The long period of ultra-low interest rates and high liquidity is over, and some governments don’t know what this means or how to deal with it. The UK is a case in point.

Governments and central banks have two options – deal with inflation and damage economic growth, or ignore inflation and attempt increase economic growth. The UK went for option 2. The pound dropped further, bond yields rose dramatically and equity values dropped. In other words, growth expectations did not rise but interest rate expectations did. Interest rates in the UK are now expected to reach 6% and this has been evidenced in mortgage markets.

In the US, interest rates are continuing to increase and more investors are of the view that the US will be in an official recession in 2023. Equity valuations have dropped since the beginning of the year, but some investors do not believe they have fallen far enough to reflect their fair value based on lower earnings. This puts growth stocks with high P/E ratios at further risk of a fall.

Stagflation is looming in Europe and different regions are expected to react differently depending on their economic makeup. High energy costs persist and this will drag on European economies for some time to come.

In China, regulators are intervening to prop up a financially unstable property market and while this has improved share prices initially, investors are vary wary about the huge leverage underpinning the sector. Chinese economic growth is forecast to miss its target. A reform in the countries zero-covid policy is needed but this looks unlikely to happen in the short term.

Areas of Focus

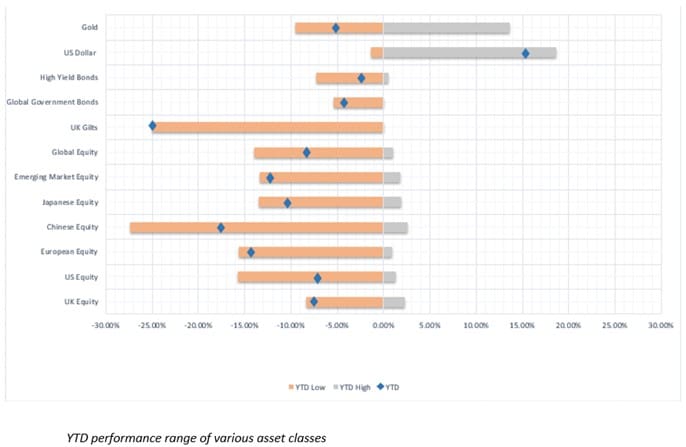

- Although bond yields are continuing to rise, they still offer protection for portfolios as economies near recessions.

- Individual European countries will weather a recession differently. Variance in returns will continue to show.

- The USD continues its strong performance while gold has dropped 5% year to date (YTD).

- Illiquid assets in pension funds face reduced demand as market risk in liquid assets continues to rise.

- UK gilt yields may continue to rise as the government’s recent fiscal plans raise questions about the countries financial credibility.

- Emerging markets face slowing growth and commodity exporters are preferred over importers.

- Quality investment grade credit offers higher coupons (particularly in Europe) and is better positioned to weather an increasingly negative macro backdrop.

UK

We are not short of investment commentary for the UK this month. Uncertainty and volatility have plagued the UK markets once again, this time driven by politics and the surprise “mini-budget” announcements. The financial credibility of the UK has been called into question and consumer confidence continues to plummet.

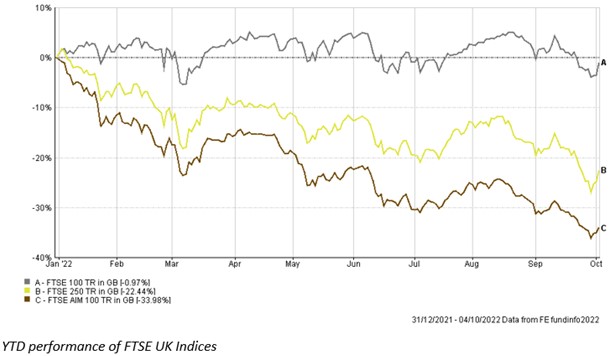

Since the beginning of this year the FSTE 100 and 350 are the still best of a bad bunch among global stock markets, with the FTSE 100 supported by a weak pound, but the underlying economic fundamentals may be a cause for concern. We talk below regarding the implications of a weaker GBP.

