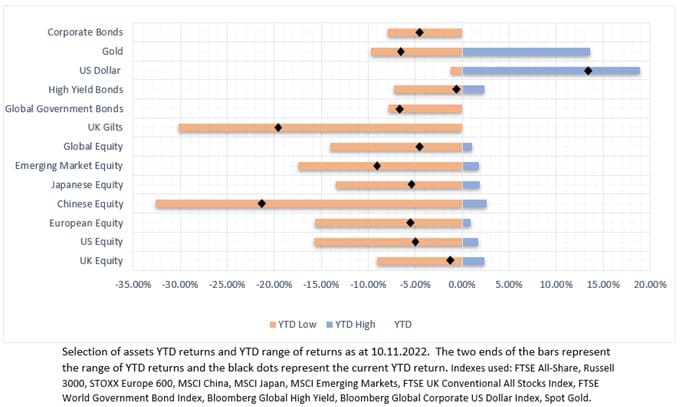

Areas of Focus

- Demand for global corporate bonds increases as their higher yield and high coupon rates make an attractive addition to portfolios.

- While high-yield bonds are also relatively good value, their lower credit ratings amid a global downturn increases their default risk.

- Technology stocks continue to fall in value amid disappointing earnings, but recent falls could present an ideal buying opportunity for long-term growth.

- Many growth focused investment trusts are trading at big discounts which could also present buying opportunities. If the discount narrows this enhances the investment return (although the opposite is also true!).

- The FTSE 100 has demonstrated strong performance this year to date (YTD) relative to other global markets.

- While European equities have rallied, near-term risks may mean these rallies prove to be short-lived.

- Chinese equity rallies have been built on a slim hope of Chinese zero-covid policies being lifted and an improved outlook for the struggling Chinese property sector.

- Falling global commodity prices has dragged the price of gold down, bringing the second top performing asset this year into negative territory.

UK

Political background

Political turmoil had continued to plague the UK with the appointment and subsequent removal of Liz Truss. Truss now holds the unglamourous achievement of being the shortest-serving Prime Minister in UK history.

While the markets have mostly corrected any negativity that was priced in, the credibility of the UK in political and fiscal terms is still damaged.

With Rishi Sunak now appointed as the Prime Minister, many investors see him as a safer pair of hands to lead the UK economy over the next two years. Scrutiny will be placed on the next budget (to be released on 17th November) and this will indicate where gilt yields are headed.

It is important to emphasise that this will have short-term effects on asset classes but will not be the driver of longer-term returns.

Economic growth & inflation

UK GDP growth for the third quarter is expected to have contracted by -0.3% which would put the UK in the recessionary phase of the business cycle. This is not a surprise for investors and a recession has already been priced into markets.

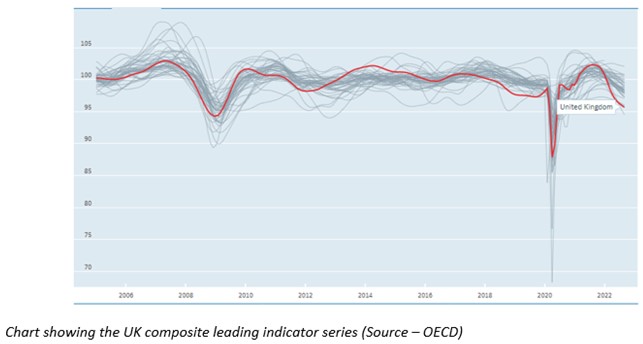

The chart below shows the composite leading indicator series. This series contains leading indicators (that is to say, economic statistics that usually precede a recession) and any major downturn usually indicates a recession is looming or in progress. As we can see below, the indicator has dropped significantly this year.

Business confidence has also plummeted sharply as the reality of rising costs and a difficult macro-economic backdrop hit home.

Production for August also fell by 1.8%, with a 1.6% fall in manufacturing contributing to the contraction in GDP.

Going forward, the economy is expected to contract by 0.2% each quarter from Q4 2022 to Q2 2023, meaning that overall GDP growth for 2023 is expected to be -0.3%. These estimates should be taken with a large handful of salt, however, as previous GDP estimates in July were for growth of 1.0% in 2023. Furthermore, these estimates do not take into account the Autumn budget details.

