Firstly, a bond is essentially a loan – usually to a government or a large company.

Governments and companies issue bonds to raise finance in the form of debt and pay interest throughout the term of the bond, before finally repaying the capital.

The value of the global bond market is estimated to be $128.3 trillion, with over $950 billion traded on the US fixed income markets as of July 2022. Compare this to the value of the global equity markets which stands at $108 trillion (listed companies).

The biggest market in the world is the foreign exchange (forex) market. In April 2019 research showed that the daily average volume of trading on the forex market was $6.6 trillion per day.

The debt market is bigger than the equity market, but the forex market is bigger still.

How bond yields and prices interact

A bond’s yield is the return that can be earned by investing in a bond. The yield takes into account any coupons (interest paid for holding the bond) that will be received and any capital gains or losses that will be achieved on holding the bond to maturity (par value minus purchase price).

A bond’s price is what an investor pays for a bond on the secondary market. This is different to what will be received by the investor on the maturity of a bond. When a bond reaches its maturity date a fixed amount of £100 or £1000 per nominal holding will be paid out, regardless of the price the investor paid for the bond. This is called a bond’s “par value”.

The price an investor pays for a bond is a big determinant of the return an investor can expect.

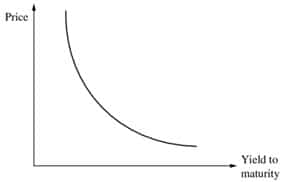

We can draw an inverse relationship between the price and yield of a bond. If a bond’s price increases then the yield will decrease, and vice versa. If an investor pays more for a bond and will receive the same coupons and the same £100 at maturity, then the yield on this bond will be lower.

Relationship between bond price and yield (note the convexity of the curve)

Yields move as investors’ outlook on various factors change. Some of the key factors which affect bond yields are interest rates, inflation levels, general economic conditions and credit risk (which is the risk that the borrower will default, i.e. not repay the capital).

Presently interest rates and inflation are increasing and this is causing bond prices to drop, so yields are moving higher. The economic outlook is also looking negative as well.

Bond coupons are paid at periodic dates in the future and the final payment of the par value at maturity can be many years in the future, depending on the bond’s maturity.

Some bonds have maturity dates of up to 50 years. When inflation is higher, the real value of these payments decreases and investors will move out of longer-dated bonds into shorter-dated bonds and other securities which provide better inflation protection.

For example, a bond which has 20 years to maturity (assuming a constant inflation rate of 2%) will have a nominal par value of £100 at maturity, but this will only be worth £67 in real terms due to the effects of inflation. The par value of a bond with two years to maturity will be worth £96 in real terms at maturity.

When interest rates increase, bond yields to rise because:

- An increase in the return offered by safer cash assets provides a more attractive return than before

- New bonds will be issued with higher coupon rates, which makes existing bonds with lower coupons less attractive. If the yield on a bond is below the current market rate then an investor will sell this until the yield matches what is being offered at the equilibrium rate.

Not all bonds are created equally, however. Different bonds are affected by these changes in different ways. Bonds with longer maturities and lower coupons are more sensitive to changes in interest rates than bonds with shorter maturities and higher coupons (all else being equal).

This sensitivity is measured by Macaulay Duration. The higher the duration the more sensitive a bond’s price is to changes in interest rates. A duration of 5 means that for every 1% increase in interest rates, the price of the bond will decline by 5%. This is due to the convexity of bond prices.

Bond prices are convex because an increase in interest rates results in a price decline that is smaller than the price gain resulting from a decrease in interest rates of the same magnitude.

This curvature in bond prices reflects the fact that progressive increases in the interest rate result in progressively smaller reductions in the bond price (at higher rates a bond is worth less, so an additional increase in interest rates operates on a smaller initial base price, resulting in a smaller price decline).

The longer the time to maturity, the lower the real value of future coupons and the final payment of the bonds par value.

If a bond has a lower coupon then a greater proportion of the yield will come from the difference in the price paid for the bond and the par value paid at maturity (i.e. the capital gain). The higher the proportion of the return that will be received on maturity, the lower the value of the bond will be as this future return will be worth less in the future than a higher coupon that is received today.

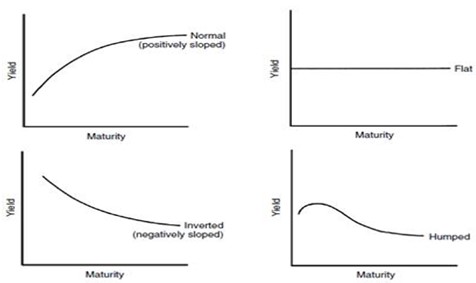

A yield curve plots the yields of bonds of the same credit quality but with different maturities. The shape of a yield curve gives indications about future interest rates and economic conditions. The four main curves are flat, negative, positive and humped.

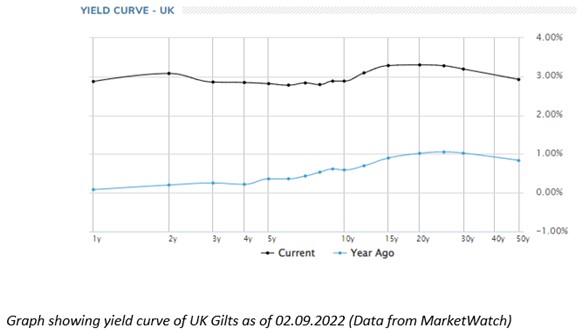

The graph above shows the current yield curve for UK Gilts. The graph is quite flat and this tends to happen when a yield curve in moving between being positive and negative i.e. there is economic uncertainty. In the UK the Bank of England are increasing interest rates but how long they will continue to do so and the magnitude of future rate rises remains uncertain.

Bond yields also have an effect on equity prices.

As bond yields rise equity values tend to drop. Bond yields are often used to value equities and they represent a “cost of capital”. When yields rise the equity cashflows are discounted at a higher rate, which reduces their present value. This is why we have seen equity values so high over the past few years (because bond yields have been historically low).

Also equities are perceived as being a riskier investment then bonds. If bonds are yielding a higher return then rational investors will move from risky equities into less risky bonds.

Equities may be perceived as more “exciting” than bonds, and they are certainly commented on more frequently by investment professionals and the media, but bonds behave differently and so they are just as important for any well-diversified investment portfolio.

Robert Dougherty, Associate IFA

September 2022

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.