The big questions are what corners of the UK market will make an attractive investment, and how deep will a UK recession go.

As mentioned in a previous update, the FTSE 100 will most likely be the best-performing UK stock market index. This is down to the companies that make up this index (many of which book their profits in USD) benefitting from a favourable exchange rate. Bigger companies also tend to be more financially stable and will be better able to withstand higher interest rates and the other hardships brought on by a recession.

UK Gilt yields had soared higher immediately following the announcement of the UK’s tax plans. They have since dropped back after the Bank of England stepped in as lender of last resort, but are still up over 400% YTD.

A big problem in recent weeks has been the investment strategies of pension fund managers, specifically managers for large final-salary schemes. The issues they have faced caused the BoE to step in with emergency quantitative easing. This has highlighted the idea that although government securities have smaller credit risks, the market risk they carry is not something to underestimate.

UK borrowers, whether first-time buyers, those looking to re-mortgage or those on variable tracker rates have seen their interest payments increase. Although more favourable stamp duty rates are being introduced, the savings will be outweighed by increasing finance costs.

The effect of this is to further negate any growth potential through consumer spending.

While UK CPI inflation dropped slightly in August to 9.9%, with food costs and import costs rising it is likely to continue to increase for the rest of the year. Although interest rates are rising, the effect of these increases on reducing inflation usually takes between 18 months and two years to be fully realised.

The outlook for the UK is complicated by the fact that fiscal policy (the government’s tax and spending plans) is in apparent conflict with monetary policy (the Bank of England setting interest rates). While the BoE is trying the slow the proverbial car down by stepping on the brakes, the government has its foot on the accelerator.

The BoE has raised interest rates in order to cool inflation, while acknowledging that the UK will likely enter a recession, if it is not already in one. The government, on the other hand, is adamant it will avoid the UK entering a recession by increasing economic growth – effectively ignoring the goal of bringing inflation down and spooking markets in the process.

According to most economic theory, tax cuts in themselves do not necessarily increase economic growth. As opposed to government spending, which goes mostly into domestic businesses, some of the money from tax cuts will leak out of the economy – they may be saved or spent outside of the UK (importing goods and services).

Further to this, the recent tax cuts announced in the mini-Budget are unfunded and for markets, this is the biggest issue.

The difference between the UK government’s spending needs and the amount of taxation it raises is the called the Public Sector Net Cash Requirement (PSNCR). Any shortfalls in this must be funded by borrowing. As the government is cutting tax rates while at the same time spending on support for consumers and businesses for energy price support, the PSNCR is growing.

The huge increase in borrowing will have to come from new government bond issues. This presents a few problems.

Firstly, if interest rates are rising from historic lows, the cost of this debt will increase substantially.

Secondly, any new gilt issues paying higher rates of interest will lead to investors selling their existing gilt holdings in order to buy the new ones, pushing yields up further.

As the government had not presented any details of how the borrowing will be funded, markets reacted badly.

Increases in gilt yields are likely to reduce equity values further and will make it more expensive for businesses to finance their activities.

All of these factors wane investor confidence in the UK economy, dragging the pound down further.

In the days following the market turmoil the BoE stepped in to attempt to restore some credibility in UK markets. The BoE had been stopping its quantitative easing programme, but had to restart buying bonds in order to stop yields from plummeting and to try to stabilise the pound. Any losses incurred in doing so will be borne by the Treasury (in effect, the UK taxpayer).

Although UK businesses may benefit from increased consumer demand as consumers will have slightly more disposable income, this will most likely be offset by increased inflation resulting from a weak currency and increased import costs.

For example, British airline companies collect their revenues in pounds, but have to buy their aviation fuel in USD. If not properly hedged, this will result in increased fuel costs which may be passed onto the consumer in order for airlines to stay profitable.