The scale of the downturn is not expected to be major relative to previous downturns, mostly due to government intervention in business and consumer energy costs.

UK inflation reached 10.1% in September, driven up by food prices rising 14.5%. Yields on longer-dated government bonds (most sensitive to interest rate rises) rose on this news. Falling fuel costs also helped to offset some of the increase in food prices, but with OPEC set to cut oil output by 2 million barrels per day (equivalent to 2% of global supply), fuel costs are on the rise again.

To counter this, a lack of production activity in China has meant transportation companies have not been demanding as much oil and this has limited price rises.

High inflation is expected to continue into 2023 where it will reach its peak and, according to current estimates, return to slightly lower levels by the end of the year. Inflation is then expected to stick at around the 5% mark and this will mean that interest rates will remain higher, even while the UK enters a recession.

The BoE has raised interest rates by 0.75% this month, with the base rate now standing at 3%. Guidance issued by the bank suggested that base rates will not have to rise much further in order to bring inflation back down. This is partly because of the effect the recessionary environment will have over the next few periods on reducing demand.

The Bank also said that markets have priced in greater rate hikes than the bank expects to make. This will be good news for bond sectors and should help to bring yields back down, delivering some upside for an asset class which has fallen sharply this year. Equity values should also rise for the same reason.

While this may be good news for some asset classes, the pound fell relative to the US Dollar as the US Federal Reserve took the opposite approach, and said interest rates may have to rise higher than expected.

Lloyds have estimated that house prices in the UK will fall 8% next year and that prices will then stagnate for the next 4 years. This is unsurprising given that rates on 5-year fixed mortgages are around 6.3% and inflation is at 10.1% – these high rates will negate most of the benefit that buyers will experience on any reduction to stamp duties.

The key is that prices are expected to fall, not to crash. A housing crash is most likely not going to happen yet because there is very little supply, and demand still outstrips this supply currently.

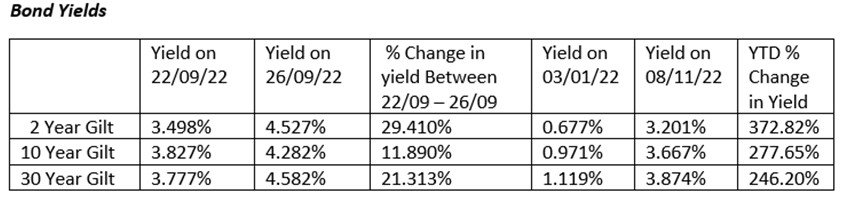

We can see from the table above how the yields on UK gilts have changed throughout the year. At the start of the year yields were low and the yield curve was upwards sloping. If we look at the fourth column, it shows the percentage change in the yields of these three gilts before and after the mini-budget was announced. Yields had increased prior to the budget due to rising inflation and interest rates.

After the budget yields rose substantially due to the fiscal concern over how the tax cuts would be funded. The BoE stepped in to temporarily restart QE to support bond prices and the yields dropped slightly; a significant move given they were planning to withdraw QE prior to the mini-budget. Since Liz Truss stepped down yields have dropped back.

Investors have continued looked at whether now is the right time to re-enter the gilt market, as yields were not expected to keep rising. With inflation expected to drop and stabilise next year yields might be reaching a peak, and so there may be some upside in gilts next year.

Currency

The GBP has depreciated markedly this year. While this is a function of a strong US dollar, political instability in the UK has contributed to its current weakness.

At the start of the year the GBP traded at 1.35 with the USD. After the budget announcement in September this dropped to 1.08, but this has since returned to 1.15.

While a low GBP has the benefit of increasing export competitiveness (by lowering the cost for foreign purchases of domestic goods), it also increases import costs and contributes to domestic inflation.

Additionally, a low GBP benefits many FSTE 100 companies which we talk more about below.

Confidence in the GBP has partially been restored, demonstrated by the 7.4% increase in its value relative to the USD. Where the pound goes from here will depend on the BoE’s stance on interest rates and what the new budget will look like.

