YTD, the FSTE AIM 100 has experienced a significant decline. With the UK nearing a recession, the outlook for these smaller early-stage growth orientated companies does not look to get better any time soon.

Europe

Energy woes plague Europe and the outlook is not getting any better. Like the US Fed, European Central Bank members are focused on bringing inflation down with higher interest rate increases, accepting the fact that this may cause economic damage.

Rates are expected to rise by 0.75%, bringing the base rate to 0.75%.

The G7 have just agreed to implement a price cap on purchases of Russian oil. This initiative has not only been supported by European countries but Canada and Japan as well.

Despite this, commodity prices (excluding natural gas) have had a meaningful decline, with oil prices back below their pre-Ukraine war levels.

The Eurozone unemployment level hit an all-time low at 6.6%. This shows the European labour market is resilient in the face of rising energy costs and conflict. However, assessing the future of interest rates and the likely rises, it is predicted that sharp wage increases will be demanded as the labour market tightens further.

To combat cost of living difficulties for consumers, Brussels have suggested redirecting inflated profits from power companies back to consumers in the form of a price limits and subsidies. This is an attempt to revive the European economy and inspire GDP growth.

Germany has adopted the above policy by capping the level of profits on companies using wind, solar, biomass, coal and nuclear energy. These firms do not use natural gas to generate electricity but as the price of natural gas has risen to heightened levels, these firms have been able to charge much higher electricity prices based on natural gas prices.

This windfall tax will help to fund the EUR 65 billion support package the German government is implementing to help support struggling consumers.

The German DAX 30 has been the worst performing major stock index this year. The index has rebounded slightly over the last month but the yields on German Government bonds have continued to rise, albeit with slight drops over the last month.

US

The rally in US equities since mid-June has hit a slump as the NASDAQ 100 and S&P 500 have dropped over 5% again in the last few weeks. This follows comments from the Fed Chairman Jerome Powell where he suggested that even though inflation data for July showed it had slowed slightly to 8.5% from 9.1% in June, the Fed was still going to be aggressive with interest rate rises. Inflation will need to moderate before rates are stabilised, even if this comes with some economic damage.

This sent the US dollar index (the value of the US dollar against a basket of other currencies) to a 20-year high.

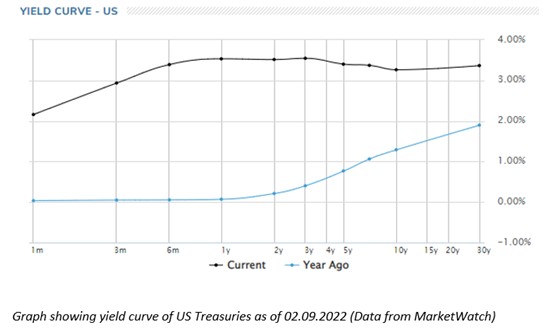

Yields on US government debt have continued to rise with yields on the 2-year note rising to their highest level this year at 3.5%. The yield on the 10-year note is slightly lower at 3.2%.

Some investors are seeing this as a buying opportunity but earlier in the year this was the same case and yields have continued to rise. The “term premium” for holding US Treasury notes will likely increase and the yield curve may steepen.

Investors are uncertain whether the Fed will raise interest rates by 0.75% as they have done at their last two meetings, or whether they will moderate back to a 0.50% rise. Inflation and payroll data for August will be key in this decision. It may be that the Fed continues with the 0.75% rises to make up for their lack of action in the past year. If this is the case yields on US Treasuries will likely rise further and US equities will decline in value again.

The market has currently priced in rates to reach 3.5% by the end of this year, 1% higher than it currently is.

Recent economic data has pointed to further slowdowns in the US economy.

Data looking at the sales of US homes showed an annualised drop of 12.6%, a steeper decline than the 2.5% drop forecasted by analysts. The Purchasing Managers Index came in at 44.1 for August. Anything below 50 shows a contraction in business activity.

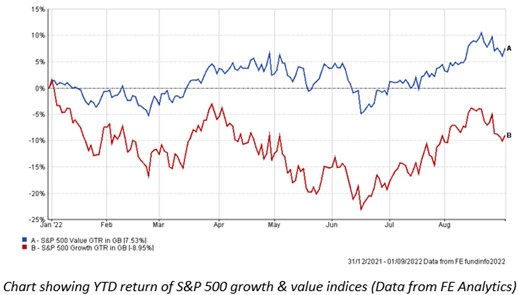

As we can see from the graph below, companies exhibiting value characteristics have continued to outperform growth stocks. While the return on growth stocks has been negative all year the value stocks have only drifted into negative territory for two and a half months.