Industries such as the alcoholic beverage industry are facing increasing costs. Beer producers often import their grain and barley from the US, which is paid for in USD.

Mortgage lenders in the UK have reduced or ceased offering fixed-rate products which is stopping people from buying new homes. At a time when stamp duty rates and limits have been made more attractive, if the average consumer cannot finance a house purchase then there is no saving to be made. Furthermore, with interest rates expected to be around 6% in the summer of 2023, the financing costs associated with a mortgage will far outstrip the savings on stamp duty.

The new government’s actions have therefore provoked much criticism. So much so that the International Monetary Fund has openly criticised the government’s fiscal plans and urged them to re-evaluate their decisions.

The fiscal credibility of the UK is currently under severe scrutiny. In an attempt to save face the Chancellor retracted his plan to remove the 45% additional tax rate, with the Prime Minister saying the government is listening to voters’ concerns. While there is no denying there has been much public criticism, it is the international markets which have forced the government into this step back, not the voter.

Why has the value of the pound fallen and what does this mean?

Currency markets are the most traded and liquid markets in the world. Consumers, businesses and governments are constantly trading in the currency markets and their effects are widespread.

There are benefits and drawbacks of a strong and weak currency, but for the UK in its present situation a weakening pound will only compound existing problems.

The UK is a net importer of goods and services. This means that the UK imports more than it exports and generally has a deficit on its current account. This deficit must be made up, in part by investment in the UK from overseas. Overseas investors are the biggest buyers of newly issued UK Gilts and their confidence in the UK has dropped.

When the GBP is weak compared to the USD, imports become more expensive. This is because a business which pays for its goods in USD, must sell GBP in order to buy USD. When the GBP is depreciating, one GBP buys less USD. Therefore more GBP must be sold in order to buy an equivalent amount of USDs.

The UK is an importing country so as the pound depreciates, imports become more expensive and this adds to inflationary pressures. With inflation already high, a weak pound further exacerbates the issue.

Exports on the other hand become more competitive as domestic manufacturers’ products are cheaper relative to other countries.

There are many factors that move currency markets, including interest rate expectations, economic outlooks, fiscal policies and overall investor confidence in an economy.

Before the recent announcement of the tax cuts, the pound was depreciating against the USD because investors were able to take advantage of higher interest rates in the US. Currently the BoE base rate is 2.25% compared to the US Federal Reserve Funds Rate of 3-3.25%.

Investors who wish to take advantage of the higher rates in USD will need to hold USD; this involves selling the GBP, weaking the pound further.

Furthermore, investors currently place a higher probability of the UK falling into a recession than the US. When the UK enters a recession the BoE generally lowers interest rates in order to spur economic growth. Thus the demand for the GBP relative to the USD declines.

Following the mini-Budget the pound had initially fallen even further against the dollar, but since has recovered its losses.

US

The US Federal Reserve are likely to back the fourth straight 0.75% interest rate rise in November as inflationary pressures remain. Most officials believe the rates will rise to 4.4% by the end of the year. US GDP is expected to slow to 0.2% this year and officials believe unemployment will begin to rise.

The Fed has stated that the recent changes to UK fiscal policy, including the £45bn tax-cut package, will have raised worldwide uncertainty and may catalyse a global recession. Uncertainty can be detrimental to economic growth as both consumers and businesses may disengage with the economy to reduce exposure to risk.

The dollar has appreciated against the pound (as well as most other currencies) for much of the year. This has benefitted US consumers looking to send money abroad or travel. However, for large corporations who make larger portions of their earnings overseas the appreciation has not been as welcome.

This has disadvantaged technology companies in particular, who make an average of 50% of their sales abroad. The US Dollar index, tracking the currency against 6 other major other currencies is approaching a near 20-year high.

The Inflation Reduction Act, a landmark climate and socioeconomic spending bill, is aimed to encourage the building of clean energy infrastructure through billions of dollars in tax credits. The hope is that the bill will allow the US to maintain a more favourable position to achieve its commitments under the Paris agreement, cutting emissions in half by 2030.