Market movements

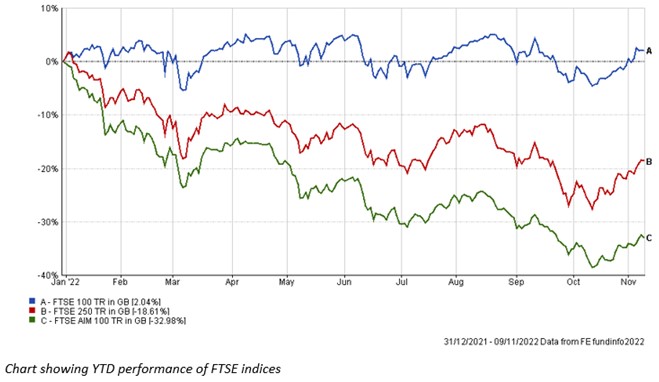

The FTSE 100 is still one of the top performing indices this year gaining 2.09% at the time of writing. In comparison the FTSE 250 has dropped by 19.00% and the FTSE AIM 100 has dropped by 32.99%.

While it may be reasonable to assume that all UK indices would move similarly to each other, we need to look at the makeup of their indices to gauge why they have performed the way they have, and where they are headed going forward.

Around 70 – 75% of FTSE 100 company revenues are derived from overseas trade. They therefore earn their revenues in other currencies, including the USD. When the USD strengthens and GBP weakens, the currency movements help to boost any profits they record. While FTSE 250 companies have around 50% of revenue derived overseas, their smaller market caps and this smaller revenue has not boosted performance by as much.

The concentrated nature of the FTSE 100 has been a big factor in its performance. Around 50% of the market cap of the FTSE 100 is accounted for by just 11 companies. The bottom 25% of the index is composed of 72 companies. YTD these top 11 companies have a positive contribution 17.33% towards the FTSE 100 returns.

Compare this to the FTSE 250 where 50% of the index consists of 72 companies, a much less concentrated index. Therefore in the FTSE 100, movement in the top 11 companies moves the index by a much greater margin. The remaining 89 companies have a much smaller impact individually.

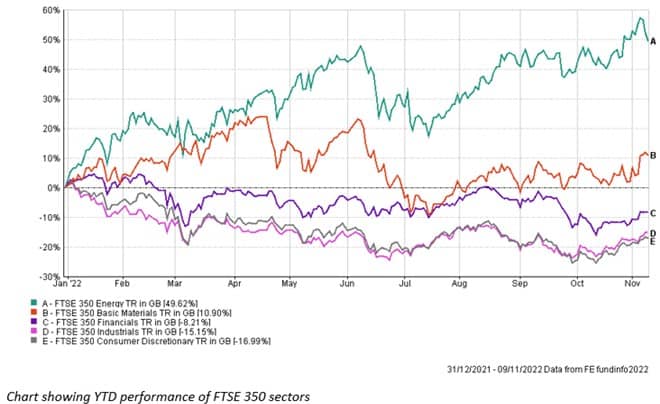

If we look at sector makeup of the FSTE 100 we can further see why the index has performed well compared to the FTSE 250; 22% of FTSE 100 stocks are in the energy and basic resources sectors, both of which have performed reasonably well YTD. In comparison, the biggest sector weightings in the FSTE 250 are financials (44%), industrials (16%) and consumer discretionary (13%). These sectors have been some of the worst performers this year.

These factors highlight some of the reasons for the discrepancy in the performance of FTSE indices this year. It also shows that even if the UK enters a deep recession, this will not necessarily be reflected in poor FTSE 100 performance due to how and where these companies derive their revenue.

In short, the FSTE 100 is not a good indicator for the health of the UK economy. The FTSE 250 is a better gauge but even so half of revenues are imported.

Both indices currently have good dividend yields (3.91% for FTSE 100 and 3.43% FTSE 250). We may see these yields drop as the UK enters a recession, the FTSE 250 more so, as earnings fall or slow. For the FTSE 100 the yield is more likely to be sustainable due to the energy companies paying high rates of dividends; the biggest risk here would be if the UK government imposes windfall taxes on energy companies’ profits.

Fixed Income

Although the fixed income sector has fallen considerably so far this year, valuations are starting to look attractive and there is upside to be found. Yields are expected to have reached their ceiling and prices are expected to converge at least someway to their par value, providing capital returns for investors not holding bonds to redemption.