China

Accounting for a quarter of the country’s GDP output at its peak, the Chinese property sector is set for a potentially large contraction. Amid rising prices and reduced consumer demand, highly leveraged property companies are struggling to refinance so they can complete existing construction projects and service their high risk debts.

Property sales have declined by as much as 30% this year. The property crisis has become a circular problem wherein consumers are delaying purchasing properties over the fears that properties will not be finished and the companies developing them will be insolvent. Companies are not generating enough revenues to service their existing debts and to finish construction projects, and so the cycle continues to get worse.

In a bid to boost demand the government has cut the mortgage lending rate for the second time this year. The five-year benchmark loan prime rate has been cut from 4.45% to 4.30%. This will reduce the financing costs for new homeowners but will not affect existing mortgages until next year.

Government intervention via easing mortgage rates and a proposed bailout package is unlikely to be enough to bolster confidence and solve the ongoing issues. The government needs to send a strong message of confidence and take forceful action to support the economy.

It is easy to think of the 2008 financial crisis when we talk about a housing crisis. The effects of this were globally widespread and caused significant hardships for consumers and businesses alike.

Each crisis has different contributing factors which mean the effects (and how widely these effects are felt) will vary.

In this case the risk of the Chinese housing crisis evolving into a deep and persisting crisis are not high as Chinese consumers have historically had high levels of savings which can be used to service interest payments when they fall due.

The risk of a property crisis spreading to cause global financial distress is also low. Major Chinese banks are mostly state-owned and will not be allowed to fail. This would otherwise be a risk as the banking sector is exposed heavily to the property sector.

We may see higher prices and a lack of supply to the rest of the world if Chinese productivity drops, but this will only add to the inflationary pressures around the world and not create new and yet unknown problems.

Further to this, only about 5% of Chinese equity and bonds are held by overseas investors. While creditors of the Chinese property companies will experience losses, the ripple effect should be relatively small compared to past crises.

Offshore holders of Chinese property developer Evergrande are becoming frustrated by a lack of communication and action from the struggling real estate developer. Nearly $20 billion in debts are owed to offshore holders. The Chinese company is prioritising onshore debtholders and residential construction projects and is unlikely to agree to offshore creditors restructuring demands.

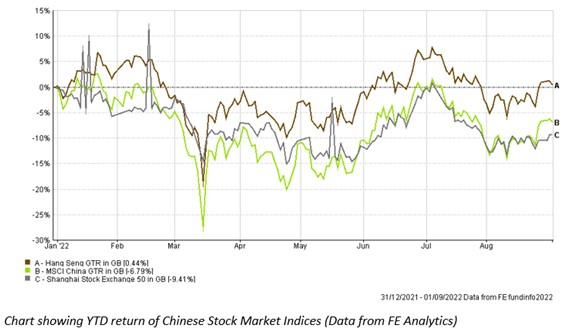

Chinese stock markets had initially recovered their losses this year by July but have since dropped back into negative territory as lockdowns and weak economic data dampen the short-term investment appeal again.

The short-term outlook depends on how the government handle the indebted property sector, what further support they will give to encourage demand and provide stability and how long the zero-covid policy continues for.

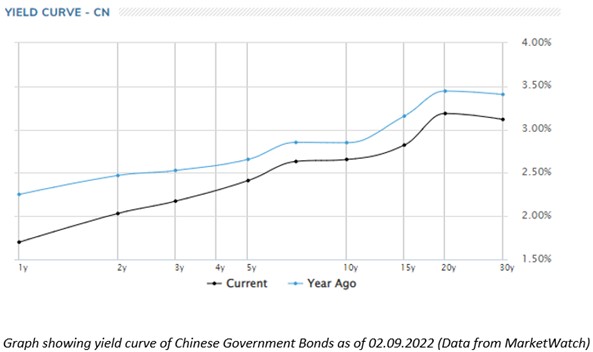

Chinese fixed income has also given up the yield advantage it had over other developed market bonds in the light of the slow government response to monetary loosening.