New laws in several states, including Texas, are punishing financial firms that boycott oil and gas. The result, according to former Deputy Treasury Secretary Sarah Bloom Raskin, is an endangerment to global financial stability through encouraging risky loans to energy firms. Raskin stated that large banks will continue lending to energy companies at current levels even though risk management reasons would call for it to be reduced.

The US market outlook is not overly positive, looking at year to date, the S&P 500 has fallen over 20% since the high points reached in January. The Dow Jones peaked at 36,585 in January and had fallen 20%, standing at 29,260 on 26th September. Finally, the Nasdaq fell almost 30% from its peak in January. The contributing factors are uncontrollable inflation rates, subsequent interest rate rises and the uncertainty and fears around recession. Table 1 shows clearly that all three indicators are sitting extremely low on their respective 52-week ranges.

Table 1: US Dow Jones, Nasdaq and S&P 500 as indicators of economic health (KITCO).

US value stocks remain in positive territory for the year, while growth stocks lag far behind. As we said before, with headwinds from slower earnings growth, we may still see growth stocks drop further than they currently are.

China

With the Chinese property sector still in turmoil, regulators have announced plans to attempt to shore up the sector and increase consumer demand.

Bailout funds and loans to complete unfinished houses were announced, with the Peoples Bank Of China also cutting the lending rate for house buyers. Various other schemes have been introduced, such as banks being allowed to offer cheap loans (regardless of the floor in lending rates) and rare tax incentives that allow homeowners to reclaim income tax by selling their house and buying another one within a year. All of these schemes are aim to support the struggling property sector.

While they sound good in theory and have pushed up share prices in property companies, investors are still concerned over the financial reliability of the sector since defaults on both dollar and renminbi denominated debt.

Manufacturing has continued to weaken as China’s zero-covid policy continues to deteriorate economic conditions and the demand for Chinese goods decreases.

For these reasons Chinese markets have had a mixed year so far, with YTD performance placing somewhere in the middle amongst major global equity markets.

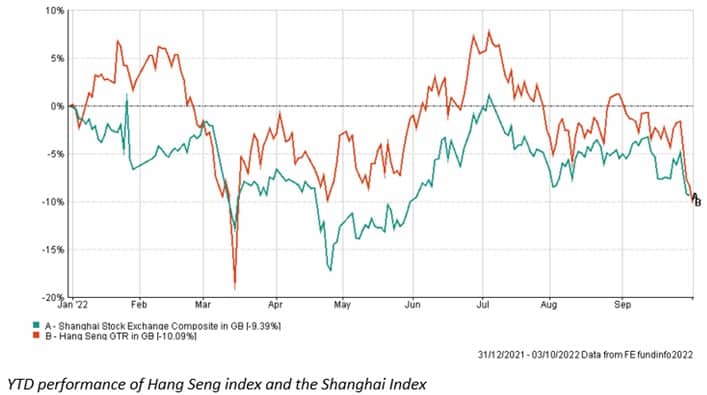

Chinese stocks listed on the Hang Seng Index have suffered over the past month, with the index down 9.49%. While global stocks have suffered YTD due to tighter monetary conditions, Chinese stocks have been hit particularly hard as slowing economic growth and political tensions, the American-China relationship being strained over Taiwan.

At the start of the year Chinese government bonds had a significant yield advantage over other government debt, particularly US government bonds.

The yield on the 10-year Chinese government bond had started the year at around 2.8%, compared to 1.6% for US debt of the same maturity. Now, the 10-year Chinese debt trades at just under 2.8%, while the yield on US debt trades at 3.7%. Portfolios have therefore switched from holding Chinese to US debt, attracted by the higher returns offered by the latter.

China’s looser monetary policy should push up its stock markets, particularly when other markets are tightening. However, the combination of various factors such as slowing economic growth, a zero-covid policy, a troubled property market and long-term concern over Chinese political interference has produced a difficult and uncertain backdrop for Chinese assets.