Investment grade bonds are offering attractive income potentials and default risk is expected to be contained. In any economic slowdown businesses are expected to fail, but quality investment grade bonds are expected to fare better than equities. The strong balance sheets of these companies offer better protection for credit holders rather than equity holders.

While global default rates are historically low, they are expected to rise to around 3% – 3.5% from current levels of 1.4%. This is still low compared to 2008 and 2020.

High yield bonds offer attractive returns albeit with higher credit risk and investors are more tempted by the protection offered by investment grade bonds.

Sell-offs in high yielding bond markets has been overstretched and the widening of corporate bond spreads over government debt is not justified by fundamentals. According to the ICE Euro High Yield index, yields have risen from 2.8% at the start of 2022, to around 7.8%.

While a rise in high yield bond prices is expected, the rebound is not likely to be quick.

US

Economics

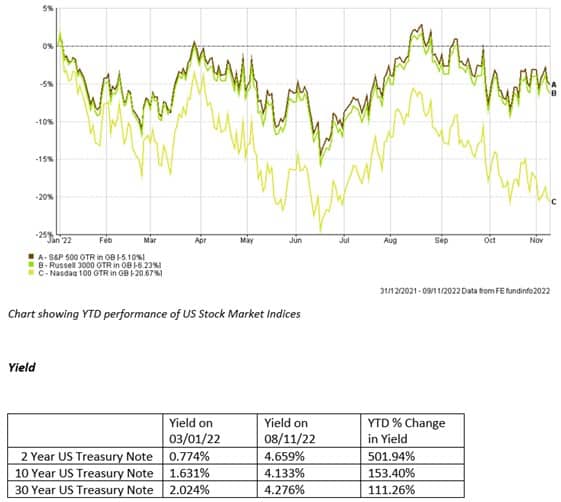

US GDP growth proved to be resilient on the headline figure, with GDP rebounding to 2.6% after spending the previous 6 months of the year contracting. The boost in GDP was as a result of increased exports due to oil sales.

The underlying components of GDP still show that consumer demand is waning and the economy is under strain. A key measure of GDP strength is the final sales to domestic purchases and this grew by only 0.1%, down from 0.5% in the second quarter and 2.1% in the first quarter.

The Fed is expected to continue to raise interest rates by 0.75% at their next meeting, bringing the Feds target rate to 3.75 – 4%. They key question is when will the Fed start to slow their rate hikes. It is difficult for the Fed to judge when the right time is, as interest rate increases take time to filter through the economy and have the desired effect on inflation.

The Fed may well continue to raise rates into restrictive territory in order to make sure inflation is brought down. While this may be good for inflation, on the other hand economic growth will be damaged to a greater extent.

Economic data is giving the Fed signs that what they are doing is working but after months of inaction, there is a danger the Fed could now overact.

The labour market is still strong with unemployment at 3.5%. This is expected to increase quickly next year pushing the US economy into a recession. We are already seeing signs that companies will have to reduce costs further, and one key area is labour costs.

With the big tech companies’ revenue growth slowing, the key theme from their recent investor updates is that costs need to brought down, and this will be achieved by cutting employees.

US CPI for September currently sits at 8.1%, mostly unmoved from the 8.3% recorded in August. For the October reading US CPI dropped to 7.7% further showing that the Fed’s actions are working. After the inflation figures were released government bond yields dropped and equity values rose sharply, with the S&P 500 moving up by over 4%.

Markets

Technology companies face difficult times ahead as pressures from all angles push down earnings growth. At the time of writing, Microsoft and Alphabet have reported weak third quarter results, pushing their values down 7.7% and 9.1% respectively. An estimated $800 billion has been wiped off the valuations of big US tech companies this week. Investors’ confidence in the resilience of tech companies business models to withstand a slowdown has been damaged.

This will reduce the elevated Price/Earnings ratios (relative to the UK and Europe) of these companies and bring them down to more attractive levels. One year ago the trailing P/E ratio of the NASDAQ 100 index was 35.47 and as at 21st October 2022, this ratio sits at 23.07. Forecasts for the forward P/E ratio put it at 20.97 (data from WSJ). Data for the S&P 500 shows similar declines.