Note that on the performance chart below, the Hang Seng Index has a greater loss than the Shanghai Index due to restrictions imposed on foreign money being removed from mainland Chinese stock markets. Investors can freely remove demand from the Hang Seng index.

Europe

The most prominent issue surrounding Europe continues to be energy costs and the ensuing cost of living crisis.

The European Central Bank’s chief economist has now called on the eurozone governments to increase taxes on high earners and profiting companies to finance those struggling the most with the energy crisis. If action is not taken the Eurozone is at risk of stagflation for a sustained period of time.

These comments were made following the UK’s decision to reduce taxes for the highest earners – part of a package of tax cuts that caused a sell-off in bond markets and a subsequent depreciation of the pound. Lane argues that providing support through tax increases on high earners will have less of an impact on inflation than increasing deficits through direct governmental funding to those in need.

These comments support the EU’s plan to raise €140bn from a levy on excess profits in the energy sector, this is due to be discussed by policymakers at the end of September. The EU has not advocated higher taxes for wealthier citizens as of yet.

The German chancellor has announced a €200bn cap on gas prices to act as a shield. This will be financed by extending an off-balance sheet fund that was set up to provide aid during the COVID-19 pandemic.

The inflation rate in Germany has reached a 70-year high, at 10.9%, causing economists to fear a deep recession is on the horizon. This announcement is predicted to lift the eurozone inflationary rate to a record high of 9.7% in the next few weeks.

In Italy, a coalition led by Giorgia Meloni’s arch-conservative Brothers of Italy party won a decisive victory in the snap election and is now in a position to form Italy’s first far-right led government since the second world war.

Meloni becomes the first Italian female prime minister since the 1861 unification. Although the leader has pledged to continue COVID-19 recovery funding and Russian sanctions, Brussels worry that the radical leader may make controversial decisions in the future.

Weak credit fundamentals amid policy tightening is causing investors to tread carefully in this area. While the credit spread between 2-year Italian government debt and 2-year German government debt has narrowed slightly, it is still wider than at the start of the year, indicating an increase risk premium for lending to less credit-worthy governments.

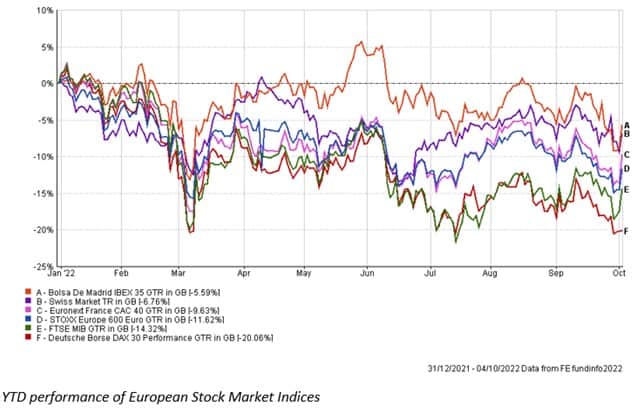

Spanish equities have outperformed other European countries since the beginning of this year. This is due to their higher exposure to interest-rate sensitive financial companies. However, this puts the region at a greater risk when there is a downturn and when interest rates are reduced. In a recession more businesses will fail and this will put pressure on financial companies.

Swiss equities have also fared better than other European countries and many investors consider them to be better positioned going forward, owing to a higher proportion of defensive industries such as healthcare and consumer staples.

For European Investment, growth is slow (if present at all) because of the uncertainty surrounding Russia-Ukraine conflict, the energy crisis, inflation, and interest rates. The chart below shows how European equity markets have reacted to this year’s events – the German DAX performing least well, dropping almost 17% over the last year. This is primarily due to the German economy’s reliance on Russian gas, the supply of which has now been reduced severely. Headwinds to earnings present valuation issues in the short-term, but long-term prospects remain elevated.