If we compare this to the FSTE 100, on 30th June 2022 the trailing P/E ratio was much lower at 15.34 and a current estimated forward ratio of 10.14.

Rising interest rates, a strong US dollar and weak consumer demand are creating a difficult environment for tech businesses.

The main revenue stream for big tech technology stocks is through advertising. In economic slowdowns businesses are cutting their advertising budgets and this results in less revenue for the big tech firms. They also tend to book their profits in foreign currencies and convert these profits back to US Dollars. With a strong US Dollar these profits are being eroded by the unfavourable exchange rates.

Like other global economies, the same sectors are struggling and the same sectors are flourishing.

Energy companies continue to book record profits driving their share prices up. This is most painful for ethical investors, who usually have no exposure to these companies and is a big reason for sustainable funds’ underperformance this year.

The S&P 500 has regained a lot of lost ground this year, while the NASDAQ 100 still lags behind and has seen returns drop further over the past three months as investors sold the tech-heavy index amid disappointed earnings results.

Yields on the 2-year US treasury bond have risen dramatically this year and with the US Fed signalling that interest rates will have to continue to rise – potentially further than expected – yields on US government debt continues their upwards trajectory.

UK government debt is preferred to US government debt and we have seen this over the past month in the 2-year government debt yields. While the UK 2-year yield has steadied, the US yield has continued to move upwards.

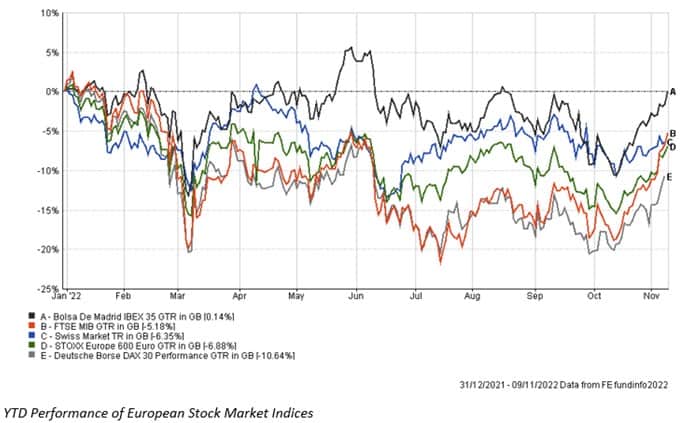

Europe

The Eurozone on the verge of a recession and inflation continues to climb higher, with the October reading clocking in at 10.7%. Latest GDP readings show that growth in the bloc slowed, rising just 0.2% in the third quarter, down from 0.8% in the second quarter.

The ECB raised interest rates by 0.75% to 1.50%, keeping the real interest rate in highly negative territory. The ECB’s latest comments vary in that some members indicate that they may not raise rates much higher amid an oncoming recession, while others follow in the footsteps of the Fed in keeping a hawkish view.

There is a clear disconnect between politicians of Euro countries and members of the ECB. The ECBs main and only goal is to bring down inflation. One of the only ways forward is to raise rates to reduce demand and doing nothing would be worse. Politicians are more concerned about tipping the Eurozone into a recession and are pressuring the ECB to not take rates beyond the tipping point where they further damage growth.

This is likely why we are seeing some comments from ECB members suggesting rates will not rise much further. The next decisions made by the ECB will hinge on the next set of inflation readings.

High energy costs in the winter are likely to bring about a recession as industrial companies are forced to cut back production and consumers’ disposable income is stretched further. This would go some way to bringing inflation down, but it is uncertain whether it will have the full effect desired.

Investors are looking at Euro government bonds in a more neutral view as markets may have overpriced the impact of higher rate hikes.

Since October performance has picked up in the Euro area, but in our view this may be overly optimistic and may be a short-lived rally in a bull market. Investors are currently only pricing in a short-lived recession, but the risks of a deeper recession are present, especially if ECB interest rate hikes drag economic activity down.

Robert Dougherty, Associate IFA

November 2022.

This article is not a recommendation to invest and should not be construed as advice. The value of an investment can go down as well as up, and you may get less back than you